Learn how we are working to transform how we use and produce energy.

US Can’t Meet Climate Goals While Spending Billions on Gas Infrastructure

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

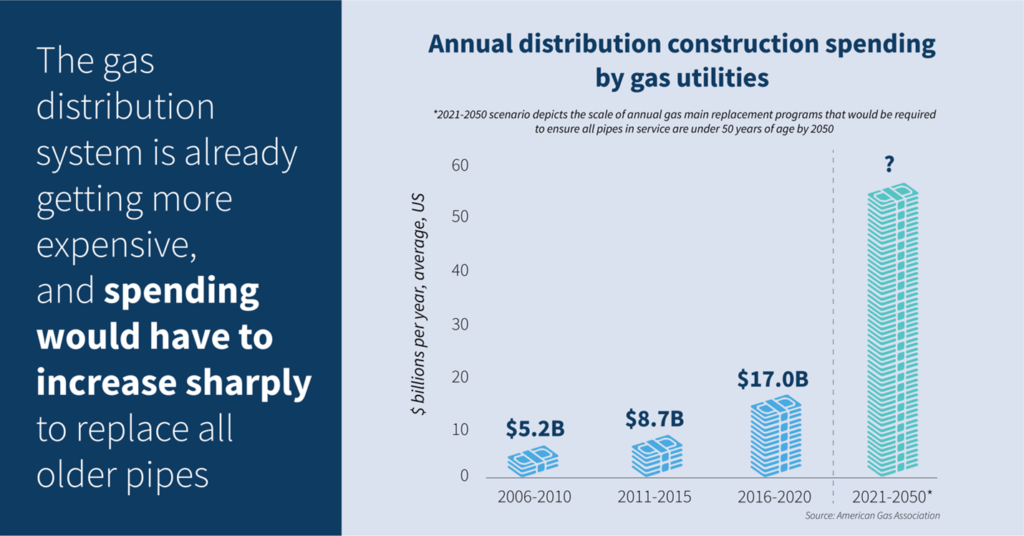

America’s gas utilities spent $21 billion on gas distribution infrastructure in 2019, more than four times what they spent just a decade prior. This dramatic increase deepens the country’s reliance on a system that delivers fossil gas to millions of homes and businesses and compounds the challenge of transitioning to a cleaner, healthier alternative.

Continued growth in gas infrastructure spending—especially the local distribution systems that bring gas to homes and businesses—are counterproductive to a safe and sustainable climate future. New spending should support carbon-free alternatives to gas, like heat pumps, weatherization, and other clean energy technologies. Future spending on gas delivery systems should more narrowly focus on targeted safety and leak-reduction needs.

We need to reverse the trend of increased spending on gas distribution infrastructure so we can move our energy systems away from fossil fuels and protect utility customers from bearing the cost of an outdated infrastructure in the future. We expect the country will dramatically cut its use of gas in buildings as states and cities implement climate policies—a shift that will leave this infrastructure underutilized and customers saddled with legacy costs that will only grow with expanded gas spending.

Limited Use Cases for Hydrogen and Biogas

The gas industry and utilities are pushing hydrogen, biomethane, and other lower-carbon gases as a reason to maintain gas distribution infrastructure while reducing emissions, hoping that consumers will be willing to cover the costs.

This line of argument has been gaining traction in research and policy. A study published in April 2021 by the Columbia University Center on Global Energy Policy argues for continued investment in the US gas delivery system and advocates for hydrogen and biogas to be used in these systems. And some state governments, including New York’s, have also been studying the potential for alternative gaseous fuels.

However, broad arguments in favor of hydrogen and other fuels do not fully grapple with important distinctions among their potential uses, and what they mean for spending on gas infrastructure. These fuels are expensive—estimated to remain seven to nine times more costly than fossil gas by 2050. These fuels will be best suited to high-value applications in power generation and hard-to-abate industrial uses, as opposed to residential and commercial buildings. The local gas distribution systems that serve buildings are usually separate from those serving factories and power plants, and distribution system spending should be considered on its own merits.

Given the availability of solutions to electrify homes and businesses, the higher-cost solutions like biomethane and hydrogen will have very limited use for these customers in a carbon-free future. Continuing to spend on expanding and upgrading local, neighborhood-level gas infrastructure risks sinking tremendous investment into systems facing quickly declining usage and poses an opportunity cost when funds could directly support carbon-free solutions like energy efficiency and electrification.

Instead, utilities and regulators can geographically segment gas systems and single out industrial and power system customers that need gaseous power sources. This would be a shift from the large-scale distribution system we have today, where infrastructure running down every street serves individual households and businesses. This compartmentalization is especially important for hydrogen, which will require expensive gas infrastructure retrofits and upgrades best suited for targeted, high-value customers.

Electrification initiatives and targeted gas system retirements can then be pursued for residential and commercial customers, reducing the overall carbon footprint of the gas system and bringing down costs for those who stay on the gas system.

Aging Infrastructure and Methane Leaks

More than 630,000 leaks in US gas distribution lines make up about 7.6 percent of the country’s methane emissions, according to the Columbia University report. Methane is a particularly potent greenhouse gas, with 84 times the global warming potential (GWP) of CO2 over a 20-year timeframe.

While reducing methane leaks is critical and urgent, massive pipeline replacement programs are a costly solution. The cost is especially high for utility customers—particularly when other approaches may be similarly effective at lower cost. In Chicago, for example, Peoples Gas began a customer-funded pipeline replacement program in 2011 with a budget of $2.6 billion over 20 years. A decade later, the project is far behind schedule and is expected to take an additional $7.7 billion and another two decades to complete.

Other solutions include gas demand reduction through electrification and energy efficiency, which helps decrease methane emissions because less gas is produced and transported in the first place. Electrification at scale—especially for residential and commercial customers—can enable retirement of aging gas mains, which serves the same purpose of eliminating methane leaks without perpetuating gas combustion. In tandem, advanced leak detection programs can identify leaks for repair or replacement where they are most needed, producing a more immediate impact.

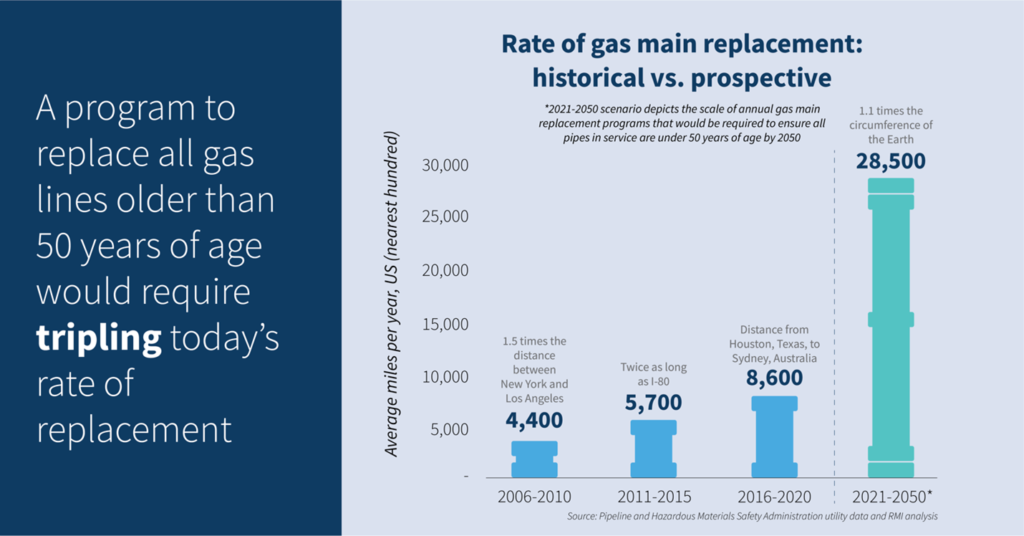

Replacing all the aging gas mains across the United States would be an expensive proposition. The Columbia report recommends replacement of distribution pipes over 50 years old. That age range makes up 26 percent of today’s gas main system, according to RMI analysis of 2020 data from the US Department of Transportation’s Pipeline and Hazardous Materials Safety Administration. The implications of such a proposal are depicted in the charts below. There are 1.3 million miles of gas mains in service across the country, with about 337,000 miles already more than 50 years old. Eliminating all pipes over 50 years old by 2050 would require replacing more than 28,000 miles of gas mains per year, starting immediately. This figure is more than three times higher than the actual replacement rate over the past five years, which has already hit a historic high.

Tripling the rate of gas main replacement would demand immensely higher spending, even beyond the quadrupled spending by gas companies on distribution infrastructure in the past decade. This spending poses a massive opportunity cost, as funds may be better spent on zero-carbon building upgrades. And the new infrastructure would be at risk of becoming stranded assets as gas demand falls in the coming decades.

Reducing Emissions and Stranded Asset Risks

It’s important to distinguish between investments in the existing system and investments in extending distribution lines to new customers. It’s a common practice across the United States for gas companies to socialize the costs of extending gas infrastructure among its customers, allowing developers to avoid the costs of installing gas mains and services.

These new investments exacerbate the risk of stranded assets as climate action and customers’ preferences shift away from gas. This practice also skews incentives for developers, favoring installation of gas in new buildings even if it’s often easier and more cost-effective to build new construction without gas installation.

Policies that discourage or restrict investment in expanded gas infrastructure, including phasing out gas allowances, enacting all-electric building codes, and requiring evaluations of non-pipe alternatives to gas projects, should be considered by policymakers across the country.

Limiting Gas Distribution Investments Is a Crucial Climate Strategy

The International Energy Agency’s Net Zero by 2050 study found that in the next 15 years, the world’s biggest economies will have to significantly reduce emissions from fossil fuels to avoid the worst impacts of climate change. And, the study finds, these countries need to begin switching to electric appliances in residential and commercial buildings in the next five years.

The writing is on the wall: gas use will have to decline steeply in buildings, and investments in local gas distribution infrastructure don’t align with US climate goals. Even replacement gaseous fuels, like hydrogen, are not a silver bullet. Electrification is a viable alternative. Governments have the responsibility of supporting policies that prioritize emissions reductions instead of further gas investments. And they must act quickly—the window to make the right decision is closing.

Related Insights

What Michigan’s Clean Community Financing Ecosystem Can Teach Other US Regions

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.