Learn how we are working to transform how we use and produce energy.

Tackling Investment Risks to Accelerate Green Hydrogen Deployment in the EU

Why do we need subsidies if green hydrogen is already competitive with fossil-based grey hydrogen?

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

In her State of the Union address, the President of the European Commission announced that a European Hydrogen Bank will soon be established to guarantee the purchase of hydrogen in the bloc. Support for the green fuel is timely – with natural gas prices lingering at all-time highs in Europe, energy intensive manufacturing industries are ready to buy green hydrogen instead of fossil fuel alternatives. If green hydrogen were widely available right now, fuel switching could save these industries hundreds of Euros per ton of product.

But manufacturers of chemicals and fertilizers cannot currently procure the levels of green hydrogen they need for production, and relief for European industries will depend on how quickly the continent can scale up its green hydrogen supply. Mobilizing €330 billion to €400 billion (US$320 billion to US$390 billion) of private investment in renewables and electrolyzers could bring 20 million tons of green hydrogen to European markets by 2030, but two key investment risks are still preventing suppliers from advancing beyond demonstration projects and deploying green hydrogen at industrial scale:

- Because green hydrogen will not only compete with gray hydrogen but also with oil, natural gas, and coal, market risk prevents potential off-takers from signing on to contracts that might lock them into paying higher-than-market rates for fuel.

- First-mover risk prevents early market participants from investing in projects where high electrolyzer costs drive up capacity expenditure, potentially rendering these projects uncompetitive due to falling technology costs in the long term.

Funding from the European Hydrogen Bank – supplemented by additional targeted subsidy schemes – can mitigate these risks and accelerate green hydrogen market development in the EU. The sooner green hydrogen can reach economies of scale, the sooner it can deliver tangible security and sustainability benefits for Europe’s energy-strained industrial and transport sectors.

Enabling Market Uptake

Suppliers of green hydrogen need to have confidence that consumers will be willing to pay for their product, while consumers need to ensure that paying potentially higher costs for green hydrogen in the short term will not make them less competitive with peers using standard fuels.

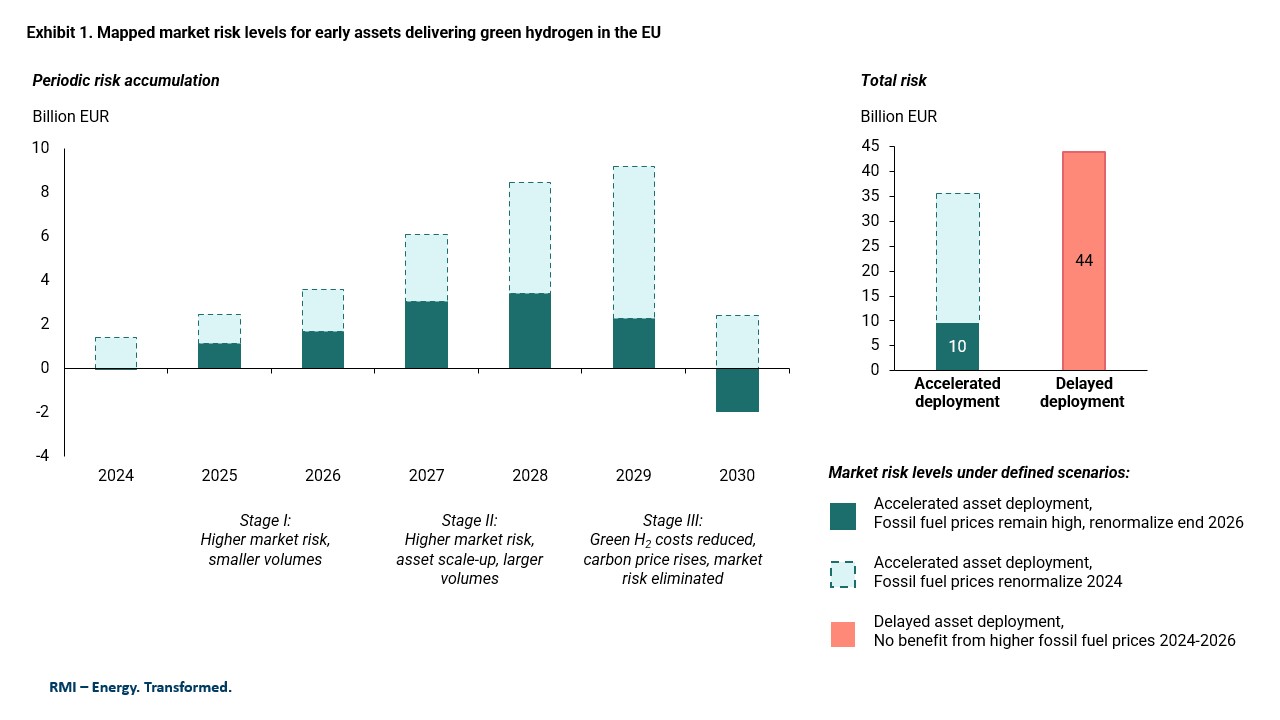

While green hydrogen is already competitive with gray hydrogen in Europe, it’s still more expensive in direct competition with fuels like natural gas, crude oil, and coal, which it will displace across several sectors. Capitalizing on currently high energy prices, a ~€10 billion cumulative investment between 2024 and 2029 could offset projected market risk and close price gaps to make green hydrogen competitive with the fossil-based fuels it would replace.

The cost gap between deploying traditional fuels to meet demand versus deploying green hydrogen will depend on the evolution of fossil fuel prices and on rising EU carbon prices. Given Europe’s ongoing energy crisis, current futures indicate that fuel prices will stay high at least until 2026 before renormalizing to average levels. At the same time, the carbon price under the EU Emissions Trading Scheme (ETS) is projected to rise from €80/ton today up to €140/ton by 2030. This carbon price will drive up the costs of fossil fuels, negating market risk for green hydrogen.

Sources: RMI analysis, adapted from the Green Hydrogen Taskforce White Paper

Exhibit 1 shows how cumulative market risk will likely build as higher volumes of green hydrogen are deployed in the EU, until rising carbon prices drive fossil fuel costs above green hydrogen costs in 2030, negating market risk. If — contrary to natural gas, coal, and oil futures — fossil fuel prices renormalize to lower levels as early as 2024, the gap between green hydrogen and standard fuel costs will expand and cumulative market risk will increase. The ranges in Exhibit 1 indicate how market risk will increase further if deployment is delayed by a few years, stalling green hydrogen cost reduction while fuel prices fall back to average rates. The EU can save billions in offsetting price risks for hydrogen by investing early and deploying assets as quickly as possible while natural gas, oil, and coal prices remain high.

Supporting First Movers

Ambitious market players are poised to invest in the technologies and infrastructure that will form the backbone of an early green hydrogen economy, but they require public support and reassurance from policymakers that the higher costs they incur will not eventually price them out of competition.

The costs of green hydrogen production and transport will drop as the market matures and economies of scale are reached, and first-mover risk for early assets will depend on the rate of cost decline. Suppliers and consumers who drive early buildup of the green hydrogen market this decade risk locking themselves into contract prices that will eventually exceed market prices.

First-mover risk will accrue as hydrogen production capacity builds up at costs above the expected 2030 market price for green hydrogen. Risk can be distributed by building up most capacity in later years, when costs are lower, but it’s important that sufficient capacity is built up early to achieve learning curves and scaling benefits, both so that technology costs can fall at projected rates and so green hydrogen can meaningfully bolster short-term energy security. Achieving desired cost reduction rates requires building up capacity that can deliver at least ~3 million tons per year (Mtpa) by the end of 2027.

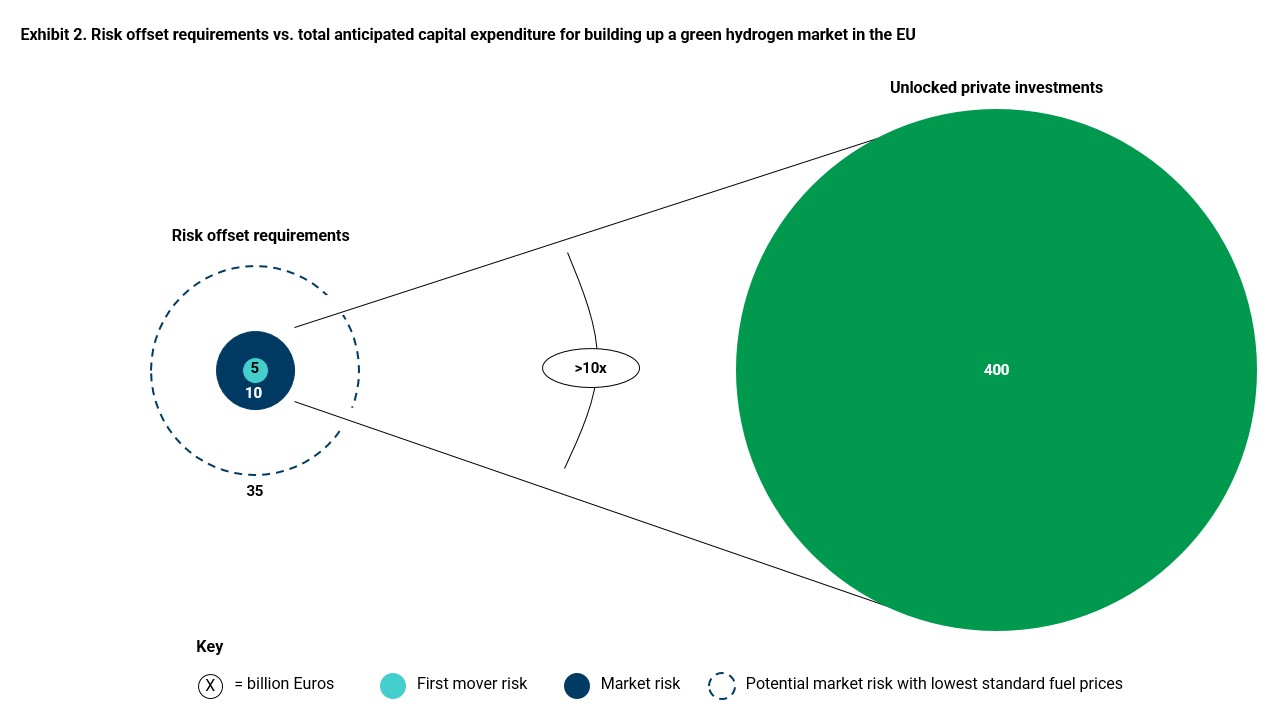

After 2030, first-mover risk will fall to zero and new assets coming on line will deliver green hydrogen in the EU at market prices. But to keep early capacity competitive and operational, producers will require between €3.5-5 billion/year in public financial support. Support to offset first-mover risk will only be needed until early assets are retired.

Risk-sharing mechanisms can remove barriers to the early investments required to quickly scale up green hydrogen deployment. Combining public subsidies that bridge investment gaps with private-sector risk management can effectively defray first-mover risk.

Capitalizing on Significant Opportunity

The EU stands to gain from supporting early producers and users of green hydrogen: spending up to €15 billion to offset investment risks between now and 2030 could generate more than 20 times as much private spending on advanced clean energy technologies. Project financing directed toward EU manufacturers of electrolyzers and renewables will likely reach €330 billion to €400 billion, as illustrated in Exhibit 2.

Sources: RMI analysis, adapted from the Green Hydrogen Taskforce White Paper

The European Hydrogen Bank will initially spend €3 billion in capital to create demand certainty in the EU’s growing hydrogen market. By leveraging additional funding from the Innovation Fund over the next decade, the bank can fully offset investment risks for early market players who are ready to switch to green hydrogen.

Critically, funding should be ramped up to remove first-mover and market risks as soon as possible to capitalize on momentum for fuel switching while gas, coal, and oil prices remain high. If the EU can kick-start its green fuel market now, falling technology costs and rising carbon prices will ensure green hydrogen rapidly and permanently outcompetes fossil alternatives.

Related Insights

Advance Market Commitments Today Can Build a Low-Carbon Tomorrow

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.