Learn how we are working to transform how we use and produce energy.

The Heat Is On: Decarbonizing Industrial Heat in India and Southeast Asia

Third Derivative’s startups can support a portfolio of solutions to lower carbon emissions from heat-intensive industries in rapidly urbanizing regions.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

The global industrial heat problem and opportunity

Industrial heat is an integral part of our lives. It is used both in the production of everyday products in the food and beverage, paper, pharmaceuticals, beauty, and textiles industries, as well as to power the cement kilns, steel furnaces, and chemical plants that build and sustain modern economies. However, the high temperatures (over 500°C) required for many heavy industrial processes have historically only been achievable through the combustion of fossil fuels. Even lower- and medium-temperature industrial processes, which can readily be met with electrified technologies available today, have traditionally relied on fossil-based technologies. As a result, industrial heat accounts for 14% of global CO₂ emissions today, equivalent to all the emissions from road passenger transport, aviation, and shipping combined.

Global construction, a primary driver of cement and steel demand, is projected to add 2.6 trillion square feet of new floor area by 2060, equivalent to building another New York City every month for the next 40 years, driven largely by rapid urbanization in the Global South. Meanwhile, the chemical sector, which already produces 719 million tons of product annually, is projected to grow 46% by 2050.

With the global population set to reach nearly 10 billion by 2050, food production will need to increase by 70%. This population growth, along with additional factors like an increase in disposable income, will drive significant growth in other light industrial sectors like textiles, which is expected to double or triple production by 2050. Major end users of chemical manufacturing outputs like beauty and pharmaceuticals are also set to see massive demand growth as the world faces not just an expanding population but an aging one. As these sectors rapidly expand, industry is projected to become the largest source of global greenhouse gas emissions by 2040.

Today, the global industrial heat market is valued at approximately $900 billion. By 2030, rising demand will push it past $1 trillion. This growth will be particularly pronounced in India and Southeast Asia, home to booming economies, rapidly expanding cities, and industrial sectors that will shape the global climate trajectory.

The opportunity in India and Southeast Asia

Decarbonizing industrial heat is a global challenge, but regions like India and Southeast Asia that face massive, rapid urbanization and industrial expansion offer uniquely compelling investment and emissions reduction opportunities.

Explosive growth drives demand for greater industrial production: GDP and urban population growth are driving increases in demand for energy and industrial commodities. From 2024 to 2030, nominal GDP in India and Southeast Asia is expected to grow by 73% and 42%, respectively, compared to the global average of just 30%. Urbanization will add hundreds of millions of new city dwellers, driving demand for cement, steel, textiles, and chemicals. India, for example, is expected to see a particularly massive rural-to-urban shift, doubling its city-dwelling population by 2050. With 70% of India’s urban infrastructure that will exist in 2050 yet to be built, total cement production capacity in India is expected to make up nearly one-third of global capacity by 2050.

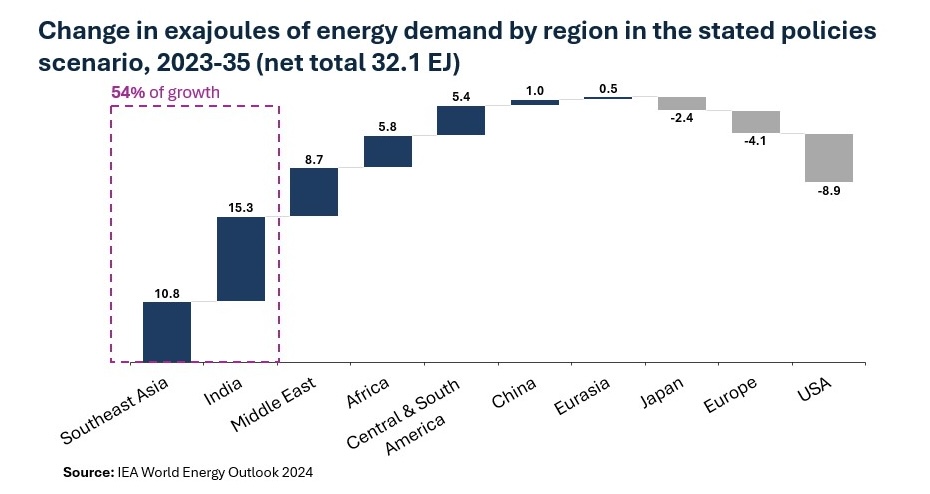

Over the next decade, India and Southeast Asia will be responsible for over half of the growth of overall energy demand, in contrast with falling demand in developed nations. Third Derivative estimates that due to these changes, the industrial heat market in Southeast Asia and India will increase two to three times by 2050, growing from about $130 billion today to as much as $400 billion in 2050. A silver lining is that as new production capacity is increasingly required to meet growing demand, it opens the possibility of deploying newer, cleaner, more efficient technologies and economies in the Global South.

Policy and export pressures create positive momentum toward climate alignment: Countries in the region are rolling out various carbon policies. Singapore’s carbon tax was the first carbon pricing mechanism in Southeast Asia, launched in 2019, with carbon tax rates set to increase to at least ten times the initial rate by 2030. India plans to implement compliance for its carbon trading scheme later this year. Meanwhile, Indonesia is taking a hybrid approach with a carbon market that will eventually transition into a “cap-tax-and-trade” system.

These countries are also developing industry-specific roadmaps for hydrogen, steel, and ammonia, and strong green power deployment plans. India alone plans to build around 500 GW of renewable energy by 2030, up from 175 GW today. Corporations in India are also taking climate action to improve their environment, social, and governance (ESG) records, which is key to accessing global capital markets. Meanwhile, export-dependent sectors such as steel and chemicals face pressure from EU carbon border adjustments, thereby accelerating decarbonization.

Additionally, international supply chains in the broader region can influence markets in India and Southeast Asia. As Southeast Asia’s largest trading partner and a major investor in the region’s development, China anchors supply chains across steel, chemicals, machinery, and manufactured goods and provides clean technologies, thereby playing a critical role in advancing low-carbon industrial transitions across the region. In recent years, industrial electricity demand growth in China outpaced industrial value added, indicating a shift toward electrification. Nearly half of electricity demand growth in the country from 2022 to 2024 came from industry. China also accounts for the largest share of global heat pump installations, reflecting large-scale deployment of electrified heating technologies. For manufacturers in India and Southeast Asia embedded in China-centered supply chains, this creates a clear opportunity to accelerate the adoption of electrified industrial heat technologies already being deployed at scale.

Energy security is another factor that can drive climate-aligned technology adoption: India and Southeast Asia rely heavily on imported fossil fuels, creating cost volatility and strategic risk. For example, 58% of Thailand’s total primary energy supply in 2023 was met by fossil fuel imports, a 133% increase from 2000. As these imported fuels are converted into usable energy, they typically incur conversion losses of roughly 60%, meaning a significant share never translates into productive output. With industry’s outsized energy use, 16% of Thailand’s primary energy supply takes the form of fossil fuel imports used specifically for industry.

In Vietnam, where net energy imports have increased by 479% since 2000, fossil fuel imports used for industry similarly make up 17% of the primary energy supply. Clean heat solutions powered by domestic renewables, biomass, or recovered waste heat are increasingly attractive hedges that enable energy independence by reducing reliance on fuel imports that suffer significant system-wide energy losses.

Rapid deployment of new fossil assets to meet this growth, along with long-expected lifetimes, creates a “now-or-never” moment to avoid locking in climate pollution, fuel price volatility, and import dependence: This growth is being front-loaded, meaning decisions made in the next five to ten years will shape emissions for decades. The average cement kiln, blast furnace, or fossil boiler built today will still be running in 2050. While this surge poses a climate risk, it also serves as a market beacon; regions with high demand growth can leapfrog over incumbent fossil assets and meet this demand while deploying more efficient, low-emissions technology to decarbonize industrial heat.

This is demonstrated clearly by India’s steel and cement industries. As the world’s second-largest producer of steel and cement, India’s output is projected to double by 2030, and may increase by up to three to five times by 2050 due to growing domestic demand. The result is that industrial assets being built today will be responsible for the majority of production and emissions by 2033. Without immediate intervention to deploy low-carbon technology to address both process and heating emissions, there is a risk of locking in a heavily polluting trajectory for decades to come.

Emissions reduction is not the only reason to avoid locking in fossil assets. Newer, lower emissions technologies often provide additional co-benefits: industrial facilities benefit from more efficient resource use or higher quality product outputs, and surrounding communities benefit from reduced local air and water pollution.

Opportunity landscape: A portfolio of solutions

Decarbonizing industrial heat won’t happen with a single technology. Different industries require different temperatures, with textiles and food processing requiring mostly low to medium grade (<500°C) and cement and steel requiring mostly high grade (500°C to 1,600°C). The breakdown of heat demand in Southeast Asia and India aligns with the global trend, with roughly half low- to medium-grade and half high-grade.

Even within sectors, there is no single technology that will be ideal for every industrial site or process. For example, heat requirements in the chemicals sector are fairly evenly split between low-, medium-, and high-grade heat due to the variety of processes involved across a complex value chain. It will be imperative to leverage the entire renewable thermal toolkit, with solutions across electrification, clean energy, and alternative fuels.

Although electrification is the primary vector for industrial heat decarbonization, solar thermal and geothermal can play a supporting role in select applications, such as when co-located project development is possible or when electrification alone cannot reach the temperatures required. Renewable fuel technologies, such as hydrogen and biomass, could also have a meaningful near-term impact on decarbonizing existing assets in regions that are developing lower-cost green hydrogen or that have abundant waste biomass, the latter of which is prevalent across India and Southeast Asia. India, in particular, is showing enthusiasm for biomass technology in industries like steel and cement, although global applicability for these sectors is generally lower as supply constraints for consciously sourced waste biomass limit practical and effective use cases.

Last year, Third Derivative and RMI launched two industrial initiatives: 1) the Industrial Innovation Cohorts, focused on supporting groundbreaking startups in the cement, steel, and chemicals sectors, including cross-cutting solutions like industrial heat; and 2) the Future Industries Partnership, which builds on the foundations of the Industrial Innovation Cohorts with a specific focus on deploying solutions across Asia and the Middle East, where industrial growth and rapid urbanization are driving urgent demand for scalable, low-carbon technologies. Through the process of developing robust technical investment theses, Third Derivative assessed a suite of industrial heat technologies to support decarbonization across industrial sectors, including heat pumps, thermal batteries, direct electrification, and waste heat recovery.

Heat pumps

Heat pumps are the most energy-efficient solution for low-temperature industrial heat. Heat pumps move energy, rather than create it, by capturing small amounts of heat from a nearby source (e.g., air, ground, waste heat) in a refrigerant and then compressing the refrigerant to raise the pressure and thus the temperature. This allows heat pumps to achieve efficiencies ranging from 200% to 500% and beyond. This means that for every one unit of electrical energy input the system consumes, it produces two to five units of heat energy output. Fossil-powered boilers typically have efficiencies around just 80%, while electric boilers are limited to 100% efficiency.

Today, heat pumps are widely available for hot water and steam up to 120°C, and there are emerging solutions being piloted capable of 200°C. AtmosZero’s heat pump is capable of producing steam up to 153°C (standard) or 165°C with a compressor upgrade. It is currently being used in the food and beverage, chemicals, and pharmaceuticals sectors. Current heat pump designs are expected to soon be able to reach up to 225°C. Future designs could theoretically be coupled with other low-carbon thermal sources to upgrade low temperatures to the high heat required for many industrial applications.

Waste heat recovery

Waste heat recovery can be used to generate clean electricity or enhance the efficiency of renewable thermal solutions. Roughly 35% of all industrial heat is wasted, for several reasons. First, waste heat is relatively low in temperature and thus not always useful in many contexts. Second, technologies like heat pumps that can actually recover and utilize heat waste effectively didn’t mature or fall in cost until relatively recently. Lastly, fossil fuels were relatively cheap for a long time, meaning there was a lack of economic pressure to conserve or recover heat.

Today, there is both the technological capability to recover and utilize waste heat and an incentive to do so. Skyven’s Arcturus system captures low-temperature waste heat from industrial processes, upgrades the temperature via heat pump, and uses it to generate steam comparable to that of existing boilers. Advanced Thermovoltaic Systems is deploying a modular, solid-state heat-to-power system applicable to waste heat in the 150°C to 500°C range, with the ability to capture waste heat from previously unavailable sources like cement kilns.

In the cement, steel, oil and gas, and power sectors in Asia, there are roughly 925 terawatt-hours of recoverable waste heat that can be used by renewable thermal solutions like heat pumps and thermal batteries to improve efficiency and project economics. Alternatively, this heat can be used to produce electricity that can cover on-site electricity demand and lower bills, often with rapid payback periods.

Thermal batteries

Thermal batteries are a versatile solution for a wide range of industrial process heat requirements. Thermal batteries charge using off grid renewable energy and/or cheap, excess renewables from the grid during hours of the day when it would otherwise be curtailed. They can then store heat up to 1,800°C for hours to days to deliver clean heat 24/7 at a variety of temperatures.

Today, initial installations are delivering heat up to 400°C. Some startups have begun pilots targeting up to 1,000°C, although delivering heat at higher temperatures draws down the stored energy much faster. As cheap renewable electricity becomes more available and technical advancements are made in high temperature heat transfer, thermal batteries could eventually target process heat delivery of 1,200°C or higher as challenges around material degradation and heat delivery at higher temperatures are solved, making them applicable as a primary energy source for cement and steel production. Several startups are advancing this technology, with some like NOC Energy and Kraftblock focused on delivering ultra-high temperatures (1,300°C to 1,500°C) and others like Antora and Cache Energy focusing on long-duration storage, delivering medium-grade heat that can be stored for over 100 hours.

Electrification

Direct electrification solutions are being developed specifically for high-temperature heat requirements in cement, steel, and chemicals, including resistance, plasma, induction, dielectric, and turbine-based heating.

Resistance heating is used by many thermal battery startups to charge their storage materials. Companies like HyperHeat are developing advanced resistance heaters capable of producing heat up to 2,000°C by using specialized materials like oxide ceramics, which are known for their strength and thermal stability.

Plasma heating uses electric arcs to ionize gases such as oxygen or nitrogen up to 20,000°C. While electric arc furnaces are commonly used in steel manufacturing, companies like SaltX Technology are developing similar methods for cement.

Induction heating, which uses electromagnetic fields to heat electrically conductive materials from within, has been used in some industrial applications for many years now. Companies like NOC Energy are adapting this technology for thermal storage and direct electrification for high-temperature process heat up to 1,500°C.

Dielectric heating, which is the same technology used in microwaves, uses high-frequency electromagnetic fields to heat insulating materials. Sun Metalon uses this technology to enable the recycling of contaminated or non-ideal scrap metal with near-zero emissions.

Turbine-based heating, which converts rotational energy directly into thermal energy, is being piloted for high-temperature heat in the cement, steel, and chemicals sectors. Kanin Energy uses turbines for their waste-heat-to-power solutions in a variety of industrial applications.

Innovation insights

Third Derivative has engaged closely with founders, corporations, and investors focused on industrial decarbonization through the Future Industries Partnership and Industrial Innovation Cohorts, including through moderating events such as the recent industrial heat panel at the SCALE conference in Mumbai, an expo for global climate tech start-ups. Through this work, Third Derivative has been able to hear directly from the industrial ecosystem about some of the market dynamics and commercialization challenges shaping the way industrial heat startups scale in India and Southeast Asia.

Corporations in the region are already chasing low-hanging fruit, such as energy efficiency upgrades and heat pumps for low-temperature applications. In 2022, for example, DCM Shriram installed a steam-generating heat pump developed by TRIGeN DC at its sugar plant in Hariawan, India, to demonstrate the technology, which provides low pressure steam at 110°C. Credence Cleantech highlighted at the SCALE panel a demonstration project providing 150°C heat from solar thermal to a food processing plant. Although the technology is capable of reaching 500°C, there are additional technical risks, such as in the receiver, the storage medium, and the reflectivity of the mirrors.

In many cases, especially for low- to medium-grade heat, solutions such as heat pumps and solar thermal are already economically viable today. High-grade heat is more challenging to fully decarbonize, but corporations at the SCALE panel expressed increasing excitement around engaging with emerging solutions like biomass and more novel technologies.

While corporations in the region have an appetite for collaboration, they are still determining their risk tolerance. Corporations in the region have expressed a strong desire to be collaborative, see more solutions from startups and innovators, and even co-develop solutions starting from the research and development level. For example, UltraTech in India is implementing waste heat recovery systems and CoolBrook’s low-carbon cement production technology, along with collaborating with IIT Madras to develop appropriate carbon capture solutions for their process.

However, the regional startup ecosystem as a whole is relatively nascent, with climate tech innovation even newer, so corporations are still solving questions around how to engage with innovators. This is especially true for large capital expenditure first-of-a-kind (FOAK) projects that do not have a clear, immediate business case either through additional near-term revenue or significant cost savings.

This presents a great opportunity for international philanthropies to have an outsized impact by deploying catalytic FOAK financing, including risk transfer instruments such as reinsurance or loan guarantee funds, or by sponsoring intensive project development support, like what Mark1 is doing in the US context. Mark1, a developer-as-a-service spun out by RMI, Third Derivative, and Deep Science Ventures, was created to address the gap between technology development and project deployment by helping startups co-develop their first commercial-scale projects. This model provides structured support across engineering design, offtake contracting, capital strategy, regulatory pathways, and early engagement with financial partners to structure the deals. Such targeted support in India and Southeast Asia can be leveraged to build momentum for global decarbonization.

Sustainability commitments matter to customers, but they won’t compromise on the financial bottom line. Corporations have told Third Derivative that they want to provide the highest quality product to their customers at the lowest possible cost and the lowest possible environmental footprint. However, coal remains cheap in India and Southeast Asia, creating economic headwinds for alternative technologies. With limited financing for small and medium enterprises and engineering and geographic barriers complicating deployment, early-stage technologies can struggle to be cost-competitive.

Startups that can provide immediate economic benefits to customers are best positioned for early adoption. Kraftblock, for example, installed a waste heat recovery system with thermal storage to utilize flue gas from sinter cooling at a Tata Steel plant in Jamshedpur. This system will eliminate roughly 110 gigawatt-hours of fossil fuel use every year, saving money and about 22,000 metrics tons of carbon dioxide. It is also anticipated to increase productivity and stabilize operations of the plant during power outages. The financial and operational benefits of this project, combined with the very short payback period of less than two years, create a compelling case study for industrial heat deployments.

Innovative financial models go hand in hand with innovative technologies. While the technology toolkit is broadening, the financing toolkit is just starting to catch up. The heat-as-a-service model shifts industrial heat from a capital expense to an operating expense: providers finance, install, and maintain equipment, and customers pay over time based on performance. For example, Skyven deploys electric steam-generating heat pumps with no up-front cost to manufacturers, aligning repayment with energy savings and emissions reductions. Book-and-claim systems separate the environmental attributes of low-carbon materials or fuels from the physical product, allowing buyers to purchase and claim emissions reductions even if the cleaner product is not physically delivered to them. RMI and partners are already deploying book-and-claim frameworks for heavy industry, including cement (Sustainable Concrete Buyers Alliance), steel (Sustainable Steel Buyers Platform) and aviation (Sustainable Aviation Buyers Alliance), to help aggregate demand and accelerate early markets.

RMI is also exploring novel financing mechanisms such as virtual industrial heat purchase agreements. Modeled on other virtual power purchase agreements that help unlock corporate renewable energy procurement, this contract-for-difference approach could help manage electricity price volatility and close the “spark gap” between electric and fossil-based heating.

The large market opportunity in India and Southeast Asia combined with corporate appetite for innovation presents the chance for this region to lead on decarbonization. A diversity of startups in the region are stepping up to meet the moment, building technology that is both suited to the regional context and global application. With targeted support, the innovation ecosystem in this region can serve as a launch pad for new technologies to rapidly commercialize and scale to support global decarbonization.

The authors would like to thank Alexander Hogeveen Rutter and Chetan Krishna for their contributions to this article, and Global Industry Hub and HSBC for their generous funding of Third Derivative.

Related Insights

Scaling the Next Generation of Industrial Climate Solutions

How Southeast Asia’s Low-Emission Chemicals Sector Can Expand

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.