Learn how we are working to transform how we use and produce energy.

Forging a Clean Steel Economy in the United States

Achieving a net-zero US steel sector will require investments in new, low-emissions primary steel production.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

In a big year for climate action, 2022 saw the United States double down on strategies and mechanisms to accelerate its economy toward achieving net zero. These incentives at the state and federal level (including the CHIPS and Science Act, the Infrastructure Investment and Jobs Act, and the Inflation Reduction Act) promise to slash emissions across key sectors, strengthen communities, and provide new development opportunities. This is a critical boost for US heavy industries, particularly the iron and steel sector, which need both regulatory and economic instruments to transition effectively.

The US steel industry claims one of the cleanest global emissions footprints due to its high recycling rate of scrap. Roughly 70 percent of the steel made in the United States comes from this recycled scrap (known as secondary steel) and is produced in electric arc furnaces (EAFs, also known as mini-mills).

The collection, sorting, and market for scrap is well executed, with a recycling rate between 80 and 90 percent. But the supply of scrap is fundamentally limited by the rate at which steel-containing products like cars, buildings, and white goods reach end-of-life. This means that even as scrap-based suppliers expand and attempt to move up the quality ladder into sectors like automotive, achieving a net-zero steel sector will still require investments in new low-emissions ore-based primary steel. In fact, the handful of ore-based steel assets in the Midwest disproportionally accounts for approximately 73 percent of the sector’s emissions due to the higher energy use and reliance on coal.

The picture is similar globally, with an even higher reliance on ore-based steel. However, industry first movers are already working to lower emissions through carbon capture or renewable hydrogen pathways to meet demand appetite from buyers.

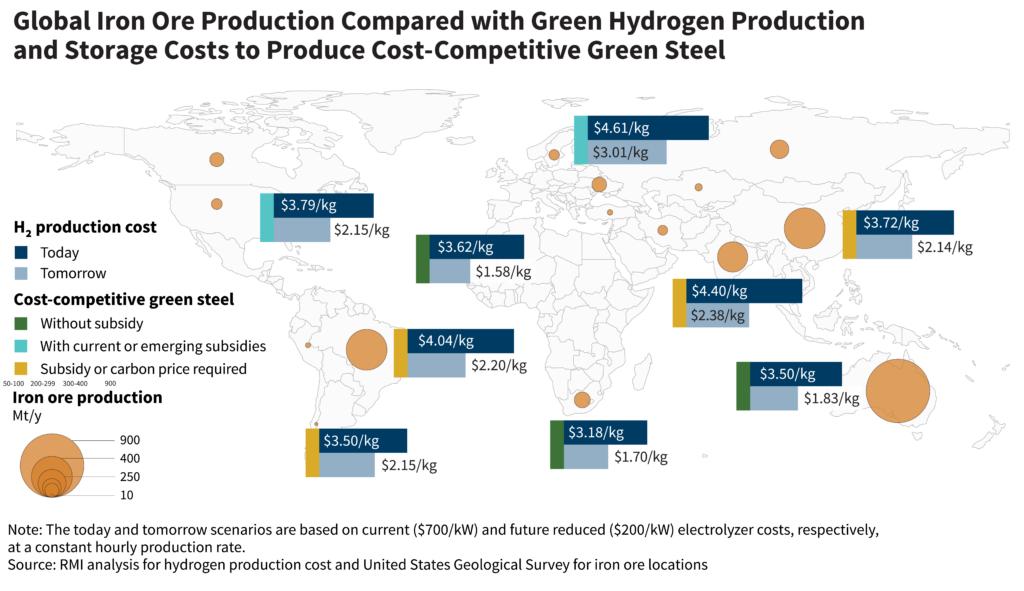

This momentum, fueled by public-private partnerships, indicates the appetite, particularly for naturally advantaged regions, to claim market share in low-emissions differentiated steel. The provisions in the IRA and other federal support combined with local supply chains and a strong skills base provides US producers with a window of opportunity to produce the most cost-competitive low-emissions steel globally (Exhibit 2) — thus improving the US trade balance.

Decision Point

The global steel production emissions intensity has steadily trended upward over the past 10 years, mainly due to new production in China. Conversely, the US steel emissions intensity has been reduced by 17 percent since 2014, due to an increasing share of production from EAFs and energy optimizations at integrated facilities. These steps, along with setting corporate climate goals, indicate movement in the right direction. If we dive a little deeper however, evaluating climate alignment at the corporate level for US producers (Exhibit 3) relying on blast furnace technology — it is clear that a major technological shift is required to converge to a 1.5°C trajectory.

Given that nearly half of the primary steel assets face major investments this decade to extend their operational lifetime, the choice to transition to direct reduction technology utilizing natural gas could be the first step to maintaining sustainable development for the Midwest, helping the region compete with less traditional production bases set to spring up elsewhere in the country.

Encouragingly, subsidies offered by the hydrogen production tax credit (PTC) provide an opportunity to leapfrog to renewable hydrogen utilizing this same direct reduction technology (Exhibit 4). This could shift the most cost-effective production locations to those that combine low-cost iron ore with high renewable energy capacity factors (instead of low-cost fossil fuels), inviting new regions in the United States to establish low-emissions steelmaking. A similar trend is occurring globally as these naturally advantaged regions explore options to integrate into a new low-emissions steel supply chain.

US blast furnace operators have employed a strategy of owning and operating upstream coal mining and coke assets to avoid fossil fuel price fluctuations. Switching to direct reduction technology with natural gas, however, may expose producers to this volatility. At their peak, natural gas prices were 2.5 times higher than historic averages and have yet to subside (Exhibit 5 compares energy costs). To have assurance around feed and fuel prices, producers could look to apply the same business model with renewable hydrogen as it allows for longer-term price stability given its low-marginal cost nature.

Acting Now to Ensure US Competitiveness

The US steel industry has been here before. In the 1960s, a new technology (basic oxygen furnaces) offered steelmakers lower costs as well as improved environmental and safety performance. US operators were slower to adopt this technology than international peers, eroding competitiveness. The result? The US steel industry went from importing less than 2 percent of steel in 1950 to 17 percent just 25 years later. This caused the shutdown of approximately 75 percent of the US blast furnace fleet from the mid-1970s through 2000.

The industry finds itself in a similar position today. Given recent technology pilots and continued cost declines in renewables and electrolyzers, hydrogen-based steelmaking has become a viable alternative. Recent federal policy support in the form of the hydrogen tax credit has now pushed hydrogen-based steelmaking to cost parity in the US. By working with state policymakers, local communities, workforce and other stakeholders (Exhibit 7) US steelmakers can this time lead the adoption of this new technology.

Download our report Unlocking the First Wave of Breakthrough Steel Investments in the United States.

Related Insights

Advance Market Commitments Today Can Build a Low-Carbon Tomorrow

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.

{kind=link}