Learn how we are working to transform how we use and produce energy.

Unpacking Five Key Barriers to Transition Finance

The world needs transition finance to speed the decarbonization of heavy industry. Here’s what’s stopping it.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

The transition to net zero will not happen without emissions reductions in high-emitting and hard-to-abate sectors. Yet credible transition finance that can both meet stakeholder expectations of real economy emissions reductions and satisfy banks’ internal governance and financial requirements is proving elusive. In this article, we explore five barriers to the deployment of transition finance at the scale and speed required.

The barriers to transition finance are often connected and mutually reinforcing. This has arguably hindered progress — but the good news is that potential solutions are equally interrelated. If financial institutions and other stakeholders can make strides in overcoming one barrier, others are likely to fall too. For example, clearer policy-led incentives could help unlock additional bankable projects. Searching for force multipliers that reduce these barriers across the financial system could help rapidly scale the market for and allocation of transition finance.

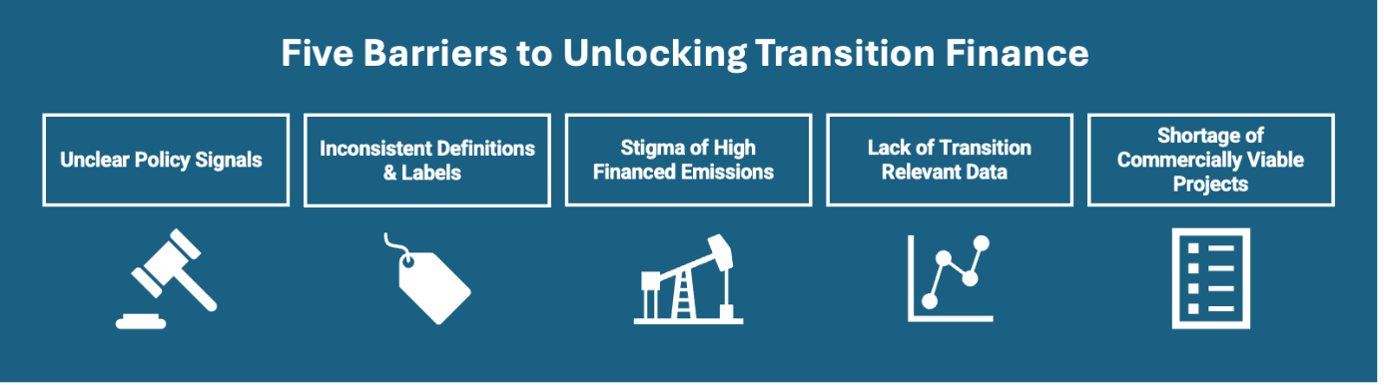

Unclear Policy Signals

Financial institutions indicate that stronger, clearer signals from policymakers are needed to accelerate and de-risk the energy transition. Policy and regulatory initiatives could bolster incentives for decarbonization in key sectors and geographies. For example, the Inflation Reduction Act (IRA) has been praised for unlocking transition-enabling finance in the utilities and hydrogen sectors. Complex and ever-changing reporting and disclosure regimes are also seen as hindering transparency and accountability in the market and financial institutions face multiple related challenges in assessing transition progress, risks, and opportunities. Financial institutions engaging with policy makers, in addition to engagement with clients and sectoral initiatives, could help foster better understanding of actions each can take to support the mobilization of transition finance.

Inconsistent Definitions and Labels

Perhaps one of the biggest challenges to transition finance is defining exactly what it is and what activities should or should not be considered eligible. In a previous article, we identified the critical importance of transition finance and highlighted the ongoing debates around its scope, purpose, and credibility. Yet, the lack of a common definition makes it hard to track and quantify the scale of the market. The burden of proof against potential greenwashing accusations, without clear guardrails of what is credible, is often a barrier to entry when assessed against the perceived limited benefit of a transition finance label.

While some attempts at labels exist, such as the recent Japanese sovereign climate transition bond certified by Climate Bonds Initiative, anecdotally we have heard skepticism about the potential for a premium or prudential benefit required of an effective, incentivizing label.

In the face of moving goalposts, financial institutions and counterparties are reticent to act publicly or at scale. Instead, to date, firms have developed their own definitions and frameworks (such as by Standard Chartered, SMBC, and Barclays) to ensure that at least internal approaches and education on the topic are consistent and any external communication is transparent. Yet this approach risks a first mover disadvantage by exposing firms to enhanced scrutiny and potential misalignment with future market standards. This is another opportunity for further collaboration and clarification between financial institutions and policy and standard setters.

Stigma of High Financed Emissions

Concerns about greenwashing and risks associated with carbon lock-in contribute to stigma associated with transition finance. Related market pressures are reportedly stifling potential transition finance transactions as financial institutions struggle to articulate the business case and demonstrate environmental outcomes to counter this stigma. This is particularly acute now that financed emissions and fossil fuel-to-renewable financing ratios are core metrics against which financial institutions are assessed by stakeholders (including asset owners, regulators, and civil society).

Focus on financed emissions accounting could lead to firms prioritizing portfolio climate alignment through divestment strategies. This may reduce paper emissions but does not necessarily reduce real economy emissions. Providing transition finance to companies that currently have high emissions, on the other hand, could raise banks’ financed emissions in the short term. However, the stigma related to this can fail to fully capture the nuance of both the need for this capital to enable decarbonization and the potential for long-term reduced and/or avoided real economy emissions.

Lack of Transition-Relevant Data

While there is growing awareness of the limitations to financed emissions metrics noted above, a remaining challenge is the lack of alternative metrics to measure, report, and incentivize transition finance across the market. The NZBA and GFANZ both published discussion papers on the subject at the end of 2023, but no approach has been widely adopted in the market.

Furthermore, financial institutions seeking to deploy transition finance face significant data gaps in terms of comparable, forward-looking, transition-relevant data. This is particularly significant in certain segments of the market, such as private markets and emerging and developing markets. Where data exists, financial institutions must often compare apples to oranges and make judgment calls on what is credible. This is complicated further by the array of sectoral, regional, and global scenarios, pathways, and benchmarks against which companies and projects are assessed.

Transition plans are increasingly seen as a key input, and even criteria, for transition finance transactions. It is hoped that client transition plans will offer investors and bankers an indication of credible pathways to 1.5°C alignment and a business strategy to achieve them. Efforts to standardize, define credibility of, and even mandate transition plans are underway through groups including GFANZ, the UK Transition Plan Taskforce (TPT), and the Assessing Company Transition Plan Collective (ATPCol). However, few companies have published transition plans to date and more work is needed to understand how they can and should be used for transition finance decisions. Issuing a plan is not the same as achieving it, and the presence of a transition plan does not necessarily indicate that a company is the best financing opportunity for supporting the transition.

Financial institutions’ ability to assess the contents of transition plans against the needs of different sectoral and regional pathways will also need to improve over time. While transition plans could be a useful data input, they are unlikely to be a silver bullet that unlocks credible, comparable transition finance, and overreliance on them as a criterion for transition finance risks delaying deployment of capital at the scale and speed needed to reach 2030 climate goals.

Shortage of Commercially Viable Projects and Companies

Credible, commercial opportunities for certain transition technologies — such as hydrogen — are still the exception rather than the rule. A lack of proof points and bankable or financeable transactions has slowed deal flow, with many financial institutions noting that liquidity and desire for transition-related deals are not the problem. When transition opportunities have come to market, they tend to be oversubscribed — with the Japanese climate transition bond almost three times oversubscribed upon launch.

Many transition projects do not meet required risk-return profiles or sufficient safeguards, such as guaranteed offtake contracts or reliable governance structures, to be deemed bankable. Public finance could be a potential catalyst to unlock new project pipelines by offering blended finance for strategic opportunities necessary to support the transition, but the mechanisms for this to accelerate transactions in key sectors and regions remain under-developed and can be seen as an additional, interrelated barrier to scaling transition finance. Some commentators are also calling for private financial institutions to overcome this barrier through innovation of new, and adaptation of existing, financial instruments.

Overcoming These Barriers

Supporting new and existing clients by issuing robust transition finance is an area that could be a potential avenue for competitive advantage and pathway to achieving financial institutions’ own net zero commitments. However, persistent barriers exist to scaling transition finance and the labeled market remains small, with a recent ICMA report finding that only 0.4 percent of the sustainability-linked bond market is transition-labeled.

Overcoming the above barriers to mobilizing transition finance requires a holistic approach across various stakeholders, including governments, policymakers, corporates, and NGOs, in addition to financial institutions. At COP28, RMI was joined by ten other NGOs in publishing a Global Call to Action which outlined some recommended next steps for each of these stakeholders to support the scaling of transition finance. With a better understanding of barriers and enablers through collaboration, thought leadership, and case studies, we hope to see solutions emerge that help the transition finance market scale to meet the needs of a 1.5°C-aligned future.

Authors

Elizabeth Harnett

Research and Impact Expert

Tricia Holland

Senior Associate

Kaitlin Crouch-Hess

Senior PrincipalRelated Insights

Improving Energy Transition Assessments with Regional Pathways

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.