Growing Markets for Grid-Connected Battery Storage in India

Power sector regulators hold the keys to unlock the trillions of rupees of battery storage investment necessary to ensure the growth of a flexible, affordable, and reliable grid.

Although the summer of 2024 is now behind us, it stands as the hottest summer on record. During the last week of May, temperatures in parts of northwest India exceeded 50 degrees Celsius (120 degrees Fahrenheit). Rising temperatures led to record power demand. On May 30th, nationwide demand hit a record high of 250 GW.

India’s electricity infrastructure strained to meet soaring demand and experienced its greatest peak power shortfall since 2010. Meanwhile, on the distribution grid, infrastructure also reached a breaking point: nearly 600 transformers failed in Kerala during the summer heatwave. These challenges threaten the affordability and reliability of India’s power system, especially as increasing heatwaves and climate events are expected to persist in the coming years. Fortunately, a solution is emerging: battery energy storage systems (BESS).

BESS Serve Critical Grid Needs

Global examples show BESS can address diverse grid challenges. Countries from China to Australia to the United Kingdom are building large-scale BESS to balance variable renewables generation and maintain resource adequacy. In the United States, BESS are actively used to improve distribution system reliability and resiliency as well as manage grid stability. In Texas, BESS are now the primary provider of frequency regulation, and a substantial provider of other ancillary services. Using BESS to provide these services helped the Texas grid save US$750 million (INR 6,255 crore) over a two-day cold stretch this winter. Across the world, BESS are enabling more efficient, lower-cost power systems.

BESS Are More Affordable than Ever Before

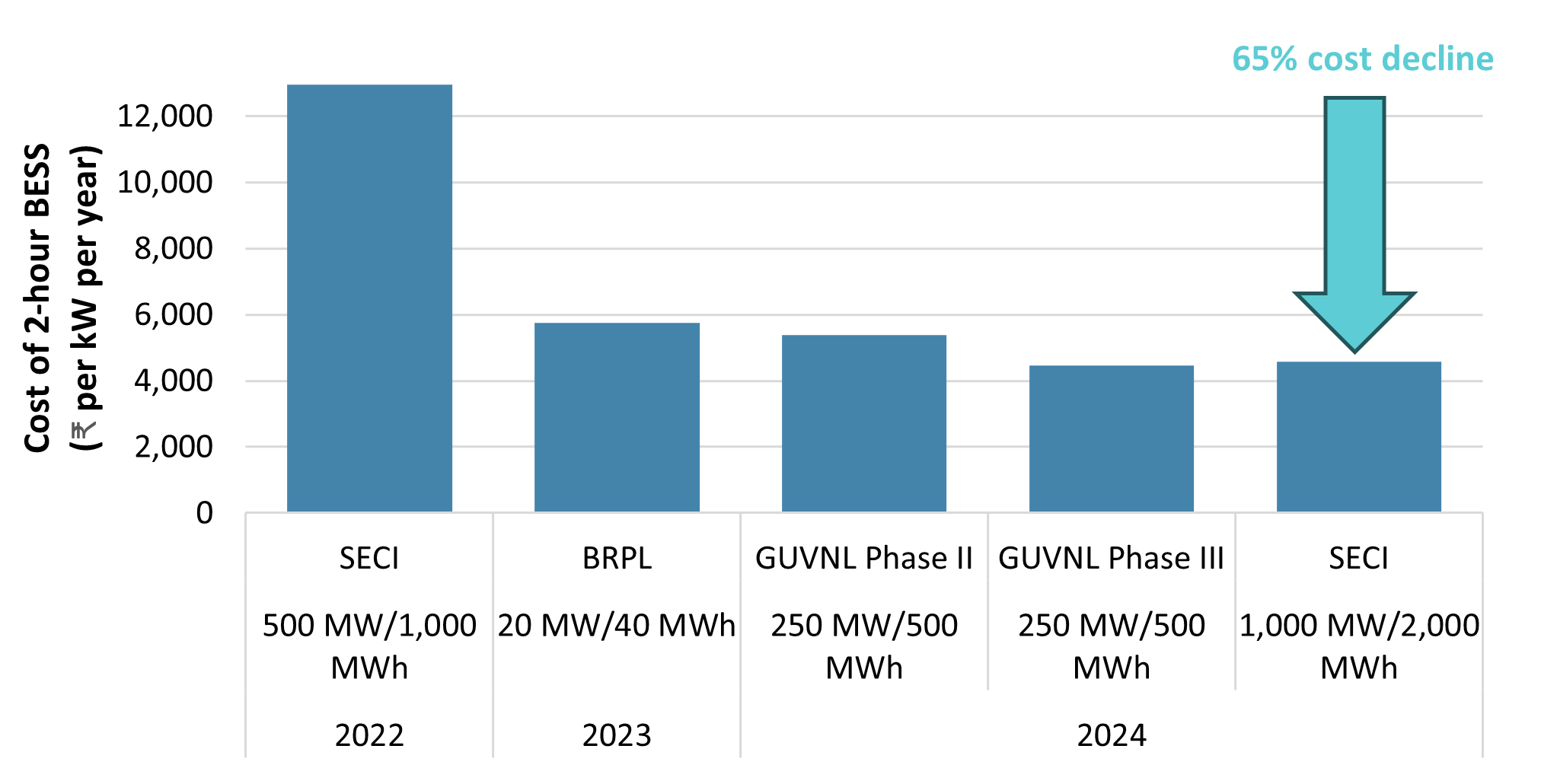

As BESS costs continue to plummet worldwide, they are becoming an increasingly attractive option to meet essential grid needs. India is no exception: in just the past two years, BESS tariffs dropped 65 percent (Exhibit 1). BESS project costs in India will continue to fall due to industry maturation and support from government policies such as the Viability Gap Funding and Production Linked Incentive Schemes.

Exhibit 1: Cost trajectory of 2-hour duration BESS in India

Notes: Source 1: costs for the SECI tender. Source 2: cost for the BSES Radjhani Power Limited (BRPL) tender. Source 3: cost for the GUVNL Phase II and Phase III tenders. All costs are reported in nominal currency and converted to rupees per kW per year. Source 4: costs for the 2024 SECI tender. All costs are reported in nominal currency and converted to rupees per kW per year.

BESS Value Must Be Recognized and Monetizable to Drive Investment

Falling BESS costs will help attract investment, but costs are only half of the equation. For Discoms and independent power producers to invest in BESS, there must be a way to monetize the complete range of BESS services. Today, India’s market rules and regulations only clearly recognize one value stream of BESS: shifting net demand to reduce system energy costs. The result is that BESS are encouraged to operate an “energy only” dispatch strategy. BESS owners receive limited remuneration, and India’s grid receives only one benefit. But global examples show BESS can provide multiple value streams, including deferring investments in energy, generation capacity, and transmission and distribution infrastructure as well as other ancillary services. Through strategic siting and operation, BESS can often provide these values simultaneously, “stacking” the benefits together, and maximizing benefits to the grid.

BESS Could Become Widely Profitable with Valuation Reforms

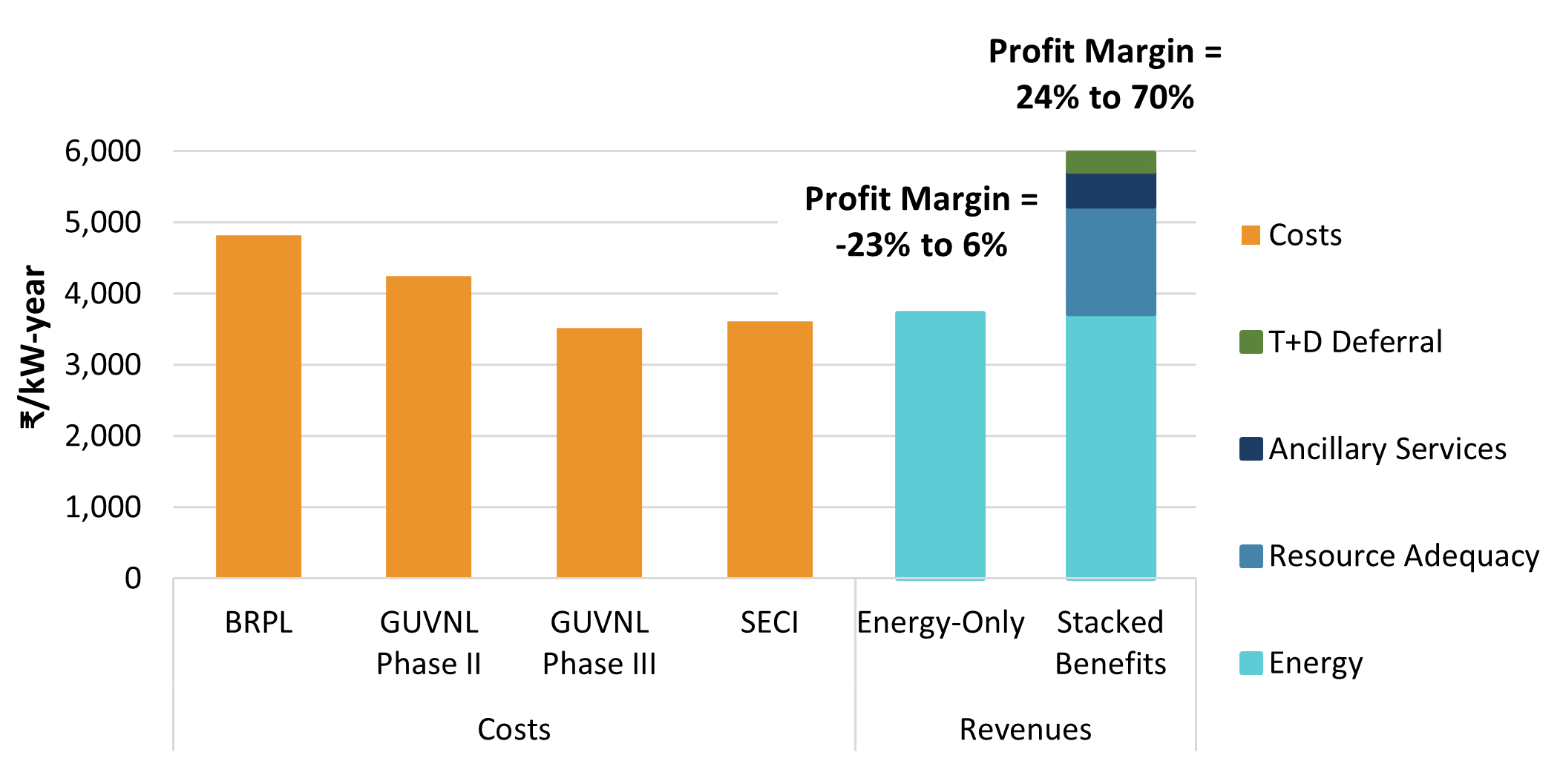

Today, potential BESS investments are teetering on the edge of financial viability. But comprehensively recognizing and valuing all BESS benefits would make them widely profitable overnight. Exhibit 2 shows the project economics for a typical BESS installation in India, comparing costs from the latest four tenders against estimated potential revenues. Under an energy-only dispatch strategy, project revenues exceed only the lowest reported costs (GUVNL Phase III and SECI). But when optimized across the full value stack of energy, resource adequacy, ancillary services, and transmission and distribution (T+D) deferral, the script flips: BESS profit margins are robust against all three reported costs: ranging from 24 to 70 percent.

Exhibit 2: Benefits and costs for 2-hour duration BESS today

Notes: Energy and ancillary service revenue estimates reflect participation in the day-ahead energy market (DAM) and tertiary reserve ancillary services (TRAS), using recent historical data. T+D deferral and resource adequacy revenue estimates reflect long-term (2030) potential. All numbers are standardized to 2020 real currency.

India’s Power Sector Regulators Can Unlock the Market for BESS

India’s power sector regulators hold the keys required to unlock the market for BESS and the substantial systemwide benefits that come from low-cost, reliable grid flexibility. We recommend three actions:

- The Forum of Regulators could issue guidance on BESS valuation for Discoms. Guidance can include clarity around the scope of grid services BESS can provide (including energy, resource adequacy, ancillary services and other balancing services, and transmission and distribution deferral). Guidance could also include a methodology that state regulators and Discoms can use to calculate the value of a project’s combined services.

- State regulators can recognize the resource adequacy value of BESS in long-term planning. States can adopt the Forum of Regulators’ Resource Adequacy Model Regulation. The Central Electricity Authority can give explicit guidance on capacity accreditation of BESS and ensure mechanisms are in place for Discoms to contract BESS capacity in service of meeting integrated resource planning/resource adequacy requirements.

- CERC can update ancillary service regulations to increase transparency and provide BESS greater access. By regulation, BESS can provide both Tertiary (TRAS) and Secondary (SRAS) Reserve Ancillary Service. However, guidance on BESS participation and liquidity in ancillary service markets operations has been limited. Even though market-based procurement for TRAS was initiated in June 2023, the market prices for it are still opaque. SRAS are currently procured out-of-market. Increasing accessibility and transparency to markets for these services is necessary to incentivize BESS investments and unlock the substantial savings made possible by utilizing BESS for ancillary services.

To maintain reliability over the coming decades, India’s grid requires substantial new capabilities. Planners already recognize the important role that BESS can play in cost-effectively meeting grid needs: the Central Electricity Authority’s cost-optimized model of the 2030 grid includes over 40,000 MW (200,000 MWh) of new BESS. To achieve necessary BESS deployments, India’s power system regulators and Discoms can recognize and provide mechanisms to monetize the full value of BESS. This will incentivize large-scale investment, unlocking the full potential of BESS to contribute to an affordable, reliable future.