Learn how we are working to transform how we use and produce energy.

Why We Need Transparency in Metals Recycling to Reach Climate Goals

Post-consumer recycling needs to increase significantly by 2050; better disclosures can speed up that process.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Have you ever stared at the universal symbol for recycling — the “chasing arrows” logo stamped on a soda can — and wondered how much of the can actually gets recycled? Alongside the proliferation of “made from 100% recycled materials” product labels, it can be hard to separate fact from fiction in these claims.

Improved recycling and resource efficiency are an integral part of the 1.5°C climate-aligned decarbonization pathways in many metal sectors. Material efficiency and recirculation contribute to almost 20 percent of the cumulative greenhouse gas (GHG) emissions reductions necessary between now and 2050 from the steel and aluminum sectors. Consumer-facing companies like Apple, BMW and beverage can manufacturers like Ball are setting ambitious targets related to recycled content in their products.

In the metals sector, particularly for steel and aluminum, the use of recycled material (also called scrap) has been a part of the production process for some time. There has been a gradual buildup of scrap-based electric arc furnaces (EAFs) for steel manufacturing and new recycling facilities for aluminum product manufacturing in North America.

While increased scrap availability and economics might have played a role in getting the facilities built, these companies are starting to capitalize on the positive environmental benefits of products with recycled content. Branded products from steel and aluminum companies offer a case in point. Despite this increasing scrap usage, there is a lack of transparency around what kind of scrap is used in different products.

This is important because from an environmental perspective, the use of scrap generated from manufacturing processes provides less environmental benefits compared to the use of end-of-life scrap. To explore the nuances around scrap usage, let’s look at the aluminum sector.

The Role of Scrap in the Aluminum Industry

Scrap is generated at multiple steps in the lifecycle of an aluminum product — a soda can, for example. Based on where in a product’s lifecycle the scrap is generated, it can be classified as pre-consumer scrap, post-consumer scrap, or internal scrap:

- Pre-consumer scrap includes the waste aluminum materials that come from manufacturing final aluminum products such as beverage cans from semi-fabricated aluminum products (also called semis) such as rolled can sheet.

- On the other hand, post-consumer scrap (or end-of-life scrap) is the recycled aluminum from various aluminum products that have reached the end of their useful life in the economy.

- The scrap that is formed when molten aluminum is cast into ingots or when aluminum slabs are converted to rolled sheet doesn’t fall into the pre- and post-consumer dichotomy. This waste material, usually referred to as internal scrap is mostly fed back into the remelting processes onsite.

From a climate mitigation perspective, the collection, recycling, and reuse of post-consumer scrap should be encouraged as much as possible. It provides emissions benefits by replacing the emissions-intensive production for primary aluminum (16 tons of CO2e per ton of primary aluminum as global average).

On the other hand, pre-consumer scrap use does not impact the volume of emissions-intensive primary aluminum used (see Exhibit 1). Instead, generation of pre-consumer scrap is primarily an inefficiency (i.e., it consumes additional energy to be reprocessed) in the system to produce the desired output (e.g., beverage cans). As a result, emissions reductions at the global level will be achieved by reducing the generation of pre-consumer as opposed to increasing its recycling rates (which are already high at around 96 percent).

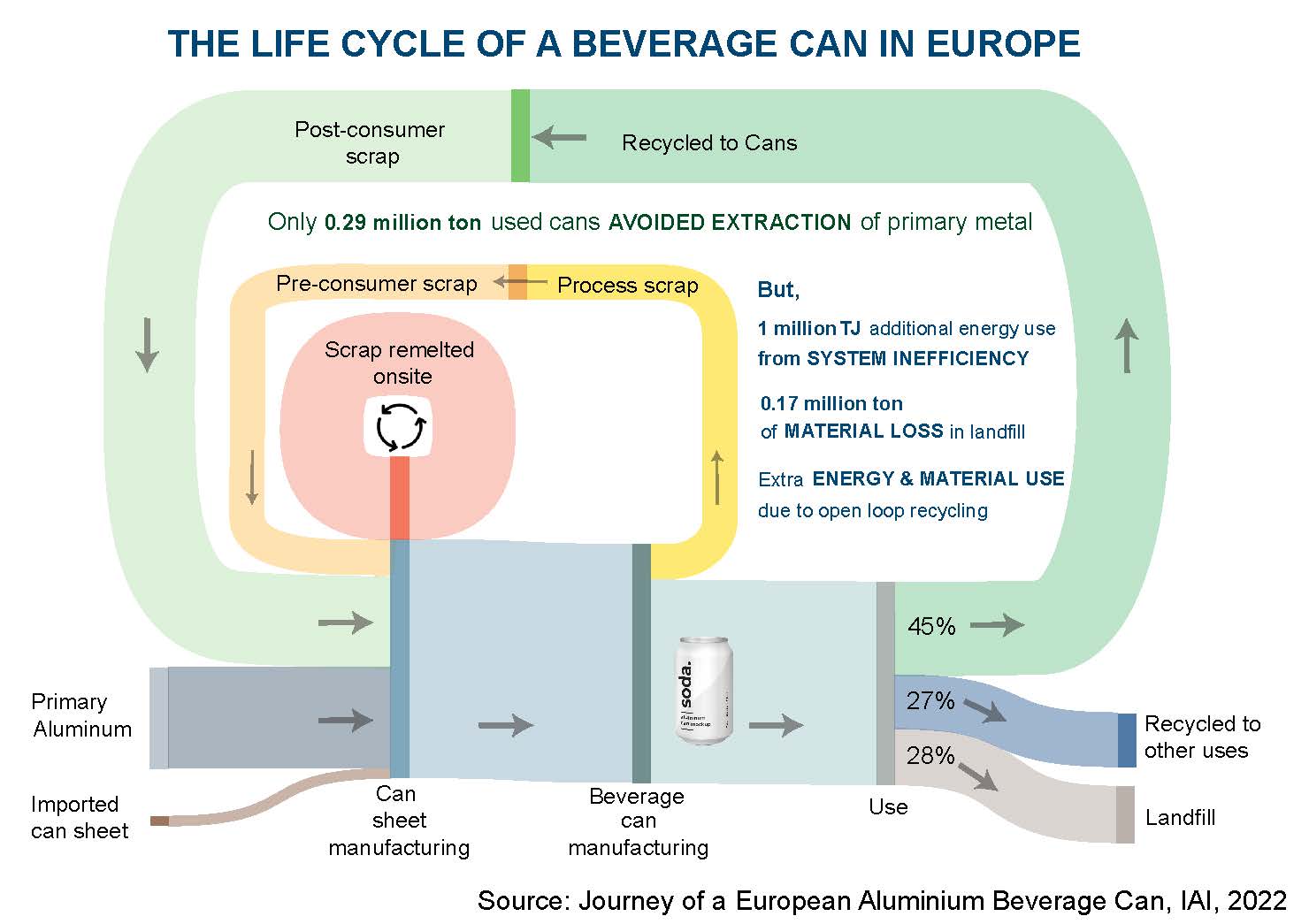

Despite its environmental benefits, not all post-consumer scrap is looped back into aluminum production. Consider the case of aluminum beverage cans in Europe.

In 2019, among Europe’s beverage cans that have reached their end-of-life, roughly 45 percent were used again in the production of new cans. Around 27 percent were recycled to other uses. Almost 28 percent of the used beverage cans either ended up in a landfill or were incinerated.

Globally, around 26 percent of the total post-consumer scrap generated from all aluminum products (roughly 7 million tons) ends up in a landfill or incineration facility currently. This number is expected to be around 18 million tons by 2050.

Exhibit 1

For the aluminum industry to stay within 1.5°C aligned greenhouse gas (GHG) trajectory, the share of pre-consumer scrap to the total aluminum production needs to decrease from 13 percent in 2020 to around 9 percent by 2050. This can be achieved through improved production efficiency of aluminum manufacturing processes so that there is less pre-consumer scrap in the first place.

The pre-consumer scrap that is inevitably generated needs to be completely recovered and used back in aluminum production. Simultaneously, the share of post-consumer scrap needs to increase from 21 percent in 2020 to 46 percent in 2050 even as total aluminum production is expected to rise considerably by 2050. In addition to this, there will be about 30 million metric tons of internal aluminum scrap remelted each year until 2050.

Exhibit 2

Current state of reporting

To incentivize the use of more post-consumer scrap, it is important to know what percentage of an aluminum product’s inputs are from this end-of-life scrap. Currently, most aluminum producers just report the total recycled content in their aluminum products. Making it impossible to know whether or how much post-consumer scrap was used. To overcome this challenge, buyers of aluminum products are increasingly requesting more information on the share of post-consumer scrap in their purchased products.

International Aluminum Institute has also released guidelines on aluminum scrap transparency that highlight the need for aluminum producers to report on the percentage of post-consumer scrap share in their products. Once reporting of post-consumer scrap share becomes common practice, it will be easy for aluminum buyers to make informed purchasing decisions based on that reported data. It can lead to increased demand for products with high post-consumer scrap content. This will provide the right incentives for aluminum producers to increase the use of post-consumer scrap within the aluminum sector. This can lead to broad sectoral decarbonization. There are already some signs of this increased demand in the market.

At the end of 2022, Fastmarkets (a commodity price reporting agency) released a new price assessment for aluminum billets with more than 20 percent post-consumer scrap content. This was in response to increasing demand for secondary billets, which is expected to grow in the future. Recent projects exploring effective recovery techniques and use of materials from end-of-life products are another sign of growing interest in post-consumer scrap.

Better Disclosures, More Recycling

Just like in aluminum, there is a need to differentiate the use of pre- and post-consumer scrap in the steel sector as well. Even though more than 70 percent of the steel generated in the U.S. and 50 percent in the EU is from scrap, at a global level the scrap share of the total steel scrap generated is much lower. Separate disclosure of the different types of scrap inputs into products can eventually lead to improved collection and recycling rates of post-consumer scrap resulting in broad sectoral decarbonization.

The Aluminum Emissions Reporting Guidance, which will be released for public consultation soon along with the Steel Emissions Reporting Guidance, contains guidelines on separate reporting of post-consumer content. Along with the IAI aluminum scrap transparency guidelines, these guidance documents represent a growing trend toward separate disclosure of post-consumer scrap content.

Related Insights

Harnessing Green Demand to Drive Sustainable Chemicals Production

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.