Learn how we are working to transform how we use and produce energy.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

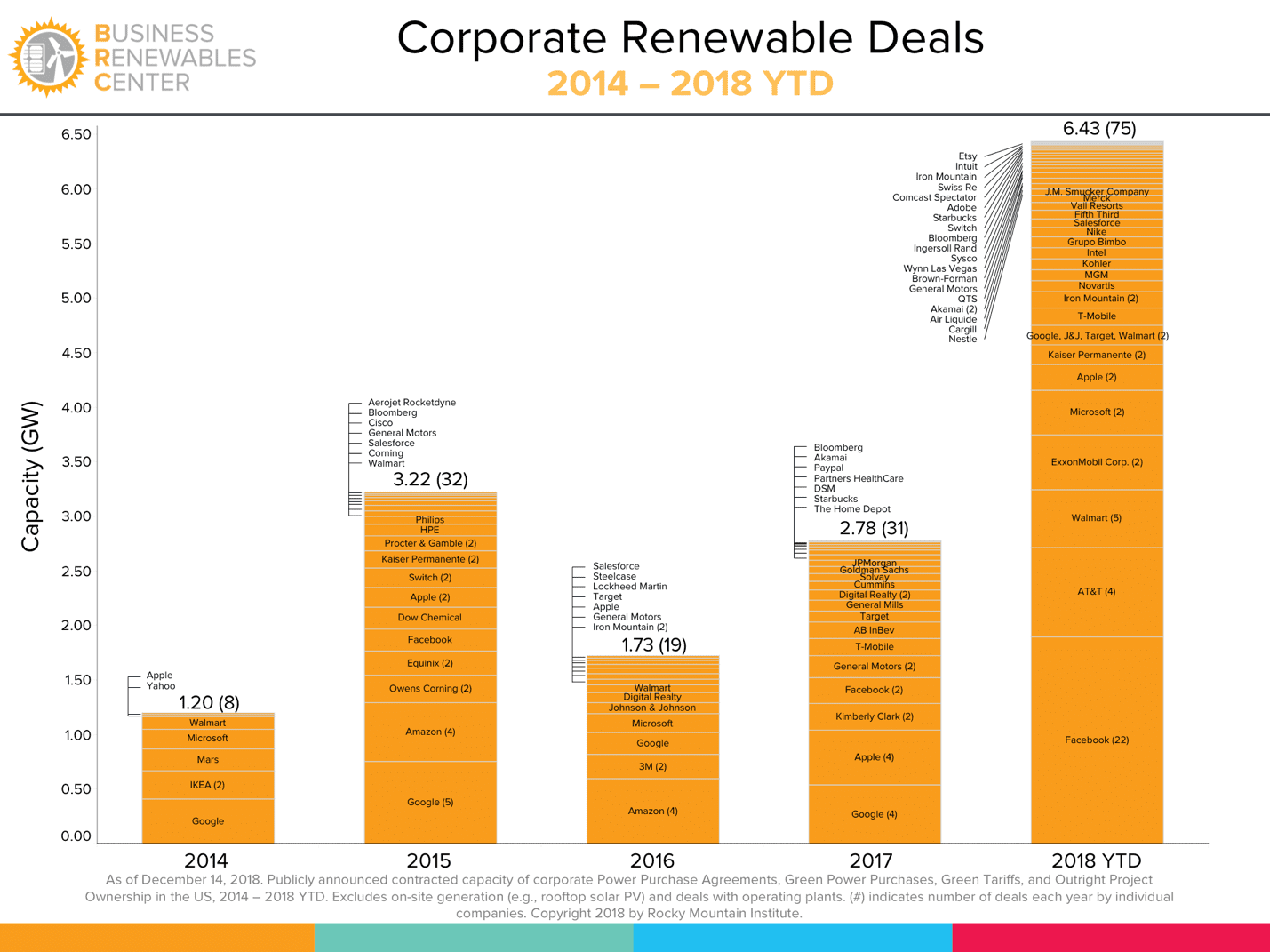

This past year set a new record for total capacity of announced corporate renewable energy (RE) purchases. This unprecedented demand has been met with robust supply from renewable energy project developers as well as from utilities, which have demonstrated their willingness to work with these buyers in finding new solutions in the market. The Business Renewables Center (BRC) State of the Market update is a glimpse into the corporate renewable energy purchasing trends of 2018. We provide some of the highlights below.

Power of partnership

The voice and the role of the commercial and industrial buyer today has become ubiquitous in the renewable energy market, reflected in the commitments from thousands of signatories within the Corporate Renewable Energy Buyers’ Principles, RE-100, and We Are Still In initiatives. Two messages are now clear:

1. Renewables are economic

2. The private sector prefers a clean energy transition

As of December 14, 2018, the corporate renewables market reached 6.43 GW of announced renewable off-site deals in the United States (however, additional buyer transactions have never been made public and therefore remain outside these market updates).

The type of transactions announced and disclosed to the BRC have two things in common:

1. They are utility-scale—from 5 to 315 megawatts (MW).

2. They are all off-site—they are not panels on a factory roof, but rather large wind and solar projects and farms developed to feed the grid.

The various types of corporate renewable transactions include off-site power purchase agreements (PPAs), REC strips, green tariffs, other utility solutions, and outright corporate investment in projects.

Tipping past 6 GW

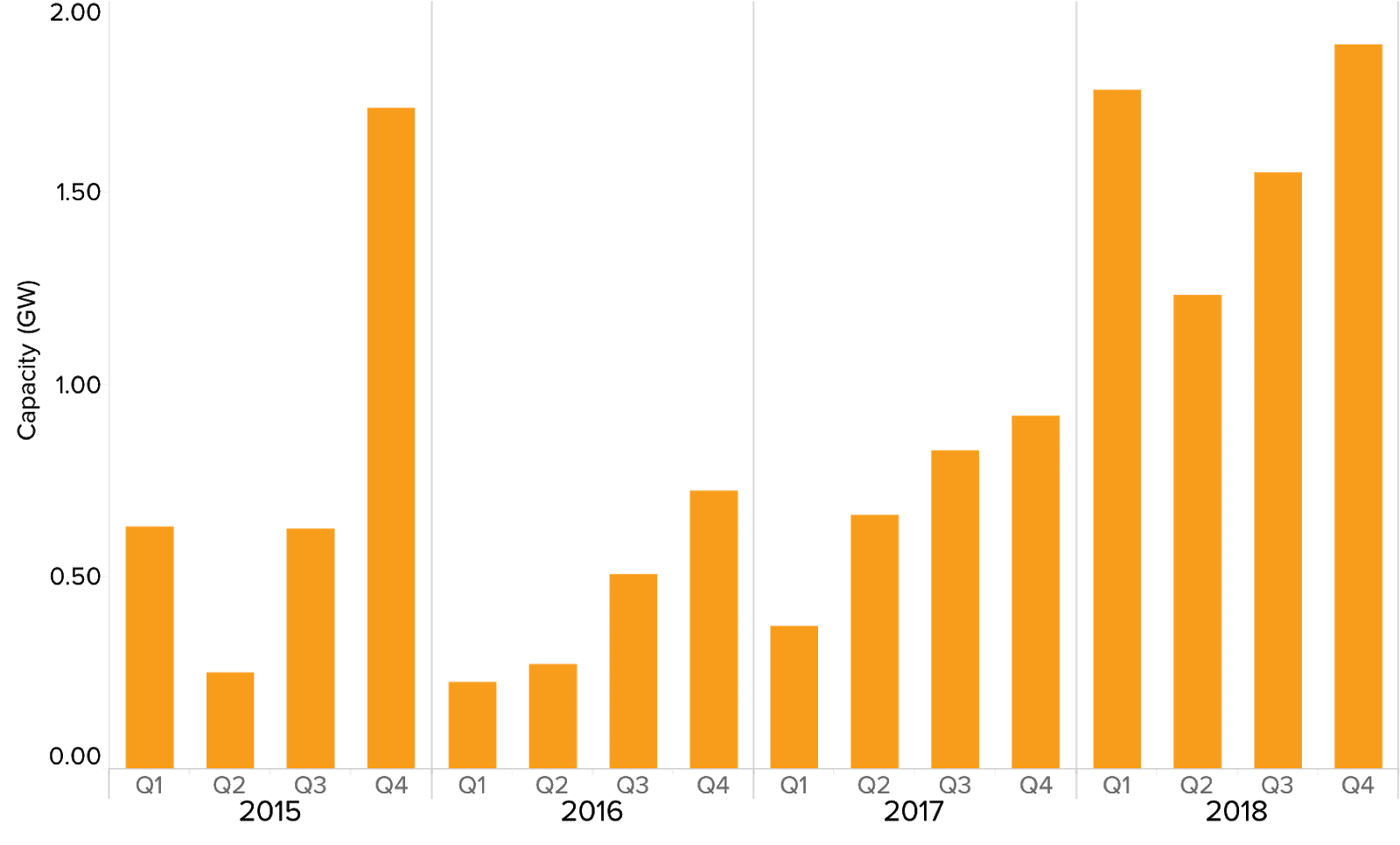

For the past three years, corporates consistently announced the most deals in the fourth quarter. Unsurprisingly, the fourth quarter of 2018 also saw the most volume of RE purchases in the amount of 1.89 GW (as of December 14, 2018).

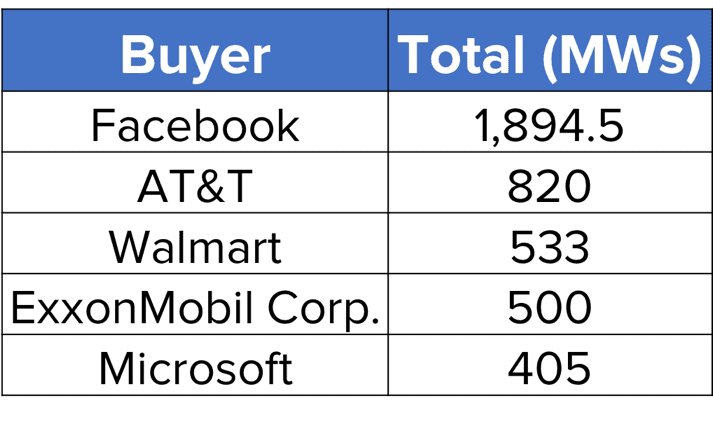

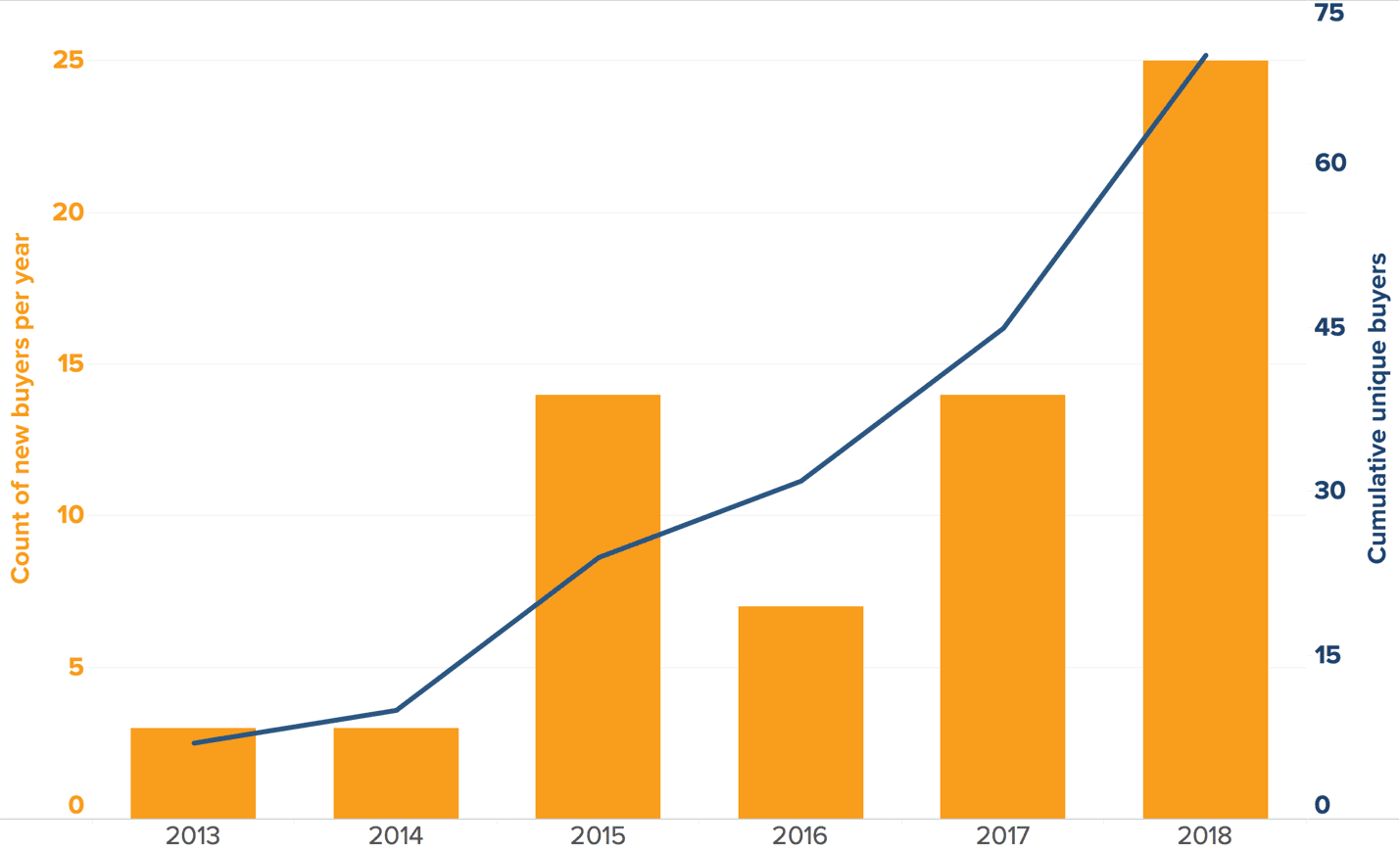

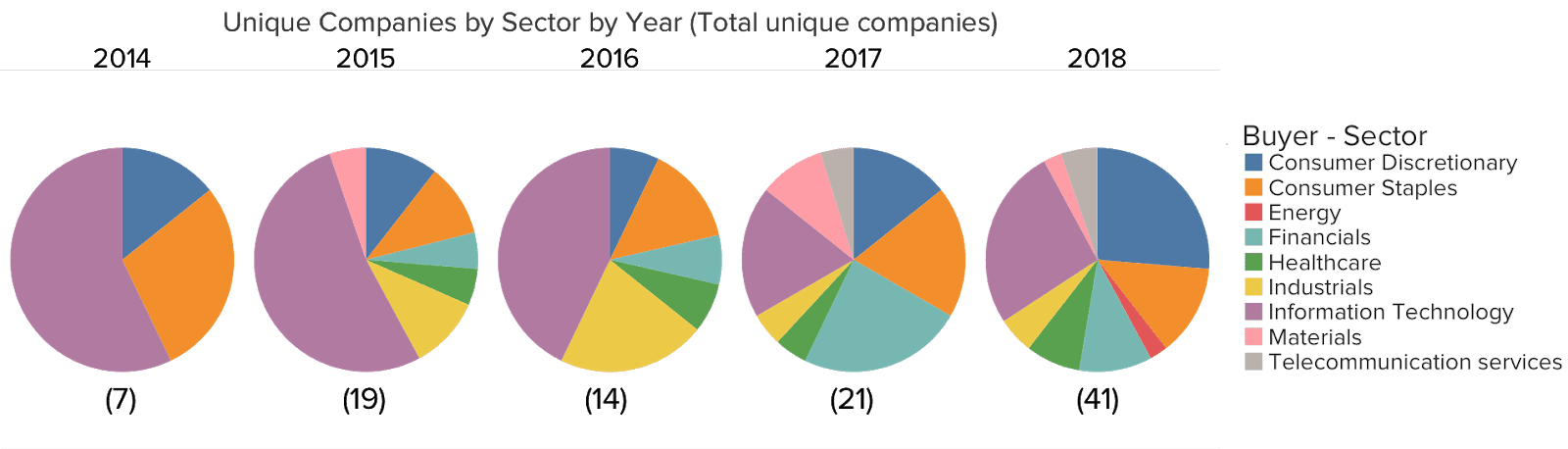

Thus far, 2018 saw 75 unique deals made by 41 individual buyers, 25 of whom were inking first-time renewable energy contracts. Over the years, the marketplace has seen a steady stream of new corporate buyers joining the renewable procurement playing field. The market has reached 70 buyers cumulatively since the first corporate deal in 2008.

First time deal examples included Kohler’s 15 year 100 MW virtual power purchase agreement (VPPA) with Enel Green Power NA and J.M. Smucker’s 60 MW PPA with Lincoln Clean Energy (now Ørsted), with Schneider Electric Energy & Sustainability Services serving as an advisor. Although barriers remain such that each of these deals may take year-long efforts to plan, member buyers have told the BRC they are feeling more comfortable making these kinds of commitments because of the prior year’s track record.

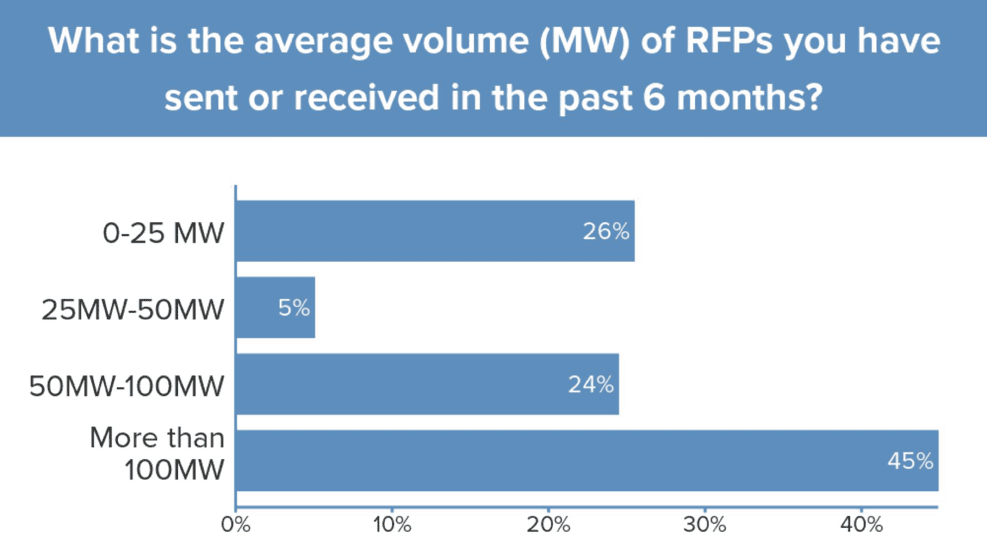

The deals made in 2018 indicate that there is still room to grow substantively in deal size. In fact, the latest poll of 100 Renewable Energy Buyers Alliance (REBA) members showed a surprising number of very large RE procurement deals (i.e., over 100 MW) being requested from buyers in the market. Forty-five percent of respondents were still receiving RFPs or sending out RFPs for more than 100 MW into 2019. Simply 10 members of those polled realizing their RFPs would mean over a gigawatt of demand for renewable power alone. There is much more large-load demand and growth to be realized.

Sector diversification

Every year, the market of buyers is becoming more diverse, not only in the terms of the size of the organizations (smaller market entrants), but also in the demand. The percentage of unique buyers in the space is evenly distributed, with an extra push this year from telecoms. The apparel sector is also ramping up its participation, either by companies announcing their RE goals or by making deals like Nike’s VPPA with Avangrid of 86 megawatts in Texas, covering its entire North American load.

Suppliers change and adapt

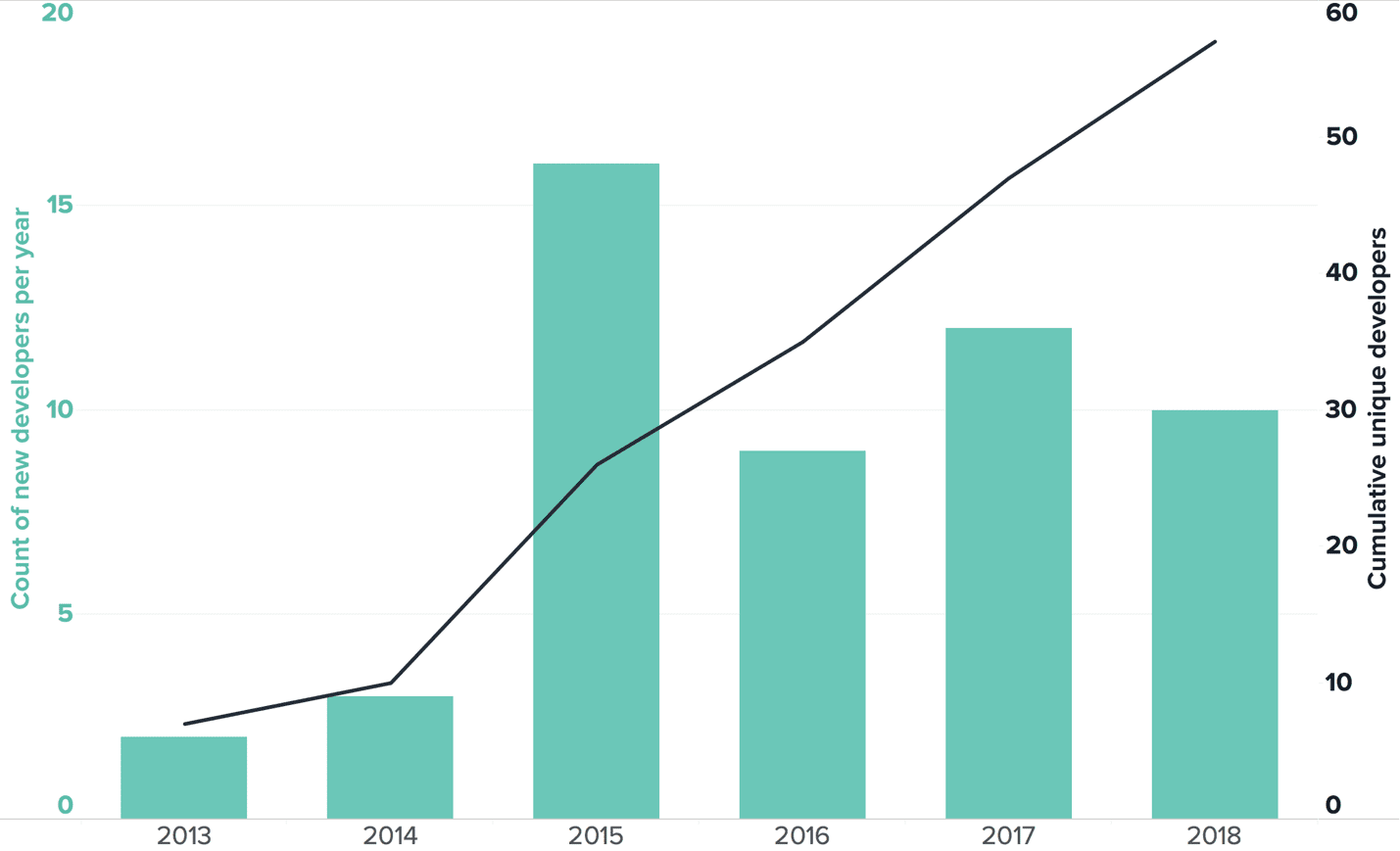

A new market of buyers has also been followed by new supplier entrants. It is clear that our collective mission is to get new buyers to go from renewable commitments to action. However, it is the developers and utilities that keep surprising us year after year, being chosen for their first utility-scale corporate PPA. More importantly, a robust market means new participation from both the buy and sell side, resulting in diversification of products and liquidity. It’s an indicator of the health of the market.

The new additions to the corporate PPA market are not new or unknown developers. They are experienced, sophisticated energy companies that understand the new energy transition and many provide and test new solutions every year. It’s a positive market advancement when a developer makes a deal involving both wind and solar, and also includes battery storage capacity, as was the case for NextEra Energy Resources’ deal to help healthcare’s Kaiser Permanente reach its carbon neutrality goal.

Utilities rising to meet customer demand

In 2018, the real change in the corporate renewables market has been the green tariff transactions with utilities creating new solutions for their commercial and industrial customers. The animated map below illustrates over time, every year, where green tariffs have been introduced in different states. World Resources Institute (WRI) and World Wildlife Fund (WWF) have monitored the regulated market and are core to the engagement with regulators such that every green tariff or every utility solution is a contributing factor to the way the market is supplying renewables to major corporations.

As of December 2018, 23 green tariffs have been approved or proposed, with 2 denied by the Commission, in 17 states by 16 different utility. More utilities are working with their customers to provide them with options, and it is a breakthrough negotiation. WRI’s data on green tariffs shows deals starting in 2013. We are starting to see more utilities incorporating renewables into long-term planning and thinking about solutions beyond green tariffs to better meet the loads and needs of existing customers, including tackling smaller loads.

Source: WRI

The adaptive utility

We’re also seeing regulated utilities adapting to reduce their own generation emissions with voluntary pledges of up to 80 percent emission reductions by 2030. Colorado’s Xcel Energy recently announced a commitment of 100 percent zero-carbon electricity by 2050. Even 75 percent of Midwest investor-owned utilities have set voluntary goals beyond what is required by states. This opens up more opportunities for corporate customers to collaborate with the utilities on the next generation of solutions, and then drive toward greening the grid.

Policy conditions support the market

None of this is possible without the policy framework in which the utilities exist. The right policy conditions have been made available to the corporate client in 26 states. Every state has different types of NGOs working with local and regional regulators. State policy is going to be a major issue for 2019, as the market has already seen from the midterm elections.

Source: WWF

Nationally, as we look toward the phaseouts of the investment tax credit (ITC) and production tax credit (PTC), we must look ahead on how it changes corporate renewable procurement timing. When polled, almost half the buyers indicated that their procurement timing is going to speed up as a result of pending phaseouts. Yet a part of the market has still not made up its mind on deal closures, with 17 percent of those polled showing uncertainty. The market not knowing the timing of closing PPAs demonstrates some potential volatility from post-tax credits, or could indicate suppliers may have time to find other ways to still obtain financing as renewable prices keep lowering.

The power of a collective YES

The power of partnership results in a record year thus far in 2018. With transactions tipping past the 6 GW mark, we believe that at this rate corporate buyers of renewable energy can realize an important goal of a collective 60 GW sum by 2025. Buyer records and sector diversification also mean a healthy market. Correspondingly, suppliers have been willing to listen to their corporate customers, change, and adapt. At the same time, utilities and policy rise to meet customer demand.

The complexity of the PPA is actually quite simple. The power purchase agreement exists only because of the word “agreement.”

Every market player—buyer or seller—is the true “power” behind these transactional agreements. Emphasis has been on the terms and conditions around the power purchase, yet the most compelling aspect of the transactions is the fact that a multitude of stakeholders have come to a unified YES. Agreements in the project deal process run the gamut from internal executive buy-in to finding the right price and risk conditions. Lastly, the willingness for utilities and developers to agree to expand their business model beyond a one-size-fits-all approach is clearly the next trend for 2019. With the corporate RE purchasing market so consistently growing, diversifying, and maturing, we can all continue to agree and remain hopeful for what the next five years will bring.

Authors

Lily Donge

Alexander Klonick

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.