Report Release: Headwinds for US Gas Power

Six Trends Eroding the Business Case for New Gas Power Plants

This past year was tough for natural gas in the US electricity sector. Headline-grabbing events like Winter Storm Uri and the blackouts in Texas in February—caused in large part by the failure of gas delivery and power infrastructure in extreme weather conditions—illustrated how fuel insecurity and high prices can cost consumers billions of dollars.

Amid the ongoing volatility in natural gas prices, and the continued trend of falling prices for renewable energy and storage technologies, numerous gas power projects have been canceled before commencing construction. A few high-profile cases, like the cancellation of a long-proposed gas-fired plant in Minnesota in June, illustrate a broader shift: utilities and investors increasingly prioritize clean energy as a lower-cost, lower-risk option than continued investment in new gas plants.

And yet, there remains a long tail of gas plants still proposed for construction in the United States, even as their economic prospects dim. In fact, utilities and other investors plan to invest more than $50 billion in new gas power plants over the next decade. But a new RMI study released today details how at least 80 percent of these projects could be cost-effectively avoided by prioritizing investments in clean energy instead. And a set of economic and policy trends, ranging from volatile gas prices to policy priorities around public health and job creation, threaten the viability of nearly all new gas projects.

New Gas Plants Are Losing Steam

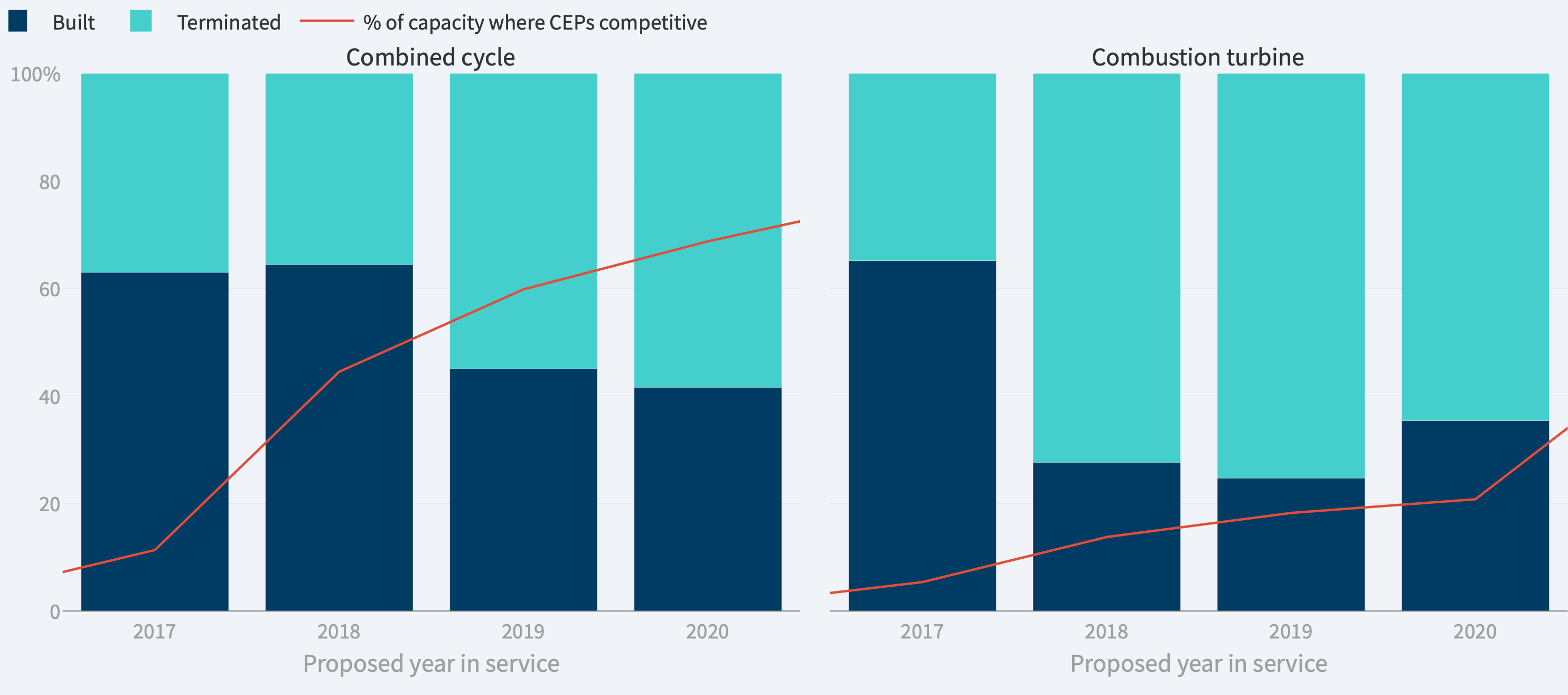

The trends have been shifting against new gas plants in the United States for several years. RMI analysis starting in 2018 documented how “clean energy portfolios”—combinations of wind, solar, energy efficiency, demand response, and battery energy storage that can provide the same reliability services as a gas-fired power plant—are increasingly economical compared with new gas plants. And since 2018, the capacity of new gas plants entering service has fallen every year, on track in 2021 to hit the lowest level since 2010.

Even more telling, over 50 percent of gas plants proposed to come online in the past two years have been canceled prior to construction as clean energy resources have become more and more competitive (Exhibit 1). This is true for restructured markets as well as for vertically integrated utilities.

Currently, new gas plants make up less than 10 percent of new capacity in interconnection queues, while renewables and storage dominate planned construction. This is reflective of shifting economics—where utilities have run modern, all-source competitive procurement processes to select the least-cost, least-risk resources to maintain grid reliability, they have overwhelmingly chosen clean energy portfolios.

Stiffening Headwinds for New Gas Power Plants

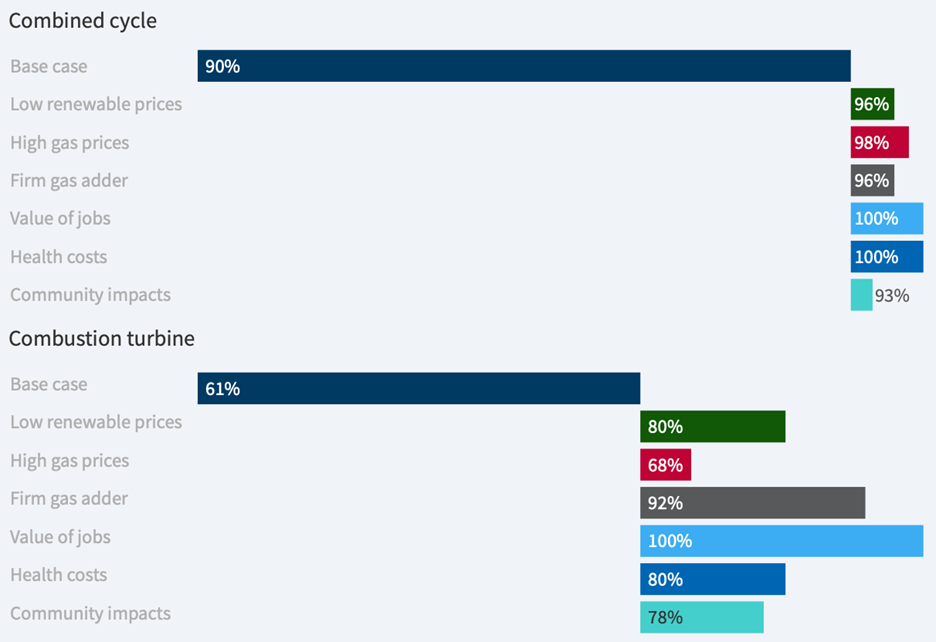

In addition to raw economics leading to gas project cancellations, a growing set of economic and policy trends threaten the viability of any new gas-fired power project proposed for construction in the United States. RMI’s study quantifies six risk factors and their impacts on the viability of new gas power plants (Exhibit 2):

- Renewable energy prices: If renewables cost declines continue at their recent pace, 91 percent of new gas plants will be uneconomic relative to CEPs at their proposed construction date.

- Gas price volatility: If gas price trajectories return to 2021 highs, 88 percent of new gas plants will be uneconomic relative to CEPs.

- Costs of fuel security: If gas plants are required to bear the cost of securing reliable fuel supply to guard against the kind of outages on display in February 2021 in Texas, 95 percent of proposed gas plants would be uneconomic.

- Focus on job creation: If policymakers continue to prioritize job creation, 100 percent of proposed gas plants are threatened, as clean energy portfolios lead to higher net job creation than new gas plants.

- Focus on human health: If policymakers account for the cost of human health impacts of pollution from new gas-fired power plants, 94 percent of new gas plants would be uneconomic.

- Reducing community impacts: If policymakers prioritize minimizing impacts to marginalized communities due to new gas plant construction and operations, 88 percent of proposed gas plants are threatened.

If proposed gas plants get built despite these growing risks, they face significant risks of losing money and early retirement well ahead of their projected lifetime. RMI’s study found that if either gas prices rise again, or renewable energy and storage costs fall at their recent pace, over 80 percent of currently proposed combined-cycle projects could face stranded cost risks within 10 years—with much of this risk ultimately passed to consumers.

A Bright New Year for Clean Energy Portfolios

Looking back on 2021, it’s increasingly clear that if natural gas were ever a “bridge” fuel to a clean energy future, we have long since crossed the bridge. Utilities and investors have largely turned toward cost-effective, clean energy alternatives that can temper high consumer costs, mitigate the impact of ongoing price volatility, and avoid stranded cost risks. And policymakers increasingly recognize that prioritizing clean energy can also help spur higher net job creation while minimizing the human health impacts, especially in marginalized communities, associated with pollution from new gas plants.

Looking forward to 2022 and beyond, utilities, investors, and regulators have an opportunity to take the lessons of the past several years to heart and reconsider the impacts of a fundamentally changed economic and policy landscape on gas project viability.

Download Headwinds for US Gas Power: 2021 Update on the Growing Market for Clean Energy Portfolios