Learn how we are working to transform how we use and produce energy.

Green Hydrogen on an S-curve: Fast, Beneficial, and Inevitable

We are reaching a series of tipping points in green hydrogen production and demand, and all actors should be prepared to capture these new opportunities.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Most predictions and models assume the energy transition will unfold gradually and that transitions from one innovation to the next are costly and hard. But past transitions, such as horses to cars for transport, gas lighting to electric lighting, and many more, show that rapid changes are more likely than not.

Green hydrogen — a powerful, low-carbon energy source made by splitting water with clean electricity — is one example of a technology that is on track to go through rapid, “S-curve” cost reduction and scale. Countries and companies are announcing new roadmaps and projects in a race to become leaders in a market that will be essential for a 1.5°C future.

Understanding the S-Curve

The S-curve is a commonly observed trajectory of growth for new innovations: slow at first, then rapidly rising, before flattening out again as it reaches market saturation. S-curves mean innovations can scale fast after reaching specific “tipping points,” creating losses for slow movers and large opportunities for those who lead.

These innovation S-curves follow the same phases, each signaling changing market dynamics and winners and losers.

- Phase 1: Visionaries recognize a problem or opportunity and conceptualize a better way to do things.

- Phase 2: Innovators move the concept from the laboratory, models, and sketches to working prototypes or pilots.

- Phase 3: Early adopters form niche markets that link supply and demand. Performance increases and costs decline but the innovation remains at a premium and not widely available.

- Phase 4: The innovation reaches mass market as it outperforms incumbents in costs and performance. This is the steepest part of growth on the S-curve.

- Phase 5: Growth slows as the innovation reaches market saturation. The innovation may be transferred to new markets or serve as the basis for further innovations.

In recent years, we have observed S-curve growth in renewable energy and batteries. The growth of these technologies often far outpaces predictions, unlocking large economic benefits for first mover companies and countries that drive innovation and scale.

The Decade of the S-Curve for Green Hydrogen

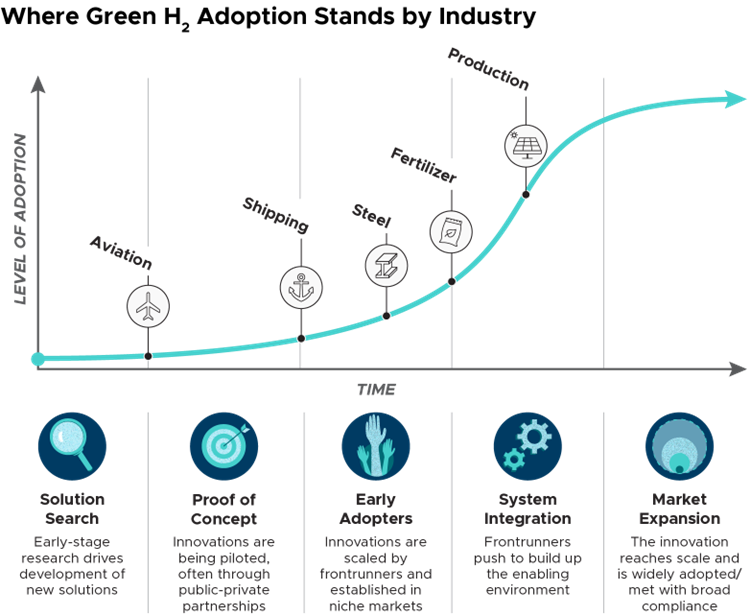

We are now observing increased policy action, corporate commitments, and investments on both supply and demand sides in green hydrogen markets. The decreasing costs of renewables are rapidly reducing the cost of green hydrogen. These are all signals of the third phase, when an innovation advances from pilot projects to the creation of new markets by linking early supply and demand.

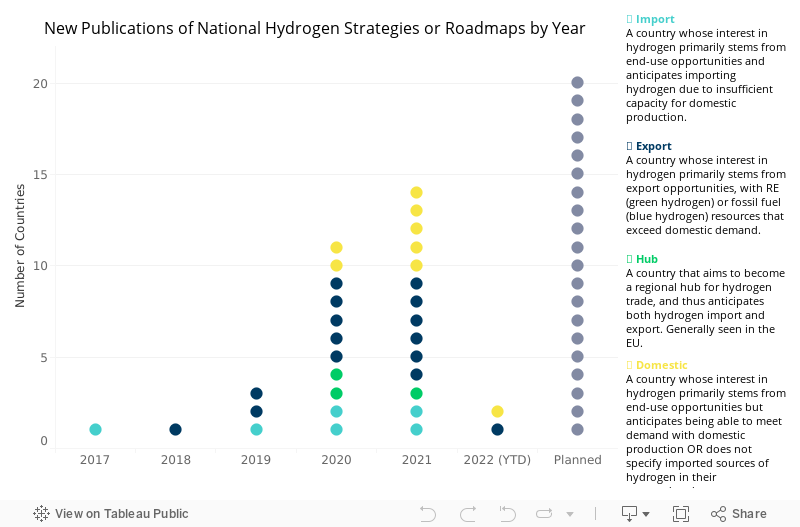

- Policy action will increase: Several countries are preparing to spend hundreds of billions of dollars to rapidly build up their hydrogen economies. Advancing the energiewende that drove down global costs for renewable energy, Germany is forging strategic partnerships to establish a robust green hydrogen supply chain and is working with the EU to develop subsidy schemes supporting first movers. The US Inflation Reduction Act will accelerate innovation. The United Kingdom has opened applications for a national clean hydrogen subsidy scheme. The number of countries with a national hydrogen roadmap has more than doubled every year since 2018.

- Demand will expand: Major demand sectors are rapidly prototyping and piloting technologies that will use green hydrogen in new industrial applications, expanding the total addressable market for green hydrogen across industries:

- Fertilizer: Major fertilizer producers such as Yara and Unigel have begun construction on green ammonia plants, with commercial launch scheduled for 2023.

- Steel: Industry consortiums such as HYBRIT, H2 Green Steel, and COURSE50 are piloting hydrogen-based steelmaking methods with commercial production to begin as early as 2024.

- Shipping: Maersk aims to put 12 green methanol-powered ships into service by 2025. The NoGAPs project is developing green ammonia-powered ships also targeted for operation by 2025.

- Aviation: The Airbus ZEROe program expects to achieve a mature technological readiness level for a hydrogen-combustion propulsion system by 2025, and is targeting commercial launch by 2035.

- Grey hydrogen: Currently, ~90 million tons (Mt) of grey hydrogen per year is used in refining and industry, most of which can be replaced with green hydrogen immediately (without upgrading technologies or industrial processes) once sufficient capacity comes on line. Chemicals manufacturing alone consumed 46 Mt of hydrogen in 2020, and total demand in the sector is projected to reach 54 Mt in 2030.

- Production will scale: New MW-scale green hydrogen production plants, such as the Air Liquide Bécancour site, the Shell China Zhangjiakou site, and the Iberdrola Puertollano site are now competing for the title of largest operational production facility. Gigawatt-scale projects are in the pipeline, with the largest plants expected to have capacities up to 10–30 GW by 2030. These pipeline projects already outpace policy commitments through 2025. Historical patterns suggest that this trend will continue to accelerate past that time frame, potentially reaching as much as 1,000 GW deployed by 2030.

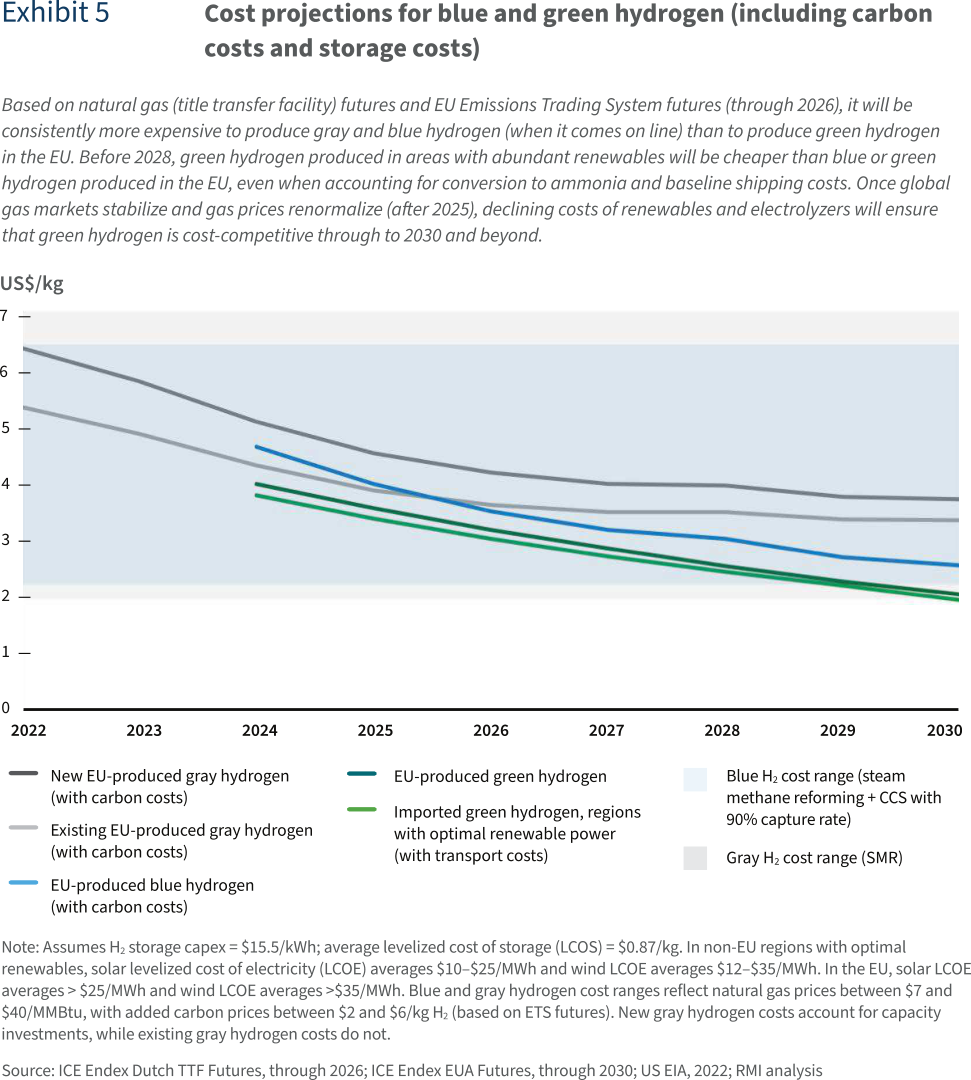

- Prices will drop. Green hydrogen is already cost competitive with blue and grey alternatives in Europe and other key regions. As markets grow, the cost of green hydrogen will also decline rapidly. Renewable energy sources, necessary for green hydrogen production, have entered the “terawatt age” and renewable capacity continues to double every 2-4 years. The cost to produce green hydrogen is expected to fall 50–60 percent by 2030, meaning that achieving US$2/kg without subsidy is feasible within the next five years (all further costs are in US dollars).

Coordinated policy, corporate, and civil society efforts further help the green hydrogen market jump-start and rapidly scale in critical markets. The Green Hydrogen Catapult is driving the scale-up of green hydrogen production through member commitments. The First Movers Coalition brings together potential hydrogen users across key industries to make purchasing commitments, while the Getting to Zero Coalition is setting the stage for niches such as green corridors to take hold. There are many other active coalitions on regional and national scales facilitating the scale-up of the green hydrogen market.

The combined dynamics of supply and demand-side investments, increasing market confidence through roadmaps and commitments, and the establishment of first-mover markets are all signals that green hydrogen is moving firmly into phase 3. The establishment of these markets will enable gigawatt-scale green hydrogen production in the next five years and increase confidence in future market growth. Initial infrastructure build-out will further increase confidence. Fast learning and cost reduction will pave the way for mass market adoption into phase 4.

What Frontrunners Stand to Gain

In relatively stable times, companies succeed by outperforming their competitors through operational excellence. Efficiency, cost-reduction, supply chain integration, and market position are the order of the day. But in times of disruption, when fundamental changes in technology are emerging and S-curves describe rapid adoption paths for new products and services, successful corporate strategies must focus on recognizing and advancing the emergence of new solutions.

Industry players along the green hydrogen value chain can capitalize on huge growth opportunities

Electrolyzer manufacturers globally could see $300–$400 billion in spending by 2030, the investment level required to bring 1,000 GW of electrolysis capacity on line (this assumes an electrolyzer cost between between $300/kW and 400/kW; total spending will in part depend on how quickly electrolyzer costs decline). Up to $1.2 trillion could be directed toward renewables manufacturers to build up the volume of solar panels and wind turbines required to power 1,000 GW of electrolyzers by 2030 (assuming cost for new solar panels averages $700/kW between 2025 and 2030, cost for new onshore wind averages $1,300/kW, and cost for new offshore wind averages $1,500/kW). And an additional $160–$260 billion could reach engineering and construction companies working to build up enabling infrastructure like hydrogen storage and distribution facilities.

At the same time, early movers in demand sectors can benefit from short-term public support mechanisms to accelerate decarbonization, future-proof their operations, and save on long-term carbon costs.

But to fully realize growth and exploit investment opportunities, stakeholders across the value chain should draft and agree on procurement contracts to ensure that production, transport, storage, and conversion facilities can be ramped up at the scale required to meet deployment targets.

Policymakers can accelerate deployment and ensure their economy is ahead of the curve

Policymakers can accelerate green hydrogen’s deployment in key demand sectors by setting precise standards for “green hydrogen” and adopting clear certification schemes as quickly as possible. Coordinating standards across geographies will provide prospective suppliers and consumers enough guidance to draft long-term procurement contracts.

Policymakers can also design effective support mechanisms (e.g., public procurement, targeted subsidies) to signal confidence in the green hydrogen market and remove barriers to investment by offsetting cost differentials between standard fuels and green hydrogen. Directed public funding can incentivize first movers to invest even while technology costs are still high, pushing the market forward along the S-curve.

Countries that move quickly stand to gain industries that are ahead of the curve, with large benefits for their industry and economy in the long run.

Financial institutions can adapt their investment strategies to create and capture new market value

As green hydrogen deployment scales up, demand for incumbent technologies and energy sources will stop growing and reach peak demand. Firms that continue to invest in older technology will face significant business risks as the market leaves them behind.

Climate and transition risks are already building across investment portfolios. As risks for incumbent technologies become increasingly acute, the financial sector will need to re-evaluate their investments and find ways to price in threats associated with climate change and technological disruption.

Financial institutions that move quickly will be rewarded with a chance to create and capture value from investment opportunities in a green hydrogen market that will grow to hundreds of billions of dollars. Investors that get in on the ground floor of green hydrogen can work alongside a vested public sector to mitigate risks and stake their ground in a market poised for rapid growth.

Green hydrogen is on an S-curve. We are close to reaching a series of key tipping points in renewable and hydrogen production deployment, and all actors should prepare for a potentially disruptive market shift and race ahead to capture these new opportunities.

Authors

Yuki Numata

Senior Associate

Laurens Speelman

Principal

Nick Pesta

Senior Associate

Oleksiy Tatarenko

Senior Principal

Natalie Janzow

Related Insights

Harnessing Green Demand to Drive Sustainable Chemicals Production

What Michigan’s Clean Community Financing Ecosystem Can Teach Other US Regions

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.