Man installing alternative energy photovoltaic solar panels on roof

Congress Cannot Ignore Residential Solar Tax Credit Inequities

Through the Justice40 Initiative, President Biden has made clear that bringing clean energy benefits to marginalized and low-income communities is a priority. Right now, low-income households experience up to three times higher energy burden (the percent of household income spent on energy costs) than high-income households. Rooftop solar is one of many important solutions available to help alleviate this burden. When financed, it can immediately lower household energy bills with no money down in many parts of the country.

Unfortunately, rooftop solar has disproportionately benefited high-income and White residents. While low-and moderate-income (LMI) residents make up 43 percent of the US population, only 21 percent of residential solar installations benefited these communities in 2019. On top of that, nearly half of communities with a majority of Black residents did not have a single solar system installed.

This disparity is exacerbated by the inequitable design of existing tax credits that incentivize residential solar. The solar investment tax credit (ITC) provides minimal advantage for those with little to no federal income tax—and thus have little use for a tax break.

In its version of the reconciliation bill, the US House of Representatives has included a direct pay option under section 48 (ITC 48) for business- and utility-scale renewables. This would allow entities without sufficient tax liabilities to take full, direct advantage of the ITC and accelerate renewable deployment. But, importantly, the current bill language does not extend the same direct pay provisions under section 25 (ITC 25D) for residential solar.

It is essential for Congress to change ITC 25D from a tax break to direct pay to help bring clean energy to more Americans, particularly LMI Americans. Specifically, the change would:

- allow substantially more homeowners to use the tax credit,

- further enable clean energy sources to help alleviate LMI energy burden, and

- bring solar jobs to LMI communities.

Residential Direct Pay Makes the Tax Credit Available to Substantially More Households

The House’s currently proposed version of the residential tax credit under section 25D can offset the upfront cost of a typical solar photovoltaic system by around $5,000 (assuming $3.30 per watt installed and a 5 kW system). That discount would be far out of reach for almost all LMI households, and even many middle-income households, given that their tax burdens often fall below that threshold.

Around 7 in 10 American tax filers would not have enough annual tax liability to receive the full ITC 25D benefit, according to 2018 data from the IRS. And the more than 4 in 10 Americans that do not have any federal income tax liability at all would see zero benefit.

Consider a married couple with one child making a combined income of $60,000 per year (around 70 percent of the median family household income). Given their annual federal tax liability of around $1,500, they would see only 30 percent of the House’s currently proposed residential solar tax credit in the year that they purchased the system. The inequities are even starker for low-income households. If that same household made $45,000, they would likely not receive any benefit.

While the current ITC 25D does have a carryforward provision that allows taxpayers to apply the rest of the credit in future years, most homeowners do not realize this complicated provision. Even with this policy in place, LMI households likely cannot wait years to receive the full amount, and the bottom half of earners still receive little to no benefit from the incentive.

Residential Direct Pay Can Help LMI Residents Reduce Their Energy Burden

Changing the ITC 25D from a tax break to direct pay would not only lower the upfront cost of solar for residents, but it could also be the catalyst for LMI homeowners in many states to lower their energy costs. For the more than 100 million American households without the tax liability to utilize the full ITC 25D, changing this benefit to direct pay could be the difference between rooftop solar lowering or increasing their bill.

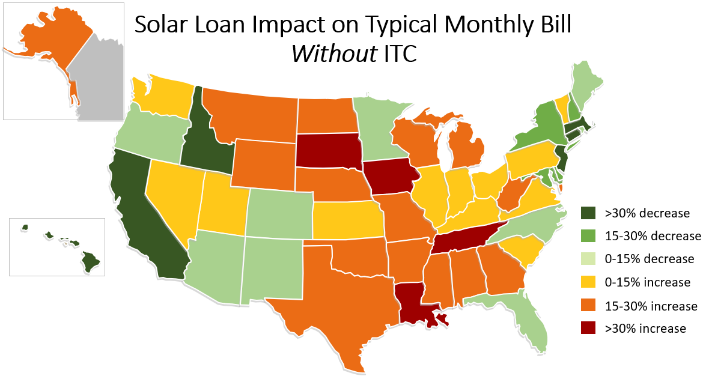

For LMI households without any federal tax liability, an average 20-year rooftop solar loan would reduce their energy burden in just 19 states under the current policy, according to an analysis using RMI’s forthcoming Residential Solar Calculator. Direct pay for ITC 25D would bring this number to 38, doubling the number of states where families below the federal income tax threshold would be able to use a solar loan to save money with no money down.

This change would also decrease utility bills by around 20 percent. This could significantly accelerate the solar market in these 19 additional states and bring the co-benefits to more LMI communities.

Residential Direct Pay Is Essential to Bring Solar Jobs to LMI Communities

By modifying the ITC 25D to direct pay and opening up the solar market to a previously untapped portion of the country, the solar industry can also bring economic development and workforce benefits to LMI communities.

If LMI communities could match the levels of annual rooftop solar installations that are currently seen in high-income neighborhoods, an additional 1.2 GW of residential solar economic activity could take place in LMI communities each year. This would generate nearly $4 billion more in economic activity (assuming $3.30 per watt installed) and over 26,400 more jobs each year (assuming 22 residential solar jobs per MW). To realize this full impact, solar job training will also be essential to ensure a smoother, more equitable transition to cleaner energy sources, while maximizing economic benefits.

It’s Time for Congress to Take Action

Right now, Congress has a once-in-a-decade opportunity to design equitable climate policy that will ensure all communities can access the benefits of renewable energy.

Fortunately, momentum is building. The Residential Renewables for All coalition recently formed to advocate for this change to the residential solar tax credit, which 25 US Senators have urged leadership to include in reconciliation. The coalition includes more than 350 environmental justice advocates, environmental justice organizations, and renewable energy businesses.

For too long, the ITC 25D has made solar deployment more inequitable. To level the playing field and reduce the energy burden for lower-income Americans, all households should have the same opportunity to access residential solar incentives. This simple change can lead to more equitable solar deployment and bring the economic, workforce, health, and emissions benefits to the communities that need them most.