Learn how we are working to transform how we use and produce energy.

Sunshine for Mines: A Brighter Vision for Sustainable Resources

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

In both life and work, it’s important to reflect on your past accomplishments and how they inform your future journey. When RMI started its mining initiative five years ago, carbon reduction wasn’t on the radar for mining companies, and the renewable capacity on (or provided to) mine sites was just over 600 megawatts. In most instances, the barrier to change was not cost, but the industry’s comfort with traditional practices. The industry status quo was to use grid power were possible, and diesel, heavy fuel oil (HFO) or natural gas everywhere else.

RMI’s Sunshine for Mines initiative was initially launched to accelerate the adoption of renewables on mine sites to 1.4 gigawatts (GW) by 2022. At the time of publishing our first blog (“Missing a Mining Opportunity”) in 2015, we knew that this would require several successful pilots and a deliberate effort to reshape industry culture.

Times have changed. Mines have already exceeded the 1.4 GW goal, and by the end of 2019 there was 4.9 GW of renewable capacity installed or announced. RMI played an active role in this transition, using a data-driven approach to underline the value in renewable energy on mine sites. As RMI’s relationships and understanding of the sector grew, so did the breadth of our efforts. From looking at solar on active mine sites, we expanded to study zero-carbon hauling, closed mine sites, nascent technologies, and community engagement as levers to decarbonize the mining industry and preserve companies’ social license to operate.

But it’s still not enough. The demand and scale of moving the mining industry to a 1.5°C carbon pathway require us to continually re-consider our approach and goals. The mining industry itself is realizing this challenge as well. In 2019, carbon reduction ranked in the top five risks facing mining and metals companies. Our future work is fundamentally focused on meeting this challenge.

Accomplishments/Where We Are Now

Sunshine for Mines played a key role in studying and socializing the benefits of renewable energy on mine sites. These learnings were developed through direct engagements with the industry, including four of the top ten largest mining companies in the world. Each project provided valuable insights we then brought to the wider industry.

A 2015 study for Gold Fields showed how a large solar and storage system was already competitive with grid energy costs, and also enhanced power reliability. In 2017 we worked with BHP on their portfolio of 22 legacy mines in North America and identified potential for over 500 MW of new renewable energy generation. Over time and with more mining companies, RMI screened an additional 13 mine sites for renewables integration, performed pre-feasibility assessments and identified dozens of economically and technically viable renewable energy projects.

In addition to direct advisory work, the mining team shared our lessons learned widely. Our renewables on mines tracker, besides demonstrating the growth of renewables, has become a go-to industry source. We’ve grown a dedicated readership of those interested in the mining industry, and through study and consultation with mining and electricity markets across the globe, we’ve seen several trends emerge, many of which are promising over the longer term:

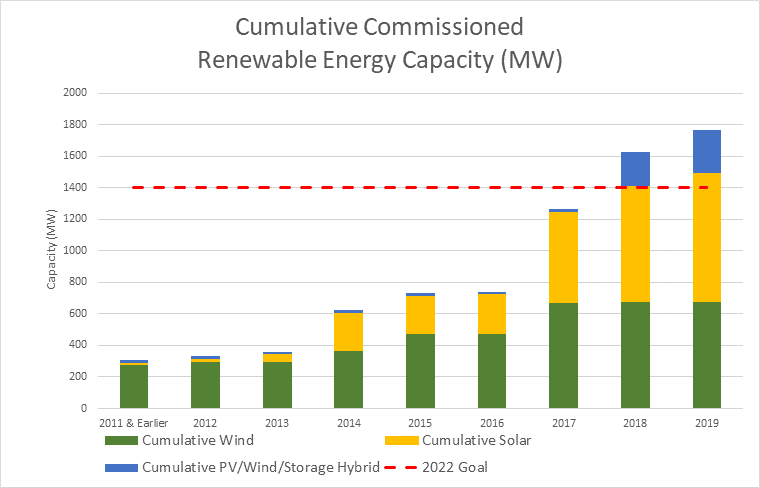

1. Renewables on mine sites blew past 2015 estimates, outpacing growth compared to the rest of the world, with cumulative commissioned capacity surpassing 1.7 GW, far beyond the 1.4 GW goal set for 2022:

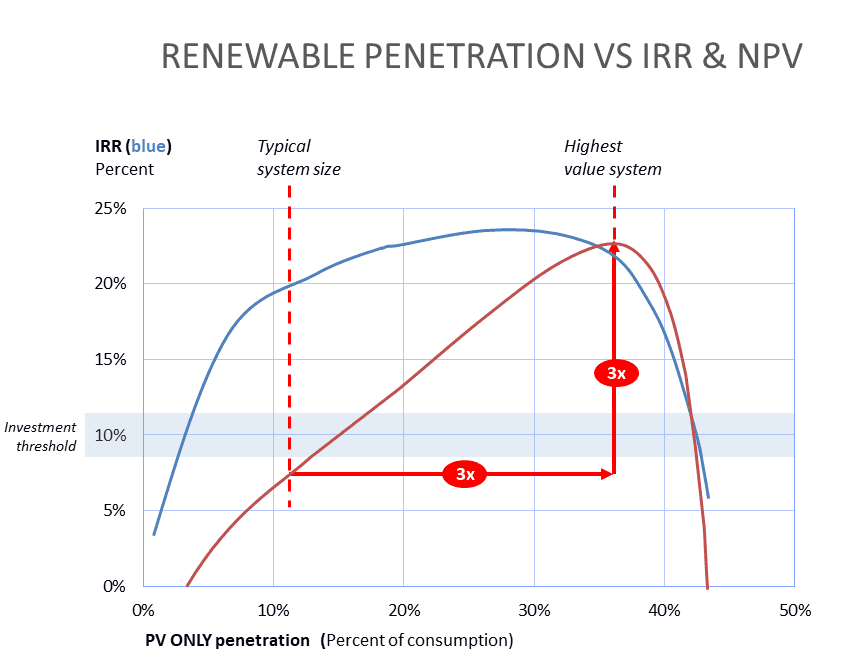

2. Despite the substantial Net Present Value that is generated when building solar installations that offset larger portions of electricity supply, we’ve found that mining companies are still opting for smaller systems and leaving money on the table:

2. Despite the substantial Net Present Value that is generated when building solar installations that offset larger portions of electricity supply, we’ve found that mining companies are still opting for smaller systems and leaving money on the table:

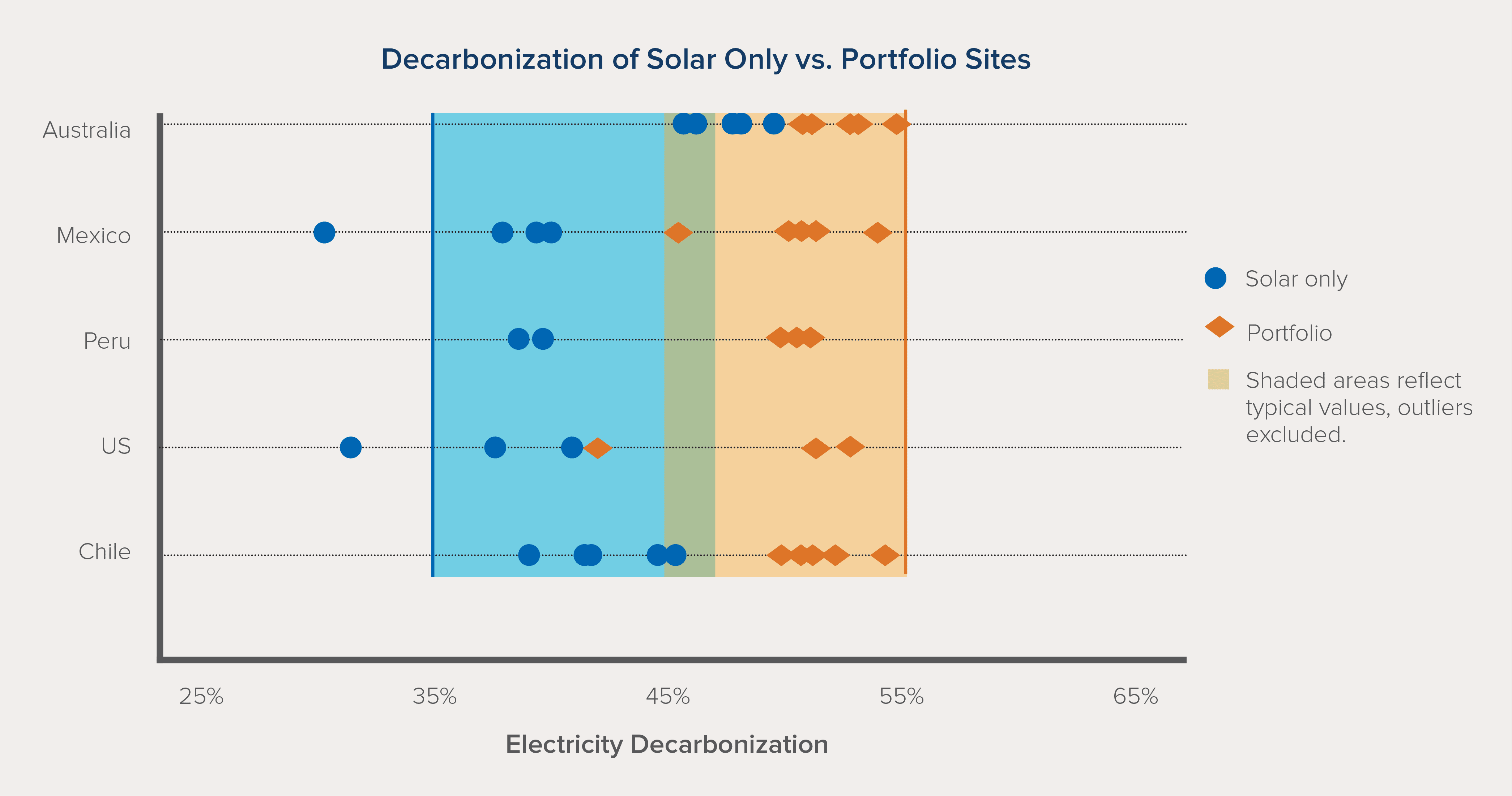

3. When using high penetration solar PV as a base (shown in blue across five key mining geographies), 45 percent decarbonization of a mine’s electricity supply can be achieved with positive financial returns when another technology like wind power or energy storage is introduced (shown in orange):

Challenges still remain. Despite clear economic incentives to look into demand response, shifting operations to reshape demand profiles is a taboo that the industry has not yet found an effective way to break.

Additionally, looking to 2050, the mining industry assumes that resource demand will increase dramatically for most minerals and metals, but this ignores the large untapped potential of resource efficiency. Companies have shown time and again their ability to dramatically decrease, or obviate entirely, their reliance on expensive or hard to obtain materials. Intentional design choices can accelerate this change as well.

Without resource efficiency, the mining industry will face increasing tension between resource demand and decarbonization. Broadly, the industry can: 1) Adopt slower growth, 2) Miss their Paris target commitments, or 3) Significantly decarbonize operations and provide clear market incentives and information to buyers to support downstream decarbonization and resource efficiency developments.

Future of the Mining Team

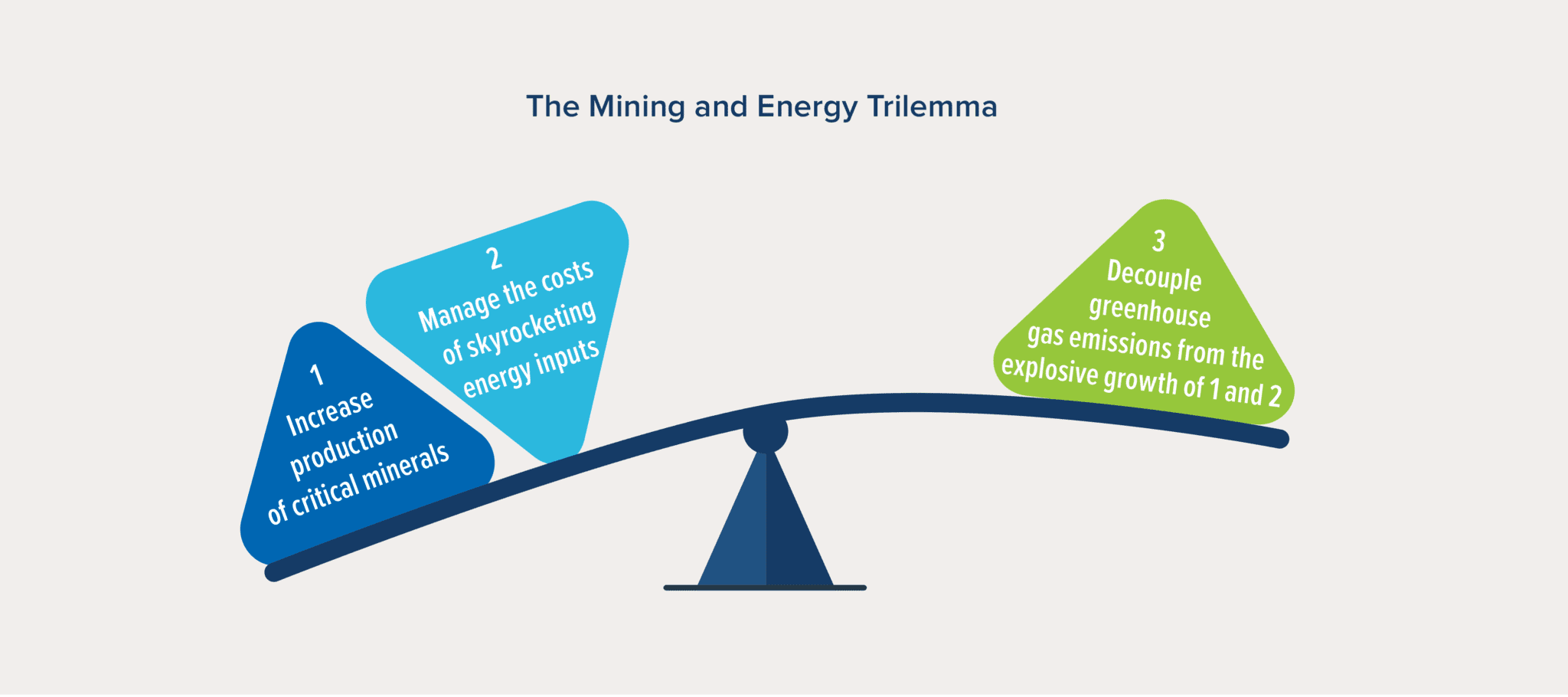

Based on our work, the original barriers to renewable energy deployment on mines have been overcome. But unfortunately, despite the strides made by the mining industry, changing how mines are powered is not enough to reach the level of decarbonization needed to limit warming to 1.5°C. The mining industry is facing what we call the Mining and Energy Trilemma, as discussed in the RMI report: “Low Carbon Metals for a Low Carbon World”. In the next three decades, the sector needs to (1) increase production of critical minerals, (2) manage the costs of skyrocketing energy inputs, and (3) decouple greenhouse gas emissions from the explosive growth of (1) and (2).

In years past, the mining team collaborated with companies on a technology-driven “push” — advancing breakthroughs in low carbon technologies and process design — to drive awareness and adoption of renewables. But in order to overcome the Mining and Energy Trilemma and enable the next step-change, our team must also generate a market “pull” that will create a demand for low-carbon goods to pull the industries toward the adoption of decarbonization technologies.

To enable this deeper change, there are three key challenges to overcome:

- Insufficient modeling capability to support high optimal penetration of renewables and electrification

- Lack of transparency of product performance and embodied emissions

- Insufficient market incentives

What does this mean for the future of our work? To address these three challenges, we are focusing our efforts through a three-pronged approach. First, we are continuing to work directly with mining companies, but focusing on broader decarbonization strategies including corporate governance, risk management, mine efficiency and electrification, and optimized renewable asset development.

Second, we are targeting a foundational obstacle to reducing carbon emissions, and one of RMI’s “Seven Challenges For Energy Transformation”: making emissions visible. Due to the nature of deep and global supply chains, neither consumers, corporates, or financial institutions know the embodied emissions in the products they produce or sell. As a founding member of COMET (Coalition on Materials Emissions Transparency), we can drive collaboration with key stakeholders and a growing number of initiatives rising to decarbonize material goods. By facilitating the development of platforms that apply data and analytics to specific opportunities, parties can independently track, verify, and analyze climate and energy data in specific sectors and locations.

The third piece of our strategy will capitalize on carbon transparency to create market incentives for low- and zero-carbon products. We believe that a differentiated market across material supply-chains for these products will allow buyers to express their preference and lead to an economic incentive for miners to provide low- and zero-carbon products and for companies to design their products in more resource-efficient ways.

We have achieved and exceeded the original vision for Sunshine for Mines: to increase the adoption of renewable energy, solar PV in particular, at mine sites. We now believe it necessary to set an even more ambitious goal based on putting the mining industry on a 1.5°C pathway. Our new goals are:

- 50 percent reduction in global absolute mine emissions by 2030: From 0.91 Gt to 0.45 Gt or less

- 50 percent of global mine electricity supplied by renewables by 2030

We call this 50 by 2030. Meeting these goals will not be easy, but they are essential to ensuring the sustainability and economic security of the mining industry. Miners time and time again have shown incredible resiliency and adaptability, while operating in some of the harshest conditions on Earth. Now, we are asking the industry to acknowledge both the urgency of climate change and the need for decarbonized materials and resources to enable the energy transition low-carbon economies. The RMI Mining team will be there through this transition and we hope you’ll be there with us.

To stay in touch with us in the future and join our mailing list, email Thomas Kirk at tkirk@rmi.org.

Related Insights

Advance Market Commitments Today Can Build a Low-Carbon Tomorrow

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.