Learn how we are working to transform how we use and produce energy.

As Oil Prices Gyrate, Underlying Trends Are Shifting To Oil’s Disadvantage

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

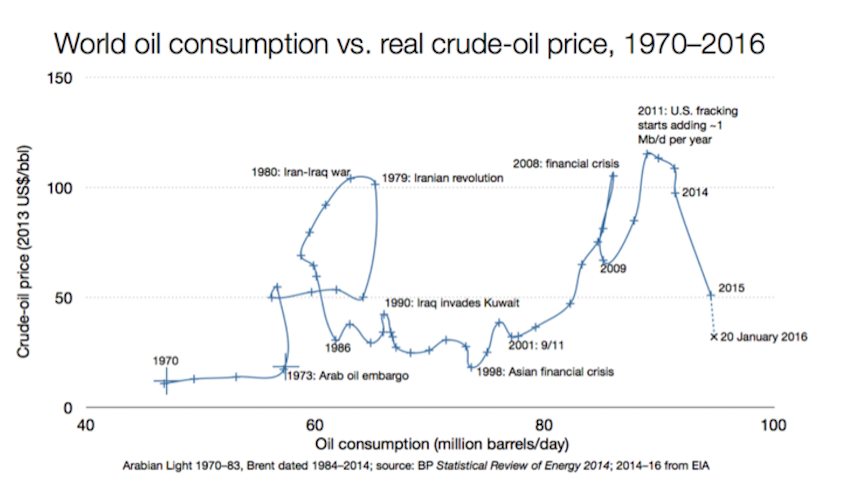

Why should equity markets tank when oil prices do? Beats me. Among many sources of jitters, this shouldn’t be a big one (though The Economist demurs). When oil prices fall 70+ percent, oil companies and their lenders and investors suffer, so do oil-dependent communities, but oil users (far more numerous) rejoice and respend. The net macroeconomic effect sounds as positive as the middle-class tax cut that it effectively is — the OPEC-monopoly-rent tax that Congress has long seemed determined to pay to the Saudis rather than to the Treasury, finally if accidentally being respent at home.

Surely investors understand — don’t they? — that oil is a commodity. As I explained elsewhere, oil prices go down because they went up before, and they go up because they went down before. Get used to it. Commodities do that; it’s their job. If you don’t like it, don’t buy them. Buy constant-price, and usually cheaper, efficiency and renewables instead, as the national and global market is doing. Then you can avoid loop-the-loop roller-coaster rides and get your energy services cheaper, cleaner, and more reliably.

Those who claimed low oil prices would crash renewables (other than biofuels) were wrong. The reason is simple. Wind and solar power make electricity. Oil makes less than four percent of world and under one percent of U.S. electricity, so oil has almost nothing to do with electricity. Thus in 2015, as oil prices kept skidding, global additions of renewable power set a new record, adding about 121 GW of wind and solar power alone. Renewables’ $329 billion investment was up 4% from 2014, says Bloomberg New Energy Finance (which tracks each transaction), but it added 30 percent more capacity because renewables got much cheaper. Solar power is booming even in the Persian Gulf, where it beats $20 oil.

Natural gas does compete with solar and windpower, and its price tends to move with oil’s, but cheaper gas doesn’t much affect renewable power either. That’s because new wind and solar power often beat even the operating costs of the most efficient gas-fired power plants anyway, even without counting the market value of gas’s price volatility.

Yet as oil prices gyrate, it’s important to understand that underlying trends are shifting too, to oil’s disadvantage. It’s happened before. In the 1850s, whalers—America’s fifth-largest industry—were astounded to run out of customers before they ran out of whales. Over five-sixths of their dominant market (lighting) vanished to competitors—oil and gas both synthesized from coal—in the nine years before Drake struck “rock oil” (petroleum) in Pennsylvania in 1859. Two decades later, Edison’s electric lamp beat whale oil, coal oil, town gas, and John D. Rockefeller’s lighting kerosene. Today in turn, most traditional lighting is being displaced by white LEDs, which each decade get 30x more efficient, 20x brighter, and 10x cheaper. By 2020 they should own about two-thirds of the world’s general lighting market.

LEDs inside-out are PVs—photovoltaics, turning light into electricity. PVs often, and very soon generally, beat just the fossil-fuel cost of running traditional power plants. PVs are now less capital-intensive than Arctic oil, not counting the ability to use electrons more effectively than molecules. Costly frontier hydrocarbons like Arctic oil can’t sell for a high enough price to repay their costs. Their revenue model has been upside-down for years. Had Shell persevered instead of abandoning its $7-billion Arctic investment, and had it found oil, it wouldn’t have won durable profits.

Oil companies since 1860 and electric utilities since 1892 have sold energy commodities—molecules or electrons—rather than the services customers want, such as illumination, mobility, hot showers, and cold beer. This business model means that when customers use the energy commodity more efficiently to produce the service they want, the provider loses revenue, not cost. That’s bad for both electric utilities and hydrocarbon companies, because most (and for oil, ultimately all) of the commodity they sell can be displaced by far cheaper energy productivity.

That displacement is already well underway. Renewable electricity merits and gets lots of headlines, but in 2014 it raised U.S. energy supplies only a third as much as the energy saved in the same year by greater efficiency. Over the past 40 years, Americans have saved 31 times as much energy as renewables added. Those cumulative savings are equivalent to 21 years’ current energy use. They’re simply invisible: you can’t see the energy you don’t use. But globally, it’s a bigger “supply” than oil, and inexorably, it’s going to get much, much bigger.

Oil companies worry about climate regulation, but they’re even more at risk from market competition. The oil that’ll be unburnable for climate reasons is probably less than the oil that’ll be unsellable because efficiency and renewables can do the same job cheaper. An oil business that sputters when oil’s at $90 a barrel, swoons at $50, and dies at $30 will not do well against the $25 cost of getting U.S. mobility—or anyone else’s, since the technologies are fungible—completely off oil by 2050. That cost, like the $18 per saved barrel to make U.S. automobiles uncompromised, attractive, cost-effective, and oil-free, is a 2010–11 analytic result; today’s costs are even lower and continue to fall.

In short, like whale oil in the 1850s, oil is becoming uncompetitive even at low prices before it became unavailable even at high prices. Today’s oil glut, we hear, is caused by fracking, a bit by Canadian tar sands, and most of all by the Saudis’ awkward (though impeccably logical) unwillingness to give up their market share to higher-cost competitors. But less noticed, and equally important, is that demand has not lived up to irrationally exuberant forecasts.

Gasoline demand has trended down in the U.S. for the past eight years and in Europe for the past ten, for fundamental and durable reasons of technology, urban form, shifting values, and superior ways to get mobility and access. Suppliers have invested to supply more oil than customers want to buy. Had crimped budgets not curtailed investment budgets, oil companies would still be building pre-stranded production assets as fast as they could.

As frontier oil becomes costlier while accelerating demand-side innovations spread from rich to developing countries, led by China, oil companies face discouraging fundamentals. They’re stuck with the least attractive 6% of global reserves while parastatals keep the rest, and even that last 6% can be confiscated or taxed away at any time. Oil companies are price takers in a volatile market. They’re extraordinarily capital-intensive. They have decadal lead times. They have high technical, geological, and political risks. They’re politically fraught and interfered with; some firms have also suffered self-inflicted reputational damage that sullies the rest. Oil companies’ shrinking reserves and geographies force them into riskier and costlier projects while investors demand lower risk and higher return. Their service companies have turned into formidable competitors. Their permanent subsidies are coming under scrutiny and pressure. Most of the reserves underpinning their balance sheets are unburnable or unsellable or both—far costlier than demand-side competitors, even at today’s oil prices, and increasingly challenged even on the supply side—so financial regulators are sniffing around mark-to-market.

What a recipe for headaches! Why be in a business like that? With mature provinces in decline and fiercely contested, prices volatile, ingenuity strained, exploration pushed to the ends of the earth at spiraling cost and risk, and unforeseen competitors inexorably taking away demand, should hydrocarbon companies ignore, deny, resist, diversify, hedge, finance, transform, or decline? That strategic choice is stark, tough, and increasingly urgent.

And that’s before we add oil’s volatile geopolitics—focused chiefly on the world’s most unstable and dangerous region where a Rubik’s Cube of ancient feuds ensures that, as one expert famously taught, “However bad things are in the Middle East, they can always get worse.”

One troubling scenario concerns the brittleness of Saudi Arabia’s vital 10 million barrels of oil per day—5–10 times the world oil market’s surplus. Most Saudi oil flows through terminals at Ras Tanura and Ju‘aymah and through the Abqaiq processing plant (which al Qa‘eda tried to attack a decade ago and then planned to fly hijacked planes into). These highly concentrated facilities have also been attacked, so far ineffectually. It could take decades to fix damaged key components.

Who might want to do that? Da‘ish or al Qa‘eda would win a twofer: damaging Western economies and toppling the Saudi monarchy (whose export of intolerant Wahhabist ideology, ironically, inspired jihadism in the first place). Oil exporters severely damaged by low oil prices, such as bystanders Nigeria and Venezuela, lack capability to limit Saudi output. But two very interested neighbors might not.

Iran is right across the Gulf, with two big airbases a quarter-hour’s flight from the Saudi oil chokepoints. Iran is a bitter rival, the opposite pole of the tense Shi‘a-Sunni axis, and influential with the disaffected Shi‘a population that predominates in the eastern Saudi region around the main oilfields. Iran is currently in a tiff with the Saudi leadership. Its versatile and creative military and paramilitary forces and proxies don’t not always seem under full political control. Reentering the oil market with the lifting of nuclear sanctions, Iran would like to earn more money per barrel.

Also now active in the neighborhood is militarily formidable Russia—the world leader in secret, disguised, and proxy warfare. President Putin’s impressive ability to retain power by seeming to protect the Russian people from crises he manufactures cannot work without a viable domestic economy. At today’s oil price, Russia is likely to deplete its stability funds this year and its foreign reserves by about next year, so Mr. Putin may see a much higher oil price (plus lifted Ukraine sanctions) as an existential necessity.

Ras Tanura and Saudi Aramco have weathered cyberattacks. (Both Iran and Russia have lately cyberattacked their neighbors—Turkey and Ukraine respectively.) There are also many options for physical attack, some hard to forestall. So far, Saudi forces have defeated both cyber- and physical attacks on key oil facilities. But attackers need succeed only once, and they could be highly motivated.

A successful attack, strangling Saudi oil output for years (and then repeatable), could make oil prices soar more than they’ve plunged. Massive global inventories could help cushion the blow, efficiency and renewables could be surged, behaviors would change, but most of 10 million at-risk barrels per day lack ready replacements. Now, that could justify a skittish Dow.

All the more reason to buy efficiency and renewables instead of oil. We’ll profit more and sleep better.

This article originally appeared on Forbes.com.

Photo courtesy of IrenicRhonda via Flickr, Creative Commons license (CC BY-NC-ND 2.0).

Authors

Amory Lovins

Cofounder and Chairman EmeritusRelated Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.