Learn how we are working to transform how we use and produce energy.

Net-Zero Commitments: The US Financial Sector Weighs In

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

In the years since the 2015 Paris Agreement, net-zero or “climate-alignment” commitments have spread rapidly across financial sector, with the trend recently gaining considerable momentum in the United States. Since fall 2020, we’ve witnessed a wave of commitments by several US financial heavyweights, with Bank of America, Citi, Goldman Sachs, and Wells Fargo all announcing their commitments within the past month alone.

Yet this new context also brings unique market, legal, and regulatory challenges to making and implementing commitments. Understanding these challenges and their solutions will be critical for advancing climate-alignment efforts both in the United States and globally.

In December 2020, RMI’s Center for Climate-Aligned Finance, with support from the UK Foreign, Commonwealth, and Development Office (FCDO), and in partnership with the Carbon Trust, held a series of workshops with US banks and institutional investors on net-zero lending and investing. Participants represented nine banks—including three regional or mid-tier banks and six large, global banks—nine asset managers, and an asset owner.

Here’s what we learned.

From Managing Risk to Influencing the Real Economy

Our workshop participants noted that recent climate–alignment commitments mark a noteworthy shift from financial institutions’ long-established role of managing risks (climate or otherwise) toward a more proactive role in supporting decarbonization goals. In the words of one banking participant: “There’s a role for banks that provide capital and information to the market, to help meet the end goal of not going past science-based thresholds.”

These perspectives recognize a financial institution’s ability—and even responsibility—to influence the real economy in line with climate goals. Although questions remain around how influence is defined and measured for different types of financial institutions, this shift is potentially game-changing: it positions the financial sector, one of the largest and most important facilitators of our economy, as an active part of the climate solution.

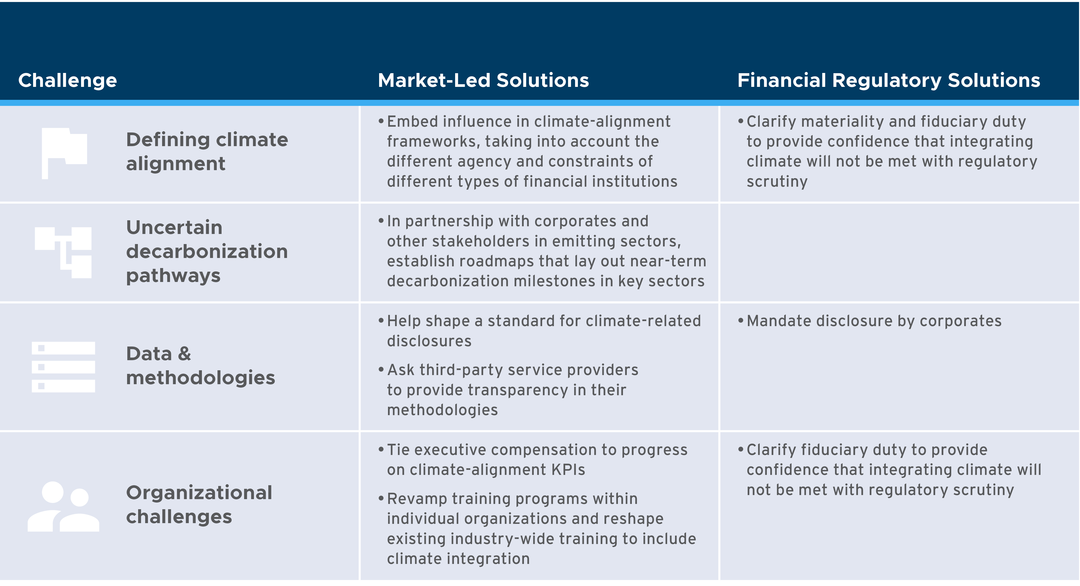

However, to help financial institutions wield this influence, workshop participants explained that US financial regulators should remove barriers to integrating climate objectives into lending and investing decisions. For example, several investor participants pointed to a ruling from the US Department of Labor’s Employee Retirement Income Securities Act (ERISA) as a potential barrier to climate alignment. In October 2020, the Department of Labor limited the fiduciary duty of investors managing ERISA-regulated funds to solely financial objectives. Though recently overturned, at the time of the workshop, US fiduciaries pointed to this example to explain the importance of having a clear definition from regulators of fiduciary duty as it relates to climate factors, as well as assurance that integrating climate into investment decisions would not be met with regulatory scrutiny.

Co-Building a Blueprint for Decarbonization

In order to effectively influence the real economy, financial institutions need to understand how real economy sectors must transform to meet climate goals. Of course, financial decisions always contain some level of uncertainty, but the particular challenge stemming from climate change is one of knowing (and publicly promising) where you must end up without a clear route for getting there. For a financial institution, it means translating long-term 2050 climate targets into timelines and terms that can inform lending and investing decisions today.

The inherent uncertainty around which pathways the world might take to a net-zero future creates a universal challenge. But workshop participants described this challenge as particularly acute in the United States, which lacks a track record of strong industrial policy and other top-down policymaking.

In the absence of policy, participants recognized they could hold dialogues with companies to agree on an emissions pathway, or a roadmap and milestones for decarbonizing key sectors. This blueprint for what needs to happen to reach net zero in different sectors is critical for informing engagement, product offerings, and other decision-making.

As one investor explained about their engagement activities, “Investors need to tell companies what they can do right, and not only what they are doing wrong.”

A Mandate for Climate-Related Disclosure

Beyond an understanding of decarbonization pathways, quality and consistent data are needed to form the bedrock of climate-aligned decision-making. Participants, both banks and institutional investors, expressed widespread support for mandatory climate-related disclosure from a body like the US Securities and Exchange Commission. This mandate, which would hold companies accountable for accurate and comprehensive climate reporting, would provide US financial institutions with the quality and legal assurance necessary to integrate climate-related data into financial decisions. This would be especially critical in light of the legal and reputational challenges financial institutions can face in the United States by making decisions based on unverified data.

Although many participants supported mandatory disclosure against a common standard, they stressed that such a standard must be informed by the market to ensure it prioritizes decision-useful information.

Changing an Institution’s DNA

In order to truly create the holistic change that climate alignment promises, climate factors must be integrated into all facets of financial decision-making. This requires evolution for all business units, functions, operational infrastructure, and even the culture within an institution—a task one participant likened to “changing the DNA” of an organization.

Though not an easy undertaking, participants cited executive and leadership buy-in on climate as a precursor to meaningful progress and suggested this could be incentivized by tying executive compensation to progress against climate–alignment KPIs. In addition to top-down leadership, participants highlighted the need for bottom-up internal capacity-building—both by revamping training programs within individual institutions and by working with industry bodies to reshape existing industry-wide training on climate topics.

When it comes to changing culture, there is no quick and easy fix. However, institutional investor participants again raised the issue of fiduciary duty and suggested that explicitly including climate within the definition of fiduciary duty could help provide fiduciaries the confidence to start reshaping internal cultures.

Conclusion

Across both workshops, participants highlighted the need for climate-alignment efforts to support financial institutions in moving beyond managing climate as a risk, and toward solutions that proactively place climate as an objective. All participants emphasized that stronger legislation on climate change is needed to bolster their efforts. But the range of solutions we heard during these sessions indicates that there are areas where the financial sector—supported by clear, enabling financial regulation—can make progress today.

Related Insights

Improving Energy Transition Assessments with Regional Pathways

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.