Learn how we are working to transform how we use and produce energy.

Stacking Rules, Bonus Credits, and the Future Industrial Markets the IRA Aims to Create

Understanding the goals behind the Inflation Reduction Act’s industrial tax credit rules is essential to maximizing their impact, both at the firm and the market level.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

The Inflation Reduction Act, passed into law in August 2022, represents the largest investment in decarbonization that the United States has ever undertaken. Included in this wide-ranging bill are numerous tax credits, bonuses, and stacking rules that specifically facilitate decarbonization in the industrial sector. However, the amount and complexity of these incentives and their guidance documents have generated uncertainty, and many companies are waiting for a clearer picture to emerge before acting. As a result, strategies for capitalizing on these tax credits’ bonuses and stackability have been the subject of countless webinars, policy briefs, and strategy meetings. But what often goes unmentioned is the implicit goal of the structures within the IRA: to create sustainable long-term successes for the taxpayer and for heavy industries at large. In other words, with its stackability and bonus rules, the IRA is attempting to tell a story of how to build future clean industries in the United States.

Creating New Markets: A Chicken and Egg Problem

In its essence, the IRA is attempting to create new, long-term domestic markets for clean industry. However, generating new markets is challenging because of a chicken and egg problem between supply and demand: producers don’t want to create something that no one wants to buy, and buyers don’t want to depend on a product that nobody produces — not to mention that new technologies often come with a hefty price tag compared to existing technology.

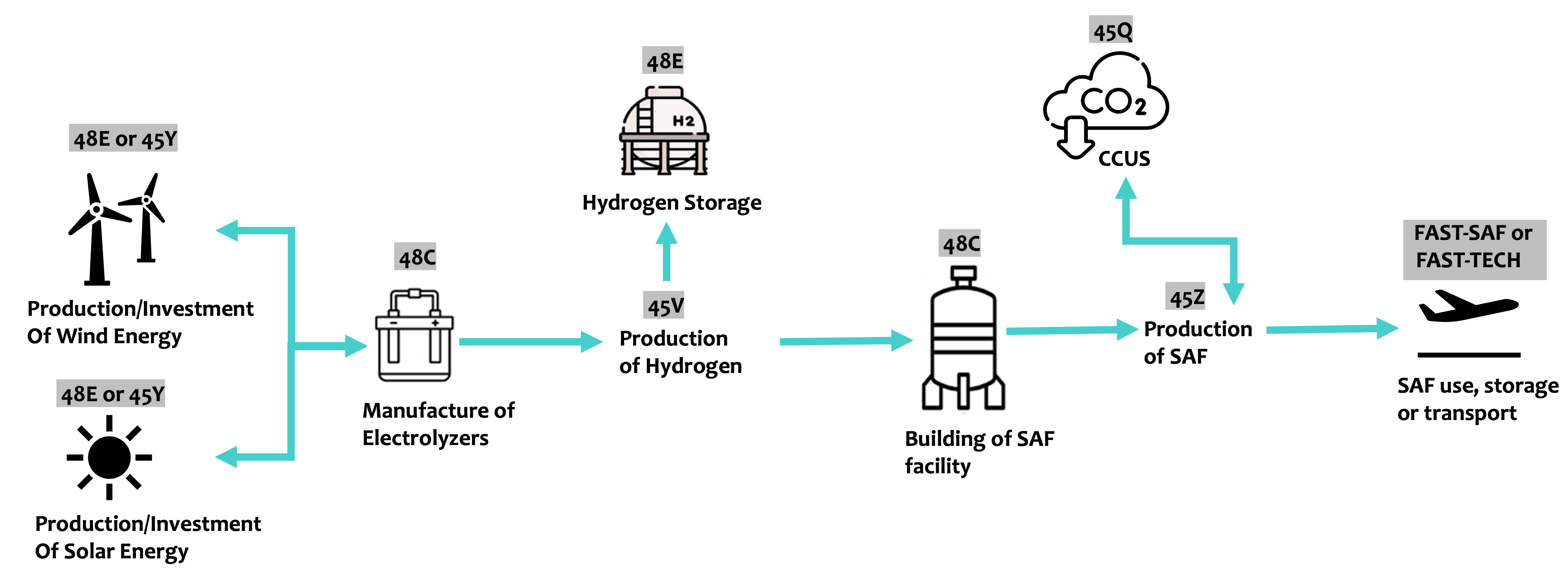

The IRA works to solve these problems by offering incentives across the value chain that interlock to activate the market as a whole. Consider aviation: Currently, the aviation fuel supply chain is a highly polluting industry that results in emissions-intensive jet fuels. While the alternative, sustainable aviation fuel (SAF), can reduce emissions by more than 80 percent there has been little demand for it due to its cost premium and lack of policy incentivizing or requiring airlines to procure SAF.

The IRA approaches these challenges by providing incentives at every step of the SAF supply chain:

- Starting with the Clean Electricity 48E Investment Tax Credit (ITC) or the 45Y Production Tax Credit (PTC): which subsidize the price of clean electricity at rates of up to $33/MWh (the PTC) or 70 percent of the investment (the ITC). (This assumes the facility qualifies for the higher base rate and both the energy community and domestic content bonuses, as well as the low-income community bonus in the case of the ITC).

- That electricity can then be routed to a hydrogen electrolyzer, the manufacture of which is subsidized by the 48C Advanced Energy Project Tax Credit.

- The production of hydrogen could qualify for the highest tier of the 45V Clean Hydrogen PTC — a whopping $3.00 per kilogram of hydrogen.

- Any extra hydrogen could be stored in a facility that receives the 48E ITC—worth 50 percent of the facility’s investment amount. The unstored hydrogen could then be sourced by a SAF production plant that combines it with CO2 to make SAF.

- Additionally, the capture and sale of CO2 is aided by the 45Q Carbon Oxide Sequestration Credit and the construction of a SAF plant qualifies for the 48C Advanced Energy Project Tax Credit.

- The produced SAF could qualify for up to $1.75/gallon under both 45Z and its precursor 40B.

- And to offtake that SAF, the FAST-SAF and FAST-TECH programs subsidize projects that transport, store, and use SAF in commercial airplanes.

For information on each of these tax credits and more, check out The Decarbonizing Industry Resources Tool.

Exhibit 1: IRA incentives along the sustainable aviation fuel (SAF) supply chain.

In this way, the IRA facilitates a completely new market and de-risks industrial decarbonization at multiple levels, taking a significant step towards solving both the chicken and egg problem and the price issue. And this narrative can be told for most of the heavy industries that plan to take advantage of IRA programs.

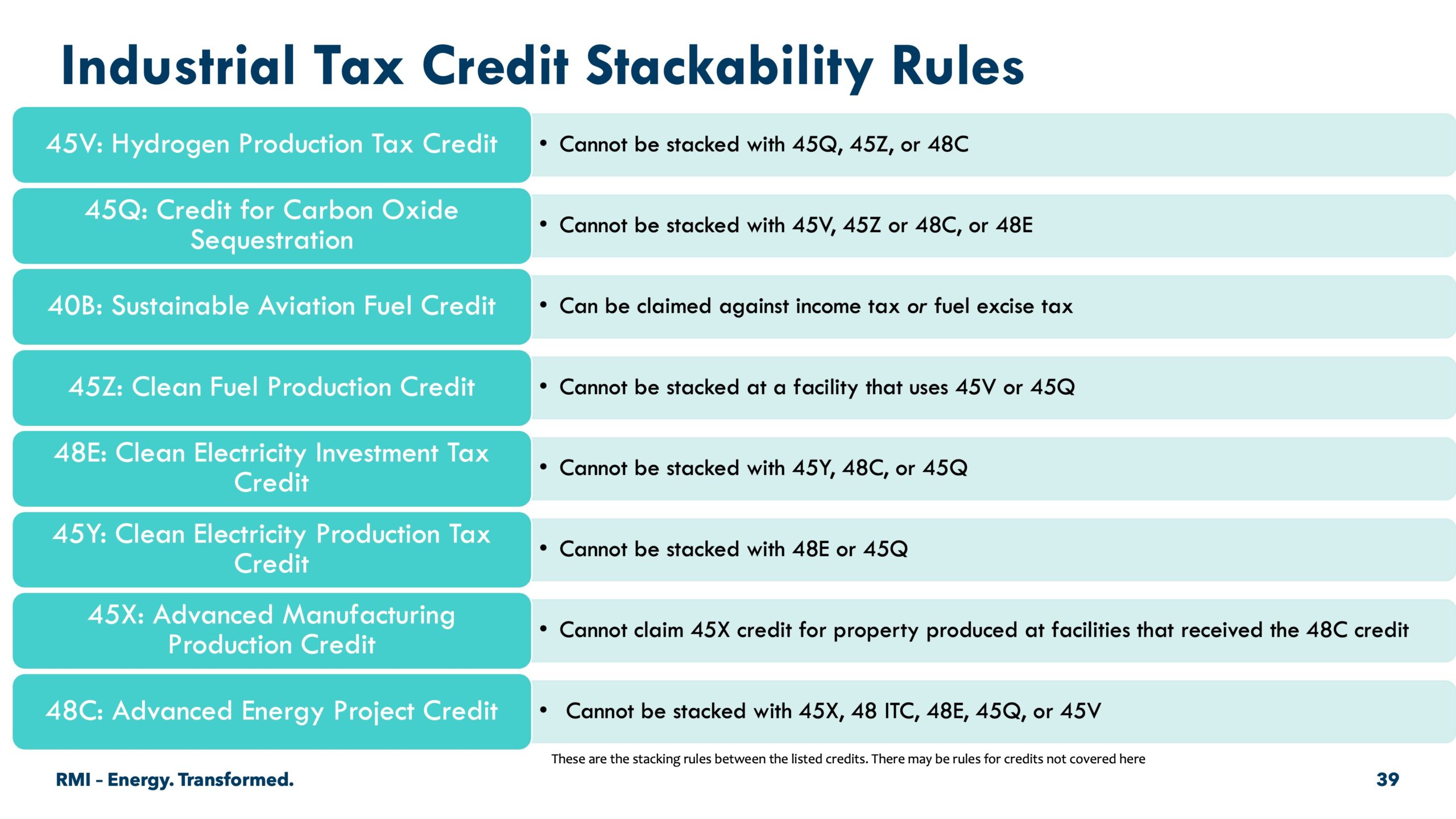

Stacking Rules: No Need for Redundancies

It’s important to note that in our story of the SAF market, different points on the supply chain are occupied by different organizations at unique facilities — in other words, some of these tax credits have prohibitions on stacking at one facility or by one company. This is because the IRA’s aim is to subsidize the various points of a new market efficiently while avoiding over-incentivization. Stacking rules work to support multiple participants of flourishing markets, and often credits that sound like they would double-benefit the same facility have prohibitions from doing just that.

This is the case for the 48C Advanced Energy Project Credit and the 45X Advanced Manufacturing Production Credit. Both credits aim to smooth the same chokepoint in industrial facility financing. 48C provides a credit for the retrofit and building of advanced energy projects, which includes facilities that manufacture components used in solar panels, wind turbines, and batteries. 45X provides a tax credit for manufacturing the very same components. Therefore, these credits may not be stacked. This is the same rationale behind the stacking prohibition on the 48Y PTC and 45E ITC, which both subsidize the production of clean electricity.

Another key stacking prohibition is that for the 45V Clean Hydrogen Production Tax Credit and the 45Q Carbon Oxide Sequestration Tax Credit. These credits were intended to support different points of the supply chain: 45V supports the production of hydrogen, which is a fuel in the production of clean cement, steel, chemicals, and other heavy industries. Carbon capture can both be part of the process of manufacturing those products (in the form of scrubbers and point source capture) as well as an input (such as in the SAF example, but also for other industrial materials as well). However, hydrogen production itself can also rely on carbon capture. By prohibiting their stacking, the IRA prevents both credits from benefiting one point on the supply chain but allows them to work in tandem at different points, separately subsidizing the fuel, process, and inputs of industrial processes instead of doubling down on the production of hydrogen. In this way, they interlock to support a healthy supply chain from start to finish.

Exhibit 2: IRA industrial credits and corresponding stacking rules.

Bonus Round: Credit Superchargers

As these new markets develop, they offer the opportunity for the federal government to steer them toward socially optimal outcomes by offering hefty bonuses for projects that check certain boxes.

One major bonus is the “prevailing wage and apprenticeship requirement”, which applies to nearly all major industrial deployment tax credits. Meeting wage and apprenticeship requirements can supercharge a credit’s worth by increasing the base rate by as much as 500 percent. In this way, the IRA can also shape new industries into equitable and forward-looking markets.

Three smaller bonuses that some credits can receive are the domestic content credit, which rewards projects that bring manufacturing jobs to America, and the energy community and low-income community bonuses, which aim to attract new projects to areas that could benefit the most from the jobs created by new industrial projects.

While it would be challenging (though not impossible) for a single project to obtain all four bonuses, each one can increase credit amounts as an incentive for new projects to direct their benefits towards underserved communities and American supply chains. In this way, tax credit bonuses are a mechanism that the IRA uses to achieve ideal outcomes for the industrial sector.

Exhibit 3: How bonuses interact with IRA credits.

The IRA’s Story is Still Being Told – And Could Be at Risk

Decisions that are being made right now about how these tax credits are worked into stakeholders’ bottom lines will determine whether these future healthy markets thrive, or if the IRA turns into a boom and bust of investment without long-term impact.

That’s why it’s crucial to encourage industrial stakeholders to see the IRA as just the first step in creating new markets. If companies pursue tax credits for their own sake without considering how new projects will feed into a broader market ecosystem, they risk creating a situation where these new markets last only as long as the IRA credits exist. This would be a huge waste of the potential that the IRA represents.

But by aligning industry goals with the goals implicit in the IRA’s structure, organizations can maximize the impact of credits and bonuses and create durable markets — which inherently leads to durable jobs. Consortiums between companies that operate across a supply chain will ensure that interlocking benefits are passed on, resulting in cheaper and cleaner goods. Investors who prioritize projects that will exist beyond the life of IRA credits can help launch permanent and lucrative new markets. And companies that earnestly pursue the bonuses for building in low-income and energy communities can simultaneously create equitable market outcomes and maximize their own benefits. Together, with greater goals in mind, the full opportunity the IRA offers can be realized to the greater benefit of all.

Authors

Jane Sadler

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.