Learn how we are working to transform how we use and produce energy.

Transforming the US Power Sector in the Decisive Decade

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

The 2020s are poised to be transformative for the US power system. 2019 capped a decade characterized by the decline of coal and the rise of natural gas and renewables, reducing emissions and dramatically reshaping the generation mix that powers an increasingly digital economy. The first 14 months of the 2020s brought a global pandemic and major blackouts, spurring an increasing focus on resilience, introducing new uncertainty into electricity system planning, and setting up the next decade to be just as transformative as the previous.

The power industry’s transition over the next ten years will also play a central role in staving off the worst impacts of climate change. Addressing climate change requires rapid, economy-wide decarbonization in this decade to limit cumulative greenhouse gas emissions. Because the power sector can use available, scalable, and low-cost technologies today, it is poised to both continue to cut emissions and simultaneously support electrification in other economic sectors.

To respond to both the shifts in the power industry and the need to rapidly decarbonize in this decade, we must get started immediately. Today, RMI released two reports that lay out practical, cost-effective, and near-term steps to meet both sets of challenges.

Accelerating a Carbon-Free Electric Future

The 2020s are expected to continue the defining trend of the US power system: the economically-driven shift from legacy, costly coal plants to new, lower-cost wind and solar generation. By managing this ongoing shift carefully, utilities can simultaneously lower electricity bills, cut carbon emissions, and retain reliability.

While some observers have tried to capitalize on recent blackouts in California and Texas by falsely blaming wind and solar for grid outages, these arguments are mere distractions from the underlying facts. Large parts of the US power system, outside of California and Texas, have a significant over-capacity of coal- and gas-fired power plants, and thus can easily accommodate coal retirement and renewable replacement without compromising reserve margins.

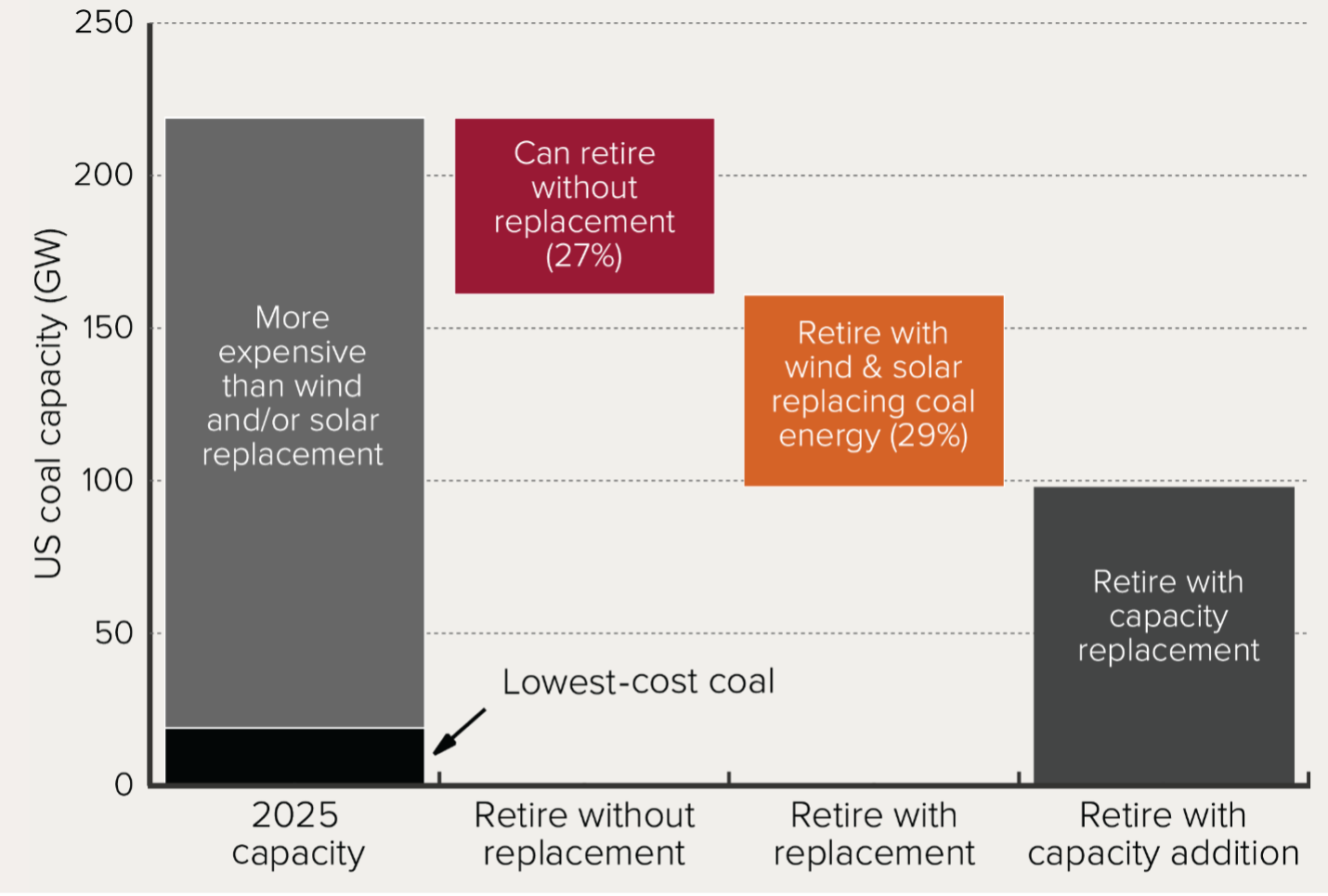

In RMI’s new report, Cutting Carbon While Keeping the Lights On, we find that over 50 percent of the US coal fleet, mostly in the Northeast and Southeast United States where utilities have historically over-invested in now-uneconomic coal plants, could be retired by 2025 without a direct capacity replacement (Exhibit 1). Replacing the electricity generated by these coal plants with lower-cost wind and solar energy would immediately reduce electricity costs and help kickstart the rapid decarbonization of the US power system.

Looking Forward: Decarbonization through 2030

While significant progress towards a least-cost and reliable decarbonized power system can be made with coal retirement and renewable energy investment through 2025, that is only the beginning of the opportunity for transformation. The US power sector will also need to respond to significant load growth (in part due to increasing electrification of buildings and vehicles), improving capabilities and economics of “clean energy portfolios” as alternatives to new gas-fired power plants, and ever-stronger climate policies and commitments (at the corporate, utility, state, and federal level). All of these trends will encourage the industry to transition to a decarbonized future.

To arrive at this future, utilities will need to make significant investments in this decade. In the second RMI report released today, How to Build Clean Energy Portfolios, we identify a need for $300–$750 billion dollars in new investment and suggest processes that allow vertically integrated utilities, regulators, and policymakers to cost-effectively procure clean energy solutions.

Today, utility procurement processes in most of the country are outdated, favor legacy technologies like coal- and gas-fired generation, and fail to provide a level playing field for clean energy portfolios. Unless utilities modernize these legacy procurement processes, they risk locking in trillions of dollars of customer costs and billions of tons of CO2 emissions with near-term resource investments, setting back progress on both affordability and climate for decades.

Fortunately, there are leading examples from utilities across the country of next-generation procurement practices that effectively promote competition between resource types and lower electricity costs. Our report highlights successful procurement processes that are:

- All-source, to select portfolios of optimal utility-scale and distributed energy resources (DERs) and capture the value of interaction between resources;

- Objective-aligned, to enable investments to address diverse, jurisdiction-specific values (e.g., resilience, decarbonization, local economic development) that stakeholders seek; and

- Least-regrets, to limit the risks of greater-than-anticipated costs for meeting system needs by capturing benefits of competition and declining costs of new technologies.

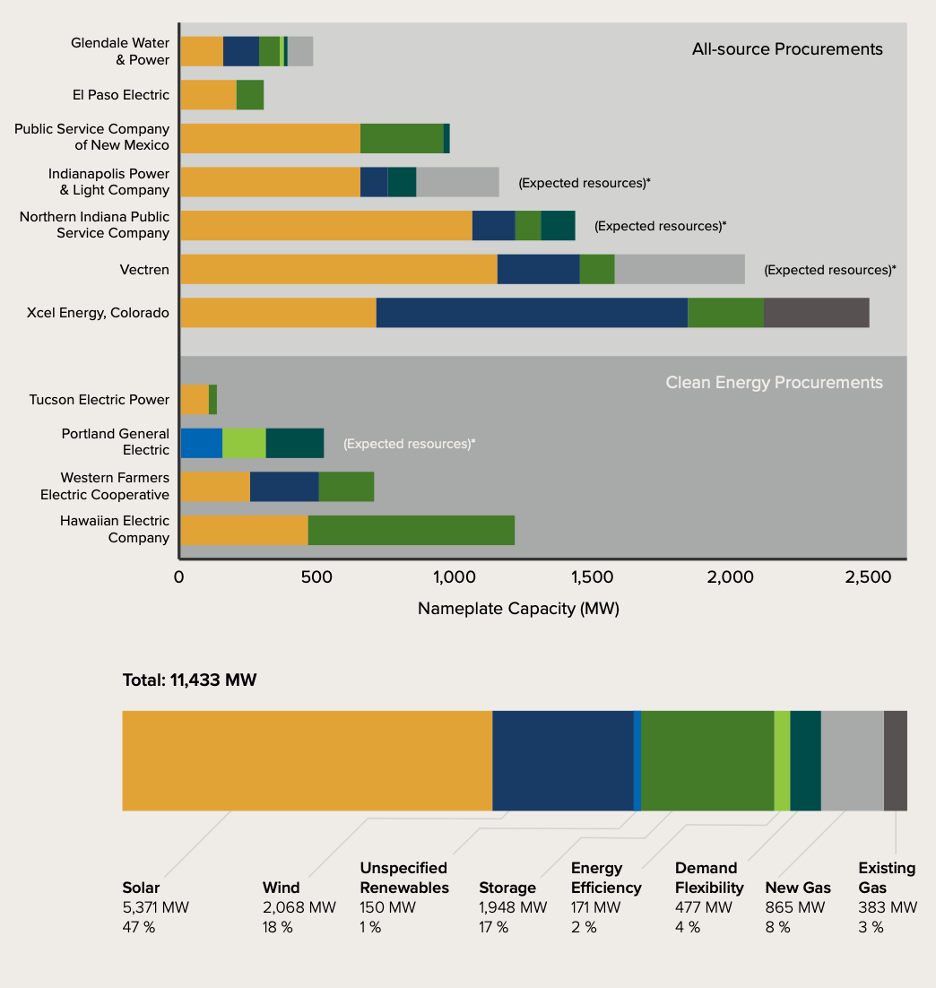

When utilities apply these emerging best practices in resource procurement, they overwhelmingly find that clean energy represents the least-cost, highest-value option for grid investment (Exhibit 2). RMI’s new report, produced in collaboration with the Regulatory Assistance Project, looks at these examples and lays out recommendations for utilities, regulators, and policymakers in each state to replicate these early success stories. This will make it possible to scale the benefits of cost-effective clean energy to all US utility customers.

Opportunities for Cost-Effective Climate Action

If anything is certain in the dynamic US power industry, it is that the next ten years will continue to accelerate the changes of the 2010s. Technology shifts, changing demand patterns, climate policy, and stress from climate change are already reshaping the grid and show no signs of slowing.

Today, utilities, regulators, and policymakers have a unique opportunity to seize the opportunity inherent in these trends, unlock economic competition, and realize immediate cost savings and carbon reductions. Our new reports show that continued coal retirement and modernized, competitive procurement can set the stage for the power sector to lead America’s decarbonization, while reducing customer costs and maintaining reliability.

However, if we fail to respond to clear industry shifts, we will set back the power sector, and hamper US progress toward meeting the climate challenge in this decisive decade. At this unique moment, America cannot afford to delay action.

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.