Learn how we are working to transform how we use and produce energy.

Institutional Investors Can Make the Climate Transition Bloom in Latin America

New study shows that investing in climate-aligned transition funds does not mean incurring greater risk or giving up returns for institutional investors.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

What makes a “climate-aligned” or “Paris-aligned” investment? Interest in investments that align with climate change mitigation objectives is growing, but questions are increasingly being raised about what actual contribution to tackling climate change such investments make, and to what extent they can deliver longer-term investments that are more resilient to future transition risks.

A new study, funded by the International Climate Initiative (IKI), led by the PACTA team at RMI and involving leading Latin American asset manager SURA Investment Management, has explored how to design a “Paris-aligned” investment portfolio of listed securities in emerging markets and how a truly climate aligned investment product could be commercialized.

What makes an investment fund climate aligned?

While there have been many public statements by investors of their commitment to “align” their investments with 2030 and 2050 climate targets, there has been very limited analysis of what it means in practice to try and align a diversified portfolio allocation and whether it would even have an impact in the real economy.

The EU’s Climate and Paris-Aligned Benchmark Regulation of 2020 (EU CTB and EU PAB) was a first attempt to answer that question, setting economy-wide decarbonization targets for portfolios accompanied by exclusions for high CO2-emitting activities. But while fund products have sought to claim alignment with these benchmarks, the approach raises fundamental questions about how this alignment is measured across industrial sectors and whether it drives change in the real economy.

For portfolios of listed securities, it would be easy to manage transition risks by simply divesting from climate-critical sectors, but this will not drive the decarbonization of companies in these sectors. In fact, it could have unforeseen effects, restricting the development of the very companies that need to invest in and manage the necessary technology transitions. This is particularly important in emerging economies, where access to capital is already more restricted and where the investible universe available to investors is more limited.

At risk from climate change: Latin America requires capital to meet mitigation objectives

The transition of Latin America will require the active participation of capital providers in the transformation of the economy. It has been estimated that the region will require an investment of between 7 and 19 percent GDP annually (which is equivalent to between US$470 and US$1,300 million annually by 2030) in order to meet its Paris agreement goals.

According to the Intergovernmental Panel on Climate Change (IPCC), the climate emergency could put the region’s economic and social development at risk, accentuating the already complex social reality. Seeing the potential for mitigation to support development, Latin America (Latam) has witnessed in recent years a growing momentum and awareness of the connection between private capital flows, sustainable development initiatives and climate mitigation and adaptation objectives. Initiatives have included ambitious updates to Nationally Determined Contributions (NDCs) in Chile and Colombia, the development of national taxonomies in Colombia and Mexico, growth in the issuance of thematic bonds to over US$48.6 billion (2021), and new mandatory requirements to incorporate climate risk into investment decision-making in Mexico, Chile, and Colombia in the near future.

The scene is therefore set in Latin America for private investors to take a more active role in directing capital toward meeting climate mitigation objectives, which at the same time must also serve to contribute to the sustainable development of the region. And this is why deepening the discussion on investment alignment with the Paris agreement is necessary and timely.

The challenge: Build a Latin American-focused listed equity and corporate bond portfolio with a forward-looking perspective on climate performance.

To address the challenges of developing a climate-aligned fund, a pilot study was carried out to design prototype listed equity and corporate bond portfolios with an active, forward-looking perspective on portfolio climate performance. The study is based on an evaluation of over 200 Latin American listed equity and bond issuers, according to their alignment with below 2°C climate scenarios, where possible, and supplemented by their decarbonization commitments, plans, and emissions trajectories.

Working within the constraints of a fund intended for institutional investors and indexed to the Latam investible universe, the study has sought to answer fundamental questions about how such a fund could be designed, constructed, and managed, including:

- How can a priority focus on the climate performance of issuers in sectors critical in seeking to reduce CO2 emissions be ensured?

- How can a credible, forward-looking climate alignment of the underlying assets of its investee companies with Paris agreement compatible scenarios be measured and tracked?

- How can a fund manager maximize the impact of investment decisions on companies in the region, including leveraging their influence as an investor?

- Is it possible to construct a fund that provides for an acceptable management of the risk and returns when compared with a broad market benchmark?

How to build a climate-aligned fund

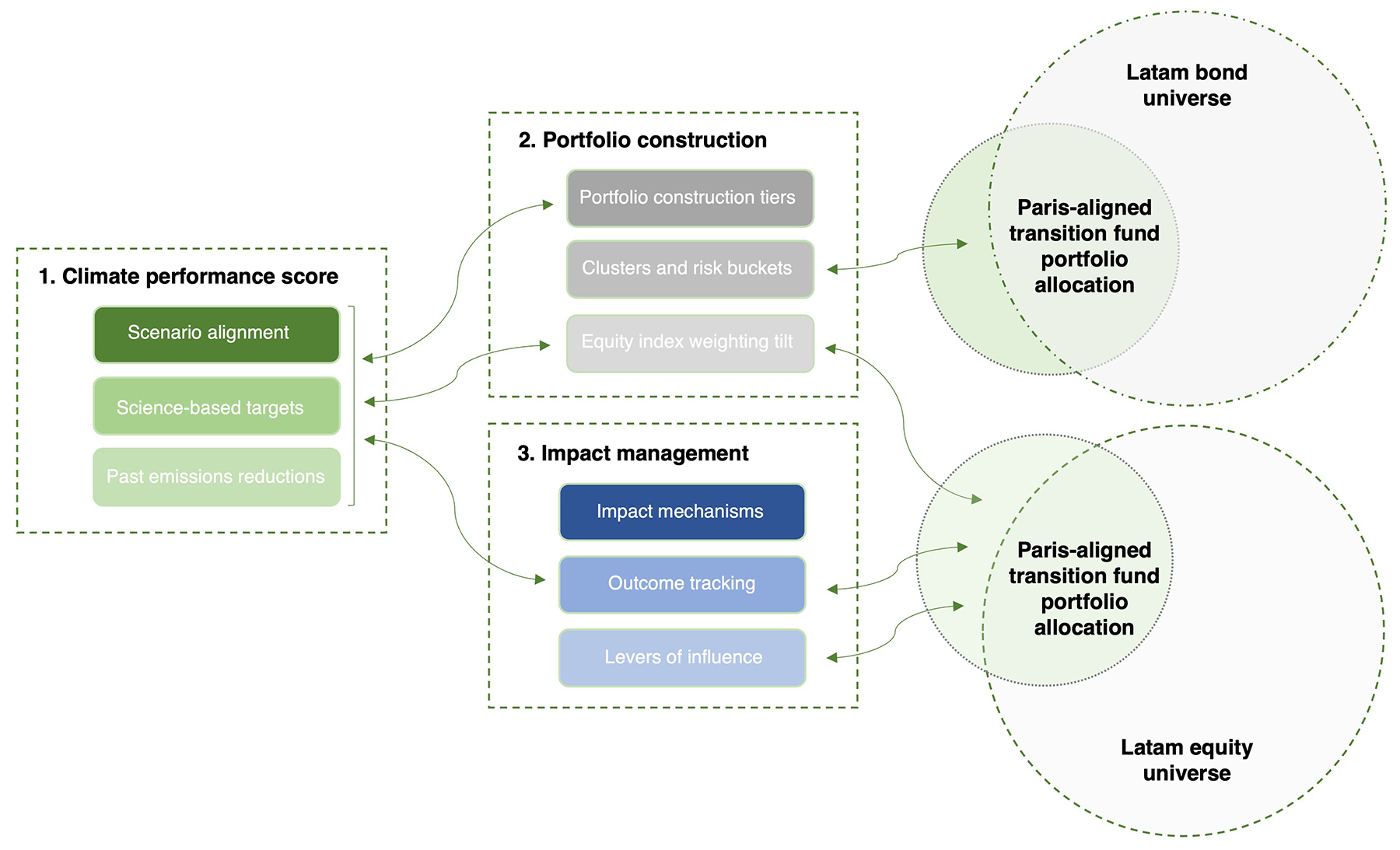

In order to explore how to design and construct a climate-aligned fund in the Latin American context, the study focused on three core components to test the climate and financial performance outcomes at investee and fund level, as well as the practical implications for the asset manager. Exhibit 1 illustrates the relationship between the three core components of the design process.

Exhibit 1. Core components of a Paris-aligned transition fund design

Step 1. Design a climate performance evaluation system

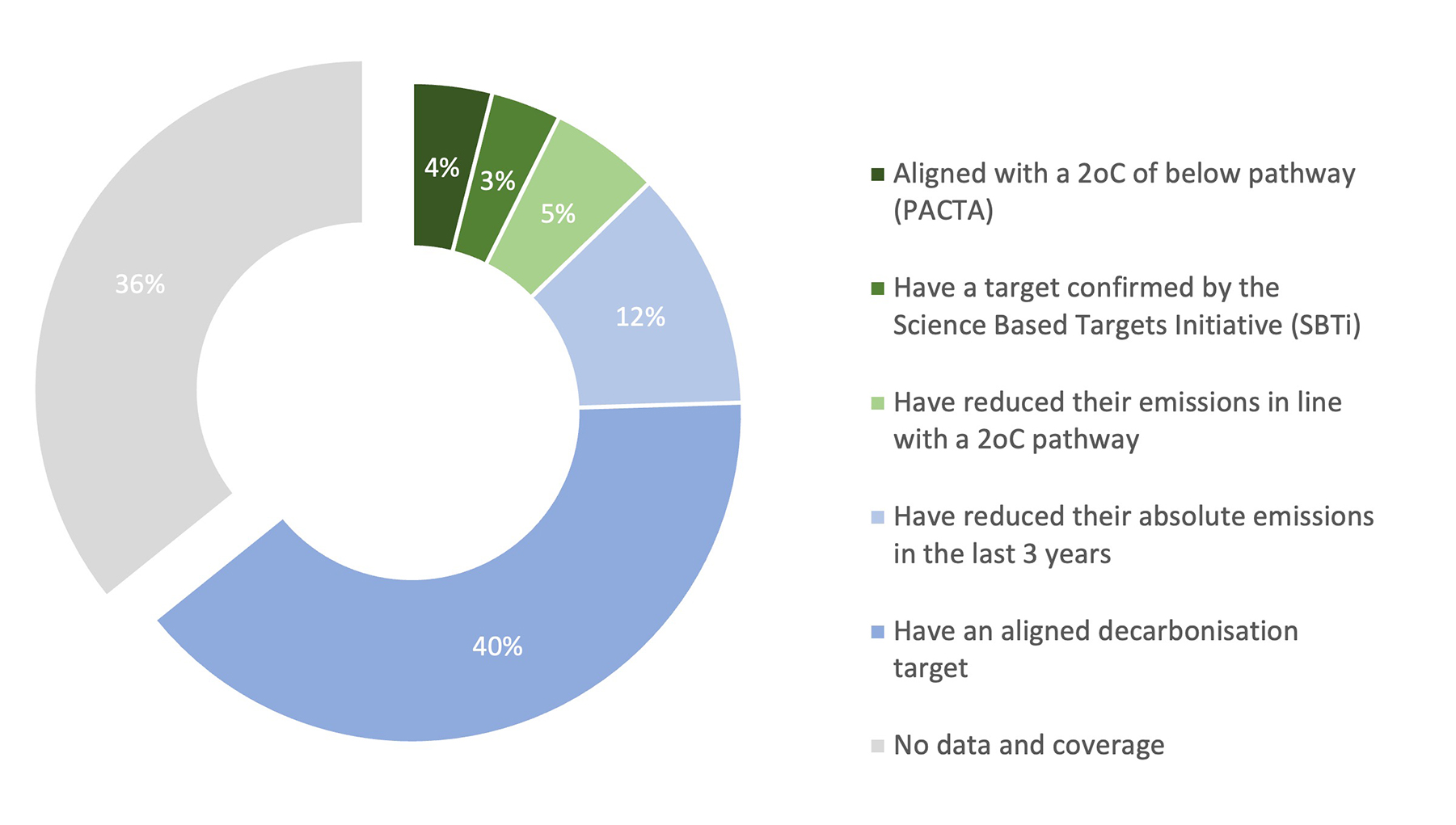

A climate performance evaluation system to score and screen companies from the Latam investible universe is a core requirement. The evaluation combines a PACTA alignment measurement with supplementary climate performance metrics sourced from third-party data providers, including science-based decarbonization targets and absolute emissions reductions.

It can be seen from the results in Exhibit 2 that there was no information found for 40 percent of the total of issuers, which signals the need to continue promoting climate disclosure and reporting from companies, and that the data providers used still have room to widen their coverage in the region. Additionally, the results show that just 5 percent of the investible universe was found to be aligned with a below 2°C scenario according to the PACTA analysis, therefore receiving the highest climate score, with 48 percent having a decarbonization target that is aligned with a sector pathway, followed by 7 percent that can demonstrate recent emissions reductions.

Exhibit 2. Results of the climate performance evaluation for the Latam investable universe

Step 2: Integrate the climate performance evaluation into portfolio construction

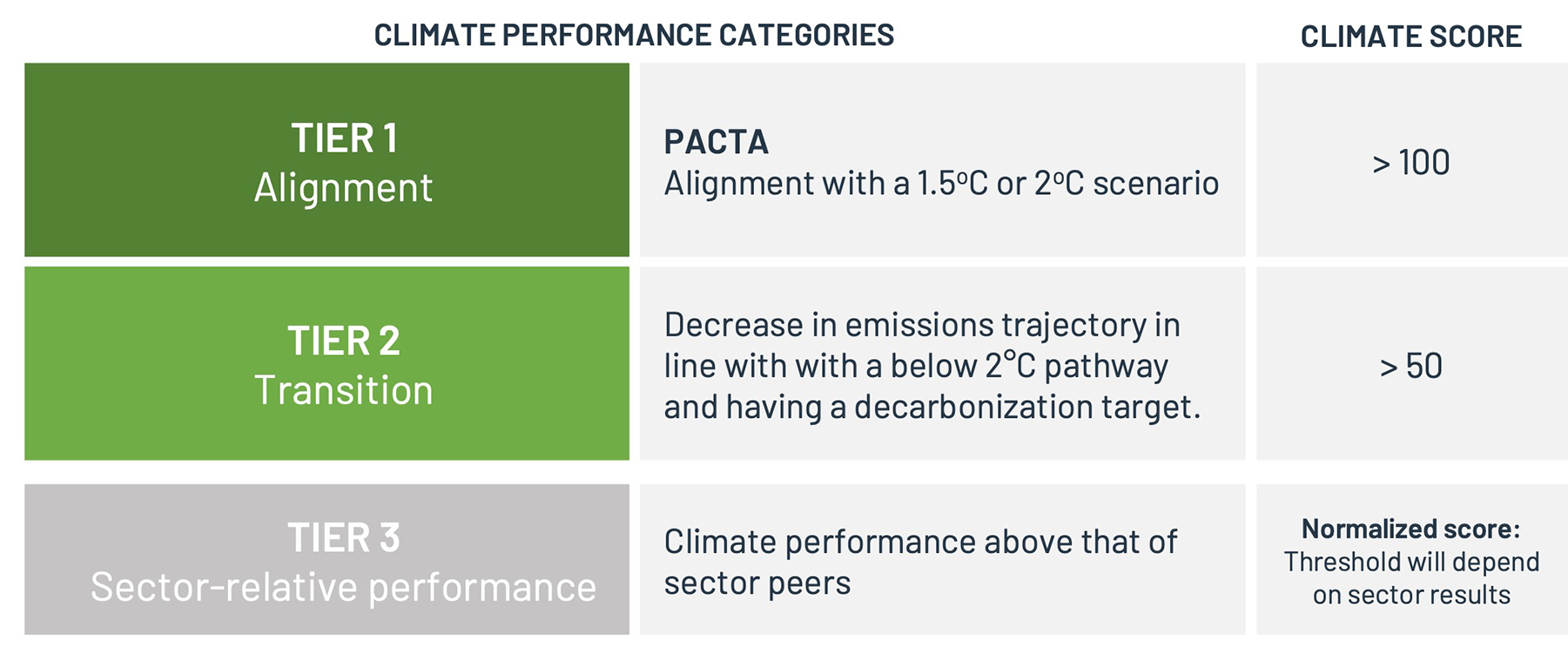

The starting point was to identify the eligible securities according to the issuers’ climate performance score. The companies were categorized into three tiers, to identify those that are aligned with a below 2°C scenario (tier 1), that have ambitious transition plans (tier 2), or that have a better performance relative to their sector peers (tier 3) (see Exhibit 3). The aim is to maximize the portfolio allocation on aligned companies (tier 1), and then use tier 2 and 3 to drive improved performance up the tiers and for diversification purposes, if necessary.

Exhibit 3. Categorization of companies’ climate performance by tiers.

The portfolio construction methodology should seek to integrate the climate performance results alongside financial factors such as issuers’ historic financial performance, risk ratings, market capitalization, and index sector weightings. Two portfolio construction methodologies were developed and the resulting portfolio composition tested:

- For listed equity, a higher weight on the portfolio was given to the issuers with higher climate performance score, and

- For fixed income, the weight of the securities was the result of an optimization process to minimize the portfolio’s volatility relative to a market benchmark.

A back-testing of the financial risk and return performance of the resulting portfolios was carried out to compare the behavior of the funds with the selected Latam benchmarks in terms of alpha (active return), tracking error (relative volatility), and absolute volatility. The overall results were encouraging, indicating that:

- To construct a sufficiently diversified fund a focus is needed on climate transition rather than complete alignment, with the objective being to include companies across sectors making clear steps toward decarbonization.

- It is possible to construct a climate portfolio that is sufficiently diversified and that has a consistent performance compared to the selected market benchmark (MSCI Latam and CEMBI Latam), demonstrated by tracking error ranging from +0.98 percent (fixed income) to +10.5 percent (listed equity) in the period analyzed (2016–2021).

- Both portfolios showed a return above the market benchmarks (2.6 percent for fixed income and 11.8 percent for listed equity) although this could respond to particular market conditions in the period analyzed and might not be caused by the climate alignment of the issuers.

- Greater tier 1 and 2 composition increases volatility and concentration in specific sectors.

- Both resulting portfolios demonstrate a greater climate alignment than the corresponding market benchmark in all technologies that can be evaluated using PACTA.

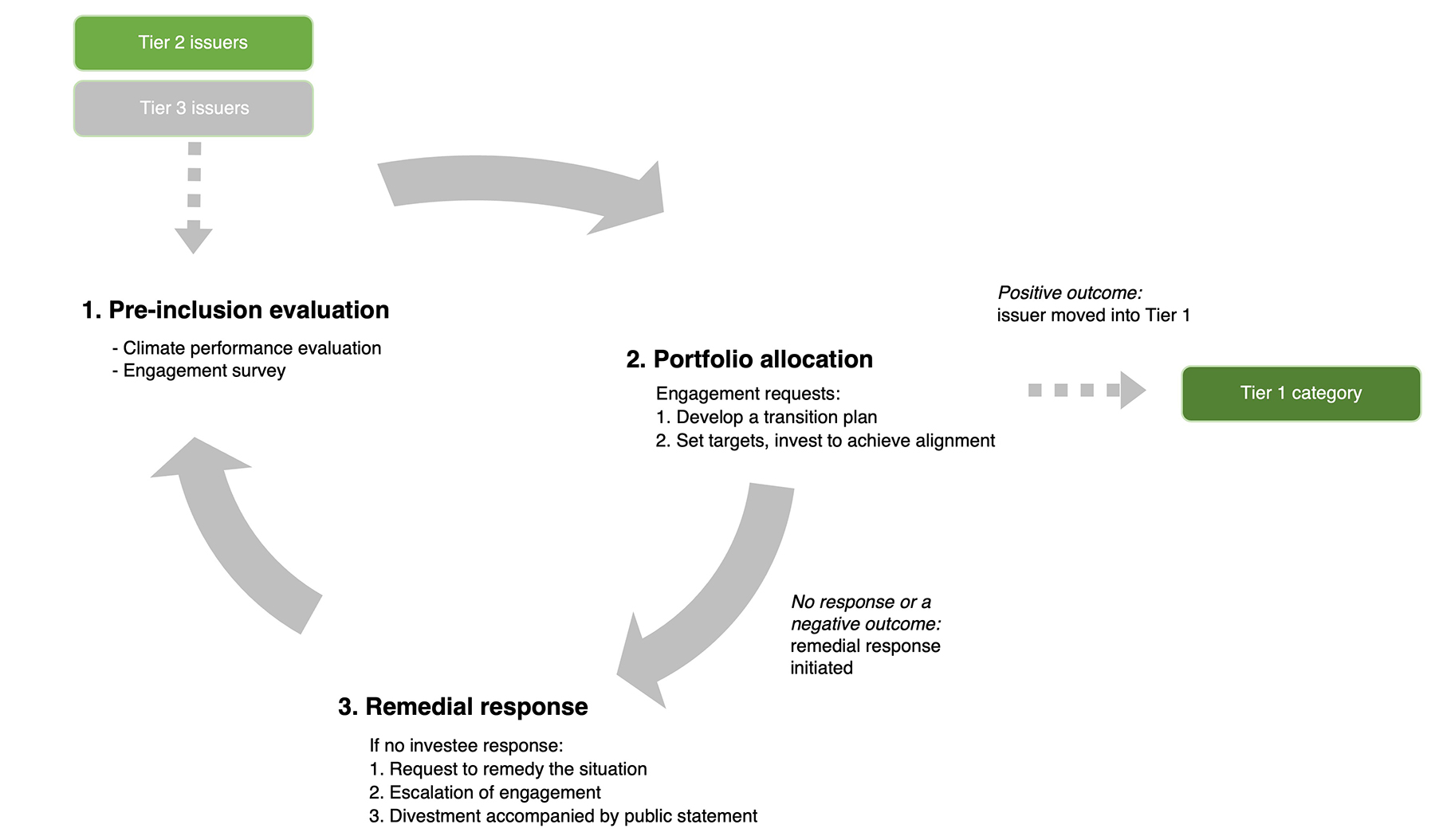

Step 3: Impact management through active investee engagement:

One of the central objectives of the fund design is to contribute to emissions reductions in the real economy. To accomplish this, RMI worked with the 2 Degrees Investing Initiative to identify the most impactful mechanisms available to investors in listed securities. As a result, active ownership to influence climate performance was identified as a key component of the fund strategy.

An active engagement strategy was designed based on the opportunities and constraints within SURA Investment Management and the Latam context. The strategy focuses on the tracking of real-world outcomes and the use of an investors’ levers of influence to request performance improvements, backed up by clear milestones for progress and, if necessary, escalatory measures. The investor would focus engagement resources on those companies initially falling into tiers 2 and 3, to motivate them to changes that might get them into tier 1. The initial evaluation has already been piloted by SURA Investment Management with 28 companies.

Exhibit 4. Core components of the Paris-aligned transition fund engagement strategy

Summary of outcomes

The results of the study show that it is possible to build equity and fixed-income portfolios with issuers that are aligned with below 2oC climate scenario pathways, but that the portfolios would also need to include companies that may only currently have targets to be aligned and, for diversification reasons, that are from sectors that are less significant in terms of their absolute CO2 emissions but that are nonetheless relevant in the Latin American markets and its main indices.

The outcomes from the study represent a first step in the process of integrating climate performance into the standard investment evaluation and portfolio construction process of an asset manager in the Latin American context. Of critical importance to the role of investors in tackling climate change, the study identifies how two key milestones in investor fund design can be achieved:

- The use of company-level forward production plans, reflecting their short-term capital commitments, as the basis for new metrics to objectively evaluate the potential future performance of issuers.

- The integration of climate performance into the portfolio weighting and bond selection steps in portfolio construction, thereby influencing issuer selection and capital allocations.

Moreover, given the need to focus on transition of the economy, a key mechanism for the fund manager to achieve CO2 emissions reductions and therefore impact in the real economy would be active engagement with investee companies and bond issuers to align their climate performance and forward capital commitments with below 2oC decarbonization pathways. In the Latam context, this creates the potential for asset managers to take a more active role in the growth and development of a decarbonized economy, in turn creating more opportunities to invest in companies that in the context of the climate emergency have longer-term economic prospects.

The outcomes from the study are just the start. Going forward RMI and SURA Investment Management will be pushing for them to be put them into practice. The next steps are likely to focus on identifying commercialization opportunities for this type of product and to work with investors to seek broader application of impactful fund design in the market.

This project has been Funded by the International Climate Initiative (IKI) that is supported by the Federal Ministry for Economic Affairs and Climate Action (BMWK), based on a decision of the German Bundestag

Disclaimer: This report reflects only the authors’ views. The German Federal Ministry for Economic Affairs and Climate Action (BMWK) is not responsible for any use that may be made of the information it contains.

Authors

Nicholas Dodd (RMI

Sr. Associate

PACTA

María Ruiz Sierra (Head of Sustainable Investment

SURA Investment Management)

Related Insights

Improving Energy Transition Assessments with Regional Pathways

What Michigan’s Clean Community Financing Ecosystem Can Teach Other US Regions

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.