Hand flipping of 2025 to 2026 on wooden blocks with the number five already faded. Turn of the new year. New year's resolution.

The Energy Transition in 2026: 10 Trends to Watch

This year should see more promising clean energy solutions reach maturity and set the stage for wider adoption.

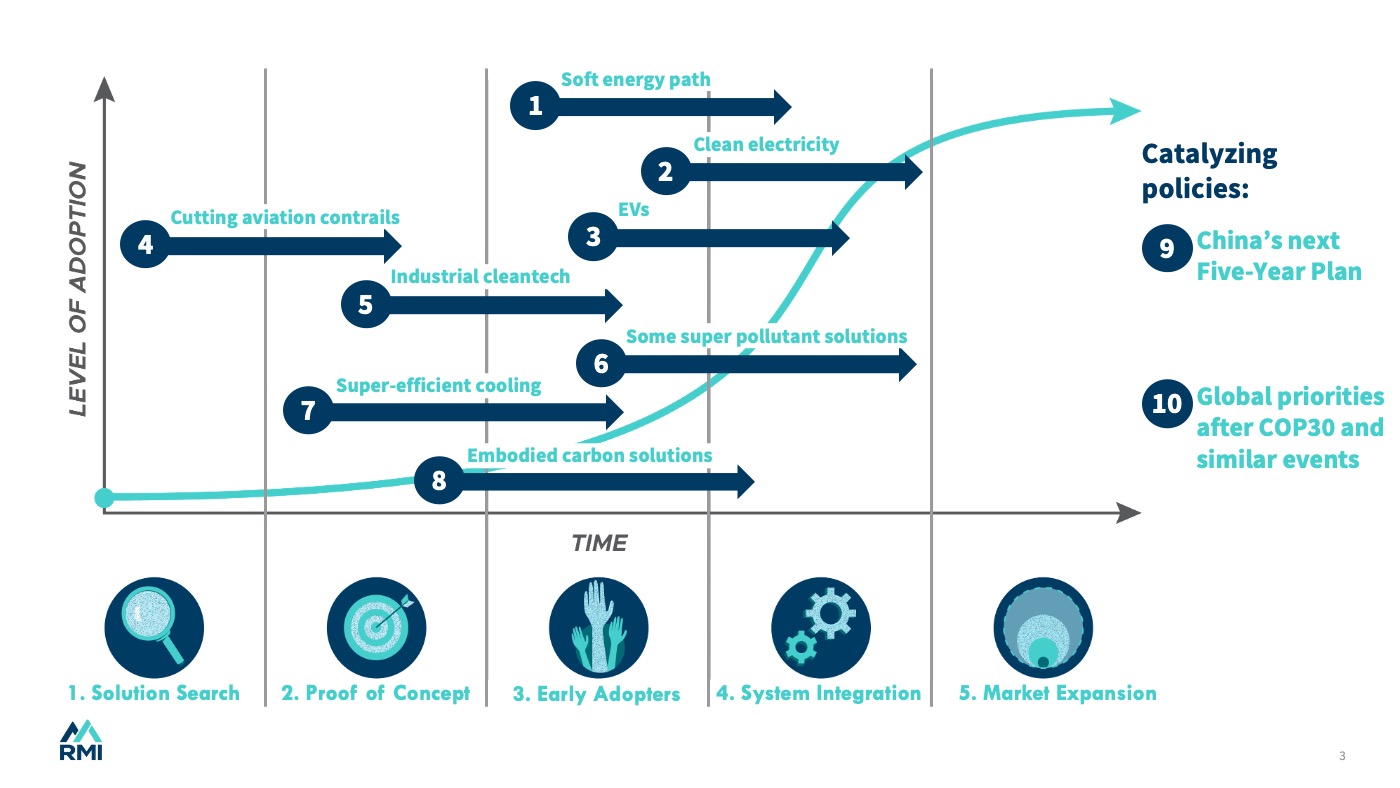

Technological progress is rarely linear. From the automobile to the television to solar power, a process of “gradually, then suddenly” can be observed. This process traditionally follows five distinct phases (outlined in Exhibit 1). The good news when it comes to our clean energy future is that many promising solutions are reaching stages of maturity that bring them closer to widespread adoption across a wide array of sectors and geographies.

Exhibit 1. Ten trends for 2026 along the 5 phases of technology adoption.

1. Decision makers consider “soft energy paths” to meet growing electricity demand

October is the 50th anniversary of “The Road Not Taken”, a landmark article by RMI cofounder Amory Lovins. The article encapsulates “soft energy paths,” a strategy which combines quick renewable energy deployment with “a prompt and serious commitment to efficient use of energy.” Fifty years later, this idea is as relevant as ever — as a new era of load growth requires fast, flexible solutions to meet increased demand. This time, it’s especially important in the Global South, where rapid demand growth and scarce capital combine to make these strategies more compelling than ever before.

Energy efficiency is a critical first fuel. Compared to supply-side projects, demand-side measures can increase grid capacity at roughly half the cost and 5 to 10 times the speed. For the grid itself, alternative transmission technologies can increase buildout several times faster and cheaper than traditional transmission. Innovative supply solutions, from virtual power plants to “power couples” for co-location, are also in the early adoption phase (phase 3).

2. Clean energy supports affordability with the right policies and investments

Meanwhile, wind and solar energy have entered phase 4 (system integration) and are set to continue growing. Countries such as Denmark have generated 70 percent of their electricity from solar and wind, while rising renewables are taking a larger share of generation in much of the Global South.

Combined with rapid electrification, this puts massive requirements on infrastructure and “supporting innovations” such as flexibility. The main challenges now lie in orchestrating the renewable technologies into a new energy system that can support electrification efficiently.

Now, as electricity demand rises, rising costs are a major concern — including in the United States, where affordability played a key role in recent elections and could do so again in November’s midterms. Thankfully, we can slash energy costs and waste by upgrading home technologies, implementing the right market mechanisms and policies to fix who pays, and accelerating investment in the “soft energy path” solutions above.

Global trends are already showing what’s possible for clean energy affordability. Average battery grid storage costs are more than 2 times lower than 2 years ago and more than 3 times lower than 3 years ago. In tandem, more than 90 percent of new renewable energy projects are cheaper than fossil fuel alternatives, and new renewables generation is now eclipsing total electricity demand growth. Leading experts expect this trend to continue as renewables and storage rise up the S-curve of phase 4, accelerating the transition away from fossil fuels.

3. Electric vehicle adoption enters a new phase with further action on key enablers

In the passenger transport sector, EVs have emerged as the ‘winning technology’ and are moving from niche markets (phase 3) to the mass market (phase 4). As such, adoption varies widely, but more than 1 in 4 new cars globally now have a plug, helping importing countries collectively save more than a million barrels of oil per day.

Reaching scale will also come with infrastructure and supply chain bottlenecks that must be resolved. For example, this new phase requires further work on the enabling environment, from manufacturing investment to preparations for the grid. Affordable purchase prices and charging options are also crucial. New research, policies, and tools can help accelerate charging stations to match EV growth while managing new electricity demand and improving battery circularity.

In addition, battery electric trucks are moving from pilots (phase 2) to niche markets (phase 3) with several models commercially available and others nearing commercialization. We expect continued rapid improvement of battery electric trucks in terms of cost and performance, alongside a need for scaling niche markets (through trucking corridors, for example).

4. Aviation contrails see further awareness and action with new collaborations

New partnerships and explainers have highlighted the potential impact of aviation contrails — and the opportunity to quickly cut 80 percent of their warming by just tweaking 2 percent of flights. Success would make contrail avoidance the sector’s greatest near-term solution for warming through 2050.

Early solutions are ready for pilots as they move from phase 1 to 2. Recently tested corporate accounting methods could make a major difference, if strong stakeholder collaboration continues. Further action could come from the EU Emissions Trading System. A key step now will be to build the transparent data practices that can underpin future progress.

5. Industrial cleantech is boosted by new policies and protocols

Industrial heat pump adoption is nearing mass market (from phase 3 to phase 4), as progress in the buildings sector helps heat pumps improve performance while cutting costs. This progress creates inroads into higher-temperature industry, enabling further opportunities for electrification in industry.

However, many industrial solutions are still in phase 2 or early phase 3 — such as green hydrogen, where top-down market mechanisms can incentivize early adoption. In 2026, several related policy efforts can spark change across the world.

First, industrial efficiency could be improved significantly. High-efficiency motors are mature (phase 5), but only account for one-quarter of industrial motors; technological improvements could save more electricity globally than the entirety of demand from data centers. Other measures include facility design, flexibility, and smart manufacturing.

Broader actions include the EU’s Carbon Border Adjustment Mechanism, which is moving from reporting to action across several industrial sectors alongside new reporting requirements from the EU Methane Regulation. India’s carbon market is also preparing for compliance trading in the second half of 2026. And voluntary carbon markets will continue to build on the recently launched Carbon Data Open Protocol (CDOP).

6. Super pollutant solutions find increased visibility and new market mechanisms

Similar progress is helping to raise awareness across methane and other non-CO2 super pollutants. New funder collaboratives, action roadmaps, and powerful data from Climate TRACE are starting to bring unprecedented visibility to ground-level ozone, the air pollutant that also causes as much current warming as the global road transport sector.

Though early-stage field-building remains, many solutions intersect with energy transition efforts that are well into phases 3 and 4 of deployment. Enabling conditions are catching up, from recent landfill methane policies to corporate credit purchases that reach more sectors. If this progress continues, it can leverage a crucial opportunity to cut warming fast.

7. Cooling solutions reach new readiness, from innovation to deployment

From appliances to design innovations, cooling solutions are gaining ground. India is a crucial player, as a leader in recent efficiency progress as well as cooling demand growth.

Take super-efficient air conditioners, which have progressed from a phase 1 solution search (via the Global Cooling Prize) to a phase 2 proof of concept. Nine months of field testing in India’s Palava City showed that the winning technologies can cut appliances’ costs, energy use, and strain on peak electricity demand by half or more. This coming year can accelerate adoption by scaling proof points, building capacity among manufacturers, and taking other market activation steps across awareness, finance, and demand aggregation.

Passive daytime radiative cooling (PDRC) is nearing a similar stage, with a recent call to demonstrate performance in real-world pilots. The coming months could show which approaches can lead.

8. New standards catalyze embodied carbon solutions

Another opportunity for buildings is to improve embodied carbon, which accounts for more than one-tenth of global emissions today. In countries like India, where as much as 90 percent of 2050 floor space has yet to be built, there are immense benefits to building right the first time.

With many approaches in phase 2 and 3, policy standards can help incentivize early adoption. The RESNET Standards in the US are one such example, with publication and training expected in early 2026.

9. China’s upcoming Five-Year Plan has ripple effects across the world

China is the pivot nation in the global energy transition, and its recent cleantech exports are reshaping the international landscape. Thus, this spring’s release of the 15th Five-Year Plan will be closely watched. As emissions begin to plateau and fall, but climate pledges remain modest, how will the next plan approach different energy technologies?

With its clean energy buildout firmly in phase 4 (or 5) across key technologies, China is transitioning fast and looking to new markets for its solar panels, batteries, and electric vehicles. But results will depend on how other countries navigate trade tensions alongside the demand for clean energy’s affordability.

10. Global climate efforts host key convenings after a year of unfinished business

At the global level, 2025 left unfinished business across a range of policy efforts, from the International Maritime Organization to the COP30 climate conference outcomes. Even with the delays, there is a clear theme of implementation as policy efforts attempt to match the progression of technologies to the deployment phase.

The coming year will have several key milestones, including sessions of the new Global Implementation Accelerator as well as April’s First International Conference on the Just Transition Away from Fossil Fuels. Key roadmaps on fossil fuels and forests are set for release by COP31, when last year’s Brazilian hosts pass the baton to Turkey and Australia.

It can be easy to get lost in the noise of the news cycle. But by returning to these energy transition phases, we can keep a systems view of the incredible opportunities for progress.

The authors wish to thank Yuki Numata, Ben Feshbach, and Colm Quinn for their contributions to this article.