Learn how we are working to transform how we use and produce energy.

How Much Does Storage Really Cost? Lazard Weighs In.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

In November 2015, financial advisory firm Lazard released its first-ever Levelized Cost of Storage Analysis (LCOS). Well known for its Levelized Cost of Energy Analysis (LCOE) analysis—now out in version 9.0—Lazard publishing an analysis of storage is a major sign that it considers battery energy storage a critical technology that’s here to stay. But a closer look at Lazard’s LCOS shows something RMI’s October 2015 Economics of Battery Energy Storage report noted: a) battery economics are usually evaluated on the basis of single-use cases, b) stacking multiple uses can greatly enhance battery economics, and c) evaluating those economics gets difficult quickly. It’s the use cases and stacked value streams—in addition to per-kWh cell cost declines—that offer tremendous opportunity.

RMI’s report primarily looked at the value, not cost, of a basket of multiple, stacked uses for customer-sited storage systems. Lazard focused on the costs of several physical storage technologies (including the lithium-ion studied in RMI’s report) and not “alternative” storage options such as building-as-storage, water heater-based storage, and other demand flexibility options. It evaluated those storage technologies on the basis of a variety of single-use cases such as frequency regulation and peak shaving/demand charge reduction. Lazard compared those costs to conventional, fossil-fuel alternatives.

Jesse Morris, a manager at RMI and co-author of RMI’s battery report, says, “We did not make this comparison in our Economics of Battery Storage report for a number of reasons but Lazard’s analysis is a great first step. It adds to a strong foundation from which the industry can better understand multiple-use cases.”

Morris adds, “In the end, this is the comparison that we need to be able to make if we’re going to convince regulators that a distributed energy resource-focused future is a lower-cost alternative.” Batteries are tricky to evaluate in part because they aren’t strictly a demand- or supply-side solution. They’re an arbiter of supply and demand, serving as either generation or load depending on whether they’re discharging or charging. So the favorable finances of storage can use all the clarity and all the study they can get.

SHIFTING FROM SINGLE- TO MULTI-USE CASES

The LCOS examined single-use cases, which is how most batteries are deployed today. But single uses are not how RMI proposes (or how Lazard expects) they be deployed in the future. Batteries today are used for a minority of their useful lifetimes. They can do much more than sit idle the majority of the time, and increasing their utilization rate can greatly enhance the value they provide to customers and the grid.

Jonathan Mir, managing director and head of North American Power and Utilities at Lazard, says, “In point of fact, it will be possible to use batteries for more than one thing, which means their value is higher than is being captured in our study.” Lazard advanced the practice of computing costs for renewably generated electricity with their LCOE series and Mir says, “I think we’re going to have to do the same thing around the stacked use cases.”

STORAGE COSTS ARE DROPPING

Both reports find that the age of the battery is here, largely because costs have dropped so far, so fast. Mir says, “This reminds us very much of where utility-scale renewables were seven or eight years ago,” when Lazard began covering renewable costs in its LCOE series. “To us, this seems like an inflection point where you can see external factors causing demand to really take off and then you wind up with price declines as manufacturing scales up,” he says. Lazard’s analysis also predicts significant cost declines over the next five years, based on a survey of industry experts. For example, the median expected five-year price decline for lithium-ion storage is 47 percent below today’s costs.

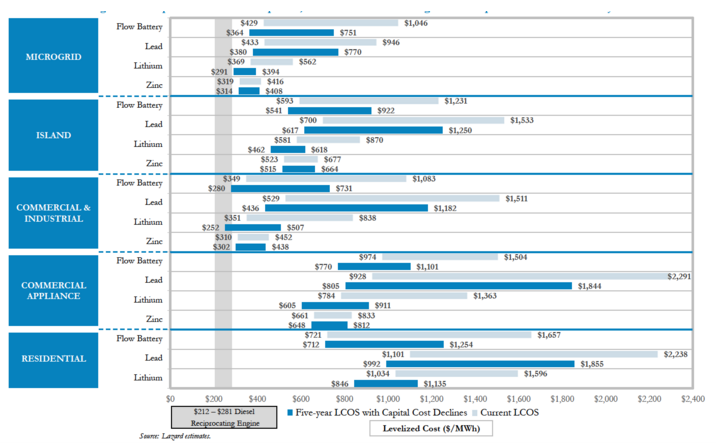

The LCOS calculates the costs of eight different energy storage technologies for ten single-use cases, half behind the meter (including augmenting residential solar PV) and half in front (including transmission-upgrade deferral). It compares these to the costs of conventional alternatives like natural-gas peaker plants or diesel generators. The study finds that the costs of storage are within “striking distance” of conventional alternatives for many single-use cases, including lithium-ion batteries used for frequency regulation and flow batteries used to defer adding a new peaker plant.

THE CHALLENGE OF MULTI-USE ACCOUNTING

What the LCOS analysis doesn’t do is estimate the cost of energy storage when it is utilized for multiple, stacked services, a key to realizing the value of storage to customers and the grid.

Most of storage’s costs are fixed, capital costs. But variable costs—as well as battery lifetime, potentially capacity loss over time, and ultimately replacement—depend on the use or uses to which a battery is put over its lifetime, especially how often it is charged and discharged. This makes it difficult to state the cost of a given storage technology for a variety of multiple, stacked services. “That is our ambition,” says Lazard’s Mir. “It’s important to capture, because we think our study is likely underestimating the value and potential of storage because storage would be used in more sophisticated ways than are being illustrated,” he says, “but the quantitative analysis and framework to illustrate that is still being developed. It is another indicium of how immature the industry is.”

Evaluating battery energy storage economics is hard, and RMI sees opportunities to build on Lazard’s commendable start. The basic problem is finding a levelized cost that can be added in as services are stacked in different combinations. Garrett Fitzgerald, a senior associate at RMI and co-author of the Economics of Battery Energy Storage report, explains that, “by combining fixed costs and variable costs—that are determined by what services and how often they are being provided—you end up with a total lifetime cost of providing just a single service. It is not possible to then determine the incremental cost of stacking other services on.” For example, “It would be incorrect to simply add the LCOS of frequency regulation and the LCOS of peaker replacement as an estimate of the LCOS of a system providing both,” says Fitzgerald.

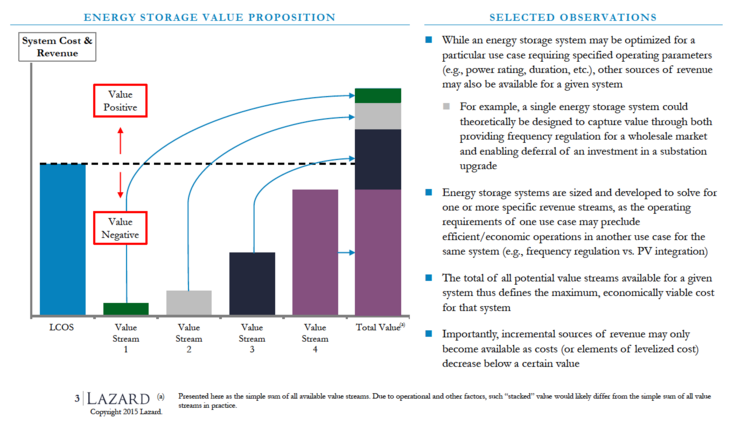

THE IMPORTANCE OF VALUE STACKING

Establishing a framework to measure the value (and cost) of stacked use cases for storage should be possible. Mir says, “To us, that is a natural evolution of the study.” But, he notes, “We have not seen a good solution in the public domain for how to demonstrate this idea, so we will come up with a framework. We understood it as a very important qualification to the work we were doing,” says Mir, “which is why we tried to be so clear about it.”

Indeed, the third page of the LCOS is devoted to explaining exactly how the energy storage value proposition depends on the stacking of multiple uses and adding together the value streams they create. RMI’s Morris says, “Their description is very clear and an excellent way to think about the comparison between stacking values and comparing different stacks of value to a given cost.”

THE CURRENT STATE OF PLAY

Lazard considered only unsubsidized costs and disregarded the additional value created by such things as avoiding the toxic or climate-changing emissions of conventional fossil-fueled technologies. Nor does Lazard take into account state incentives, such as California’s SGIP and mandatory battery storage legislation. “Their comparison of all chemistries performing all use cases against a gas peaker plant or a reciprocating diesel engine (depending on the application) is extremely helpful,” says Morris. Should subsidies for storage be introduced at the national level, Lazard will factor them in the same way it does for LCOE.

So what did Lazard find? Of all the permutations analyzed, only one—lithium-ion batteries providing frequency regulation to the grid—was cost effective when performing a single, unstacked service today. The study also predicts that seven combinations (all of them with batteries) will be cost effective within five years. These include two use cases—peaker replacement and industrial peak shaving/demand charge avoidance—for which multiple battery chemistries will be cost-competitive with their diesel and natural-gas alternatives.

The LCOS does contain this encouraging caveat, however: “a number of [technology and use case] combinations are within ‘striking distance’ and, when paired with certain streams of value, may currently be economic for certain system owners in some scenarios.” It is these combined value streams that come with stacked uses that need to be accurately and easily accounted for.

THE ROAD AHEAD

“Costs will come down naturally with scale; they always do,” says RMI’s Fitzgerald, but he cautions that, “storage won’t be mainstream until there are more channels for developers or storage owners to find revenue.” As examples of the new channels being opened up for storage, he cites, “things like aggregated wholesale market participation in California or distributed system platform providers as described in New York’s REV proceeding.”

Fitzgerald says that, “storage can do a lot for the grid, and it can do most when behind-the-meter. Regulation is changing that will allow distributed storage to collect revenue for these services.” In consequence, he says, “most of the industry is focused on opening up new revenue streams and moving toward customer-sited and customer-focused services, such as demand charge management or solar-plus-storage solutions.” Lazard’s Mir adds, “We see that demand increasing pretty rapidly.”

Top photo courtesy of Thinkstock. Graphs courtesy of Lazard. Used with permission.

Authors

David Labrador

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.