Learn how we are working to transform how we use and produce energy.

Report Release: The Economics of Clean Energy Portfolios

How portfolios of renewable and distributed energy resources can help avoid $1 trillion of costs for new gas-fired power plants in the US

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Download RMI’s new report, The Economics of Clean Energy Portfolios

The US power system is one of the largest, most complicated, and most expensive machines in the world, but the grid’s core infrastructure is old and is not aging gracefully. Nearly 500 gigawatts (GW), or about half of the existing thermal generator fleet (i.e., coal-, nuclear-, and gas-fired power plants) is likely to retire by 2030, leading to a gap in capacity that will need to be addressed with new investment.

The default choice for utilities and merchant generators operating in competitive markets to replace retiring generators is construction of new natural gas-fired power plants. Gas-fired generation technology is mature and cost-effective compared to older, retiring generators, especially with the currently low (but inherently volatile) price of natural gas. However, given the size of the coming wave of retirements, approximately $500 billion of investment would be needed through 2030 to replace all retiring capacity with new gas. This investment would lock in another $400 billion to $500 billion in fuel costs, and 5 billion tons of CO2 emissions in the same period.

Thankfully, new gas plants are not the only option the US has. In a new report released today, Rocky Mountain Institute examines the potential role of “clean energy portfolios,” or collections of renewable energy and distributed energy resources (DERs) that can provide the same grid services as new gas plants. RMI’s analysis finds that, because of recent innovation and rapid cost declines in renewable energy and DER technologies, clean energy portfolios can often be procured at significant net cost savings, with lower risk and zero carbon and air emissions, compared to building a new gas plant. More dramatically, the new-build costs of clean energy portfolios are falling quickly, and likely to beat just the operating costs of efficient gas-fired power plants within the next two decades—a sobering risk for investors and customers in a market with over $100 billion of already announced investment in new gas-fired power plants.

Significant Cost Savings across Diverse Case Studies

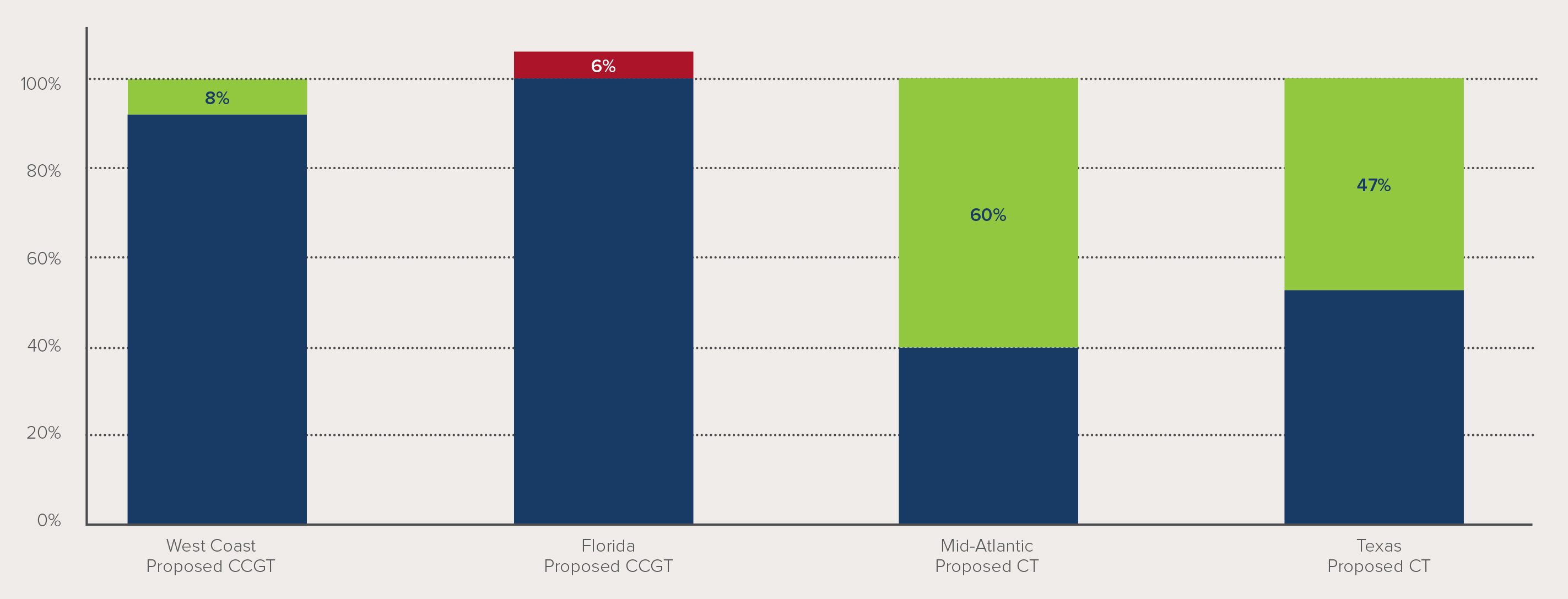

RMI examined four case studies of proposed gas plants from utilities across the US. These cases included two combined-cycle gas turbine (CCGT) power plants, planned for high-capacity factor operation, and two combustion turbine power plants, planned for peak-hour operation. These power plants are proposed for a wide variety of regions with different resource availability, resource costs, climate- and weather-driven demand needs, and customer bases.

In all four cases, RMI found clean energy portfolios to be cost-competitive with proposed gas-fired generation, while meeting all required grid services and supporting system-level reliability. In three of the four cases, optimized, region-specific clean energy portfolios cost 8–60 percent less than the proposed gas plant, based on industry-standard cost forecasts and without subsidies. In only one case was the clean energy portfolio’s cost slightly higher than the proposed gas plant. However, further analysis revealed that modest carbon pricing (i.e., < $8/ton) or feasible community-scale solar cost reductions would easily reverse the result. Similarly, two more years of anticipated renewable and storage cost reductions would also eliminate the difference in cost between the clean energy portfolio and the gas plant.

Our study also included several conservative assumptions that overestimated the cost and underestimated the benefits of the clean energy portfolios. By using an asset-specific paradigm, the analysis limited the possible savings from economies of scope that are possible with integrated system-level planning. We also assigned zero value to existing incentives (e.g., tax credits), carbon emissions reductions, fuel price volatility reductions, and transmission- and distribution-level benefits that could be harnessed by clean energy portfolios.

A $350 Billion Dollar Investment Opportunity

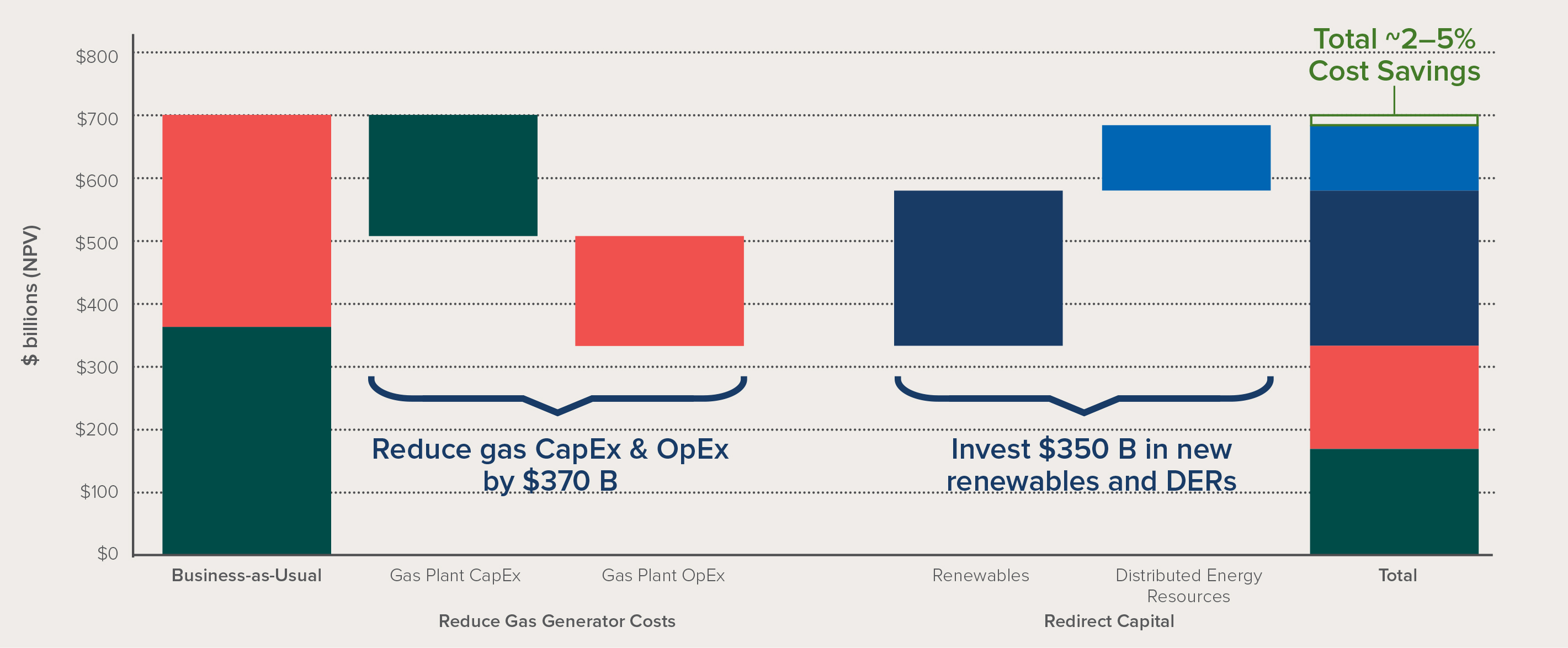

Expanding the analysis to the entire US market, RMI found an opportunity to reduce total grid costs by avoiding at least $370 billion in new gas plant investment and operating costs, and redirecting those savings to investment in renewable energy and DERs.

RMI examined a scenario where more than half of retiring thermal capacity through 2030 was replaced by portfolios of resources that can provide the same energy, peak capacity, and flexibility to the grid, using conservative assumptions of both renewable and DER adoption. This pathway would unlock a $350 billion market for renewables and DERs through 2030, while avoiding 3.5 billion tons of CO2 emissions over the same time period.

Gas Plants Could Face Profitability Threats

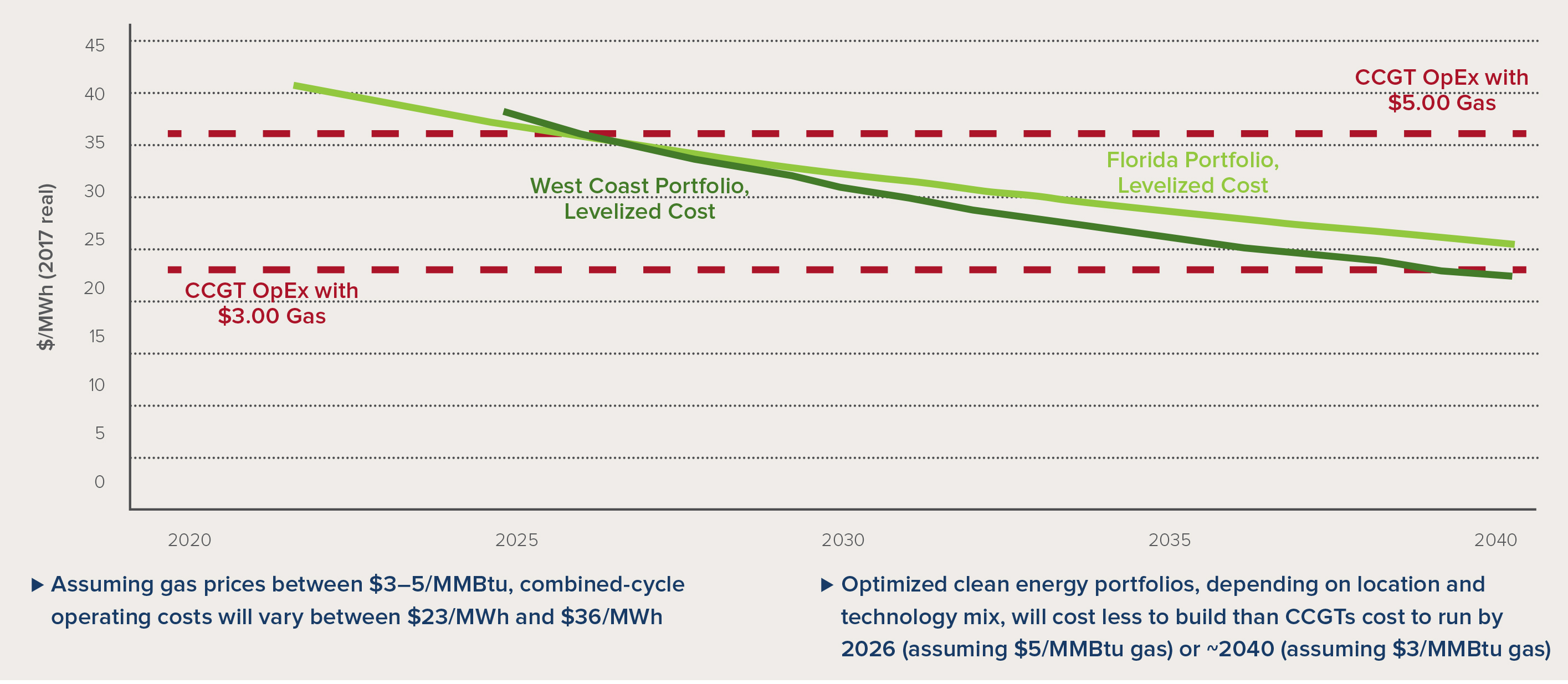

In addition to suggesting a clear cost-saving opportunity to reshape investment in the US power sector, the analysis also suggests that existing gas plants, and any built in the future, could face profitability threats in the near term. Because of expected cost declines in renewable energy and battery storage technology, we expect the costs of optimized clean energy portfolios to fall by ~40% within the next 20 years. Depending on the price of natural gas, the falling costs of clean energy portfolios will begin to outcompete just the operating costs of a highly efficient gas plant by 2026 (if gas prices rise to averages observed from 2003–2008, potentially driven by an emerging export market for liquefied natural gas) or by ~2040 (if gas prices stay at currently low levels).

In other words, within the next 10–20 years, it will likely be less expensive to build entirely new clean energy portfolios that can perform the same grid services as a gas plant than it will be to run existing gas plants. The result of this will be fewer operating hours and eroded revenue for owners of gas-fired power plants in the US. Investors in new gas-fired generation should carefully consider this emerging dynamic as they evaluate making multibillion-dollar bets on new projects.

Near-Term Action Can Unlock Opportunity and Mitigate Risk

With over $100 billion in planned investment in new natural gas-fired power plants already announced for construction by the mid-2020s, there is a narrow window of opportunity to avoid imposing stranded asset risks on merchant power plant investors (in restructured markets) or utility customers themselves (in vertically integrated states). Regulators, market operators, utilities, and technology providers all have a role to play in realizing this opportunity:

- State regulators should carefully consider alternatives to approving cost recovery for new gas generation, taking into account the most up-to-date pricing and capability data for alternatives, including battery energy storage, utility-scale and distributed solar photovoltaics, next-generation demand flexibility technologies, and targeted energy efficiency programs.

- Market operators and state regulators should align investment incentives with least-cost outcomes. In restructured markets, market operators can transition toward market products that allow the participation of distributed resources, and that don’t force these increasingly cost-effective technologies into product definitions originally designed for thermal generators. In vertically integrated markets, regulators can adjust the utility business model to remove a bias toward utility-owned assets and enable a competitive market for grid services.

- Utilities can revolutionize resource planning and procurement practices to accurately value the capabilities of renewable and distributed energy technologies, and minimize the “soft costs” of integration and deployment. The utility planning paradigm has long resulted in large-scale generation investments to meet continually growing demand; now that demand is flat and large-scale generation is no longer the most cost-effective option, there is a clear opportunity to update processes to reflect the new reality.

- Technology and service providers can offer resource portfolios that meet grid needs, either individually or as part of optimized portfolios, and continue to drive down soft costs that may limit the cost-effectiveness of aggregated resource portfolios. Service providers can also build confidence in nontraditional solutions (e.g., inverter-based reliability services) by publicly and transparently sharing results and best practices.

If the opportunity afforded by the current investment cycle is missed, the United States risks locking in costs and carbon emissions for generations to come. By seizing on the improving economics of clean energy resources, the electricity industry can avoid locking in at least $370 billion in investment and fuel costs for new gas plants, reprioritize investment in clean energy resources, and avoid 3.5 billion tons of CO2 emissions through 2030.

Image courtesy of iStock.

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.