How Utilities Can Save Customers Billions of Dollars

If utilities modernize the way they select the resources they run each day, they can cut energy prices and carbon emissions.

Over the past three years, energy market prices have been exceptionally volatile. Natural gas prices spiked then tanked at the end of 2019 and wholesale market prices followed. When COVID-19 lockdowns were enacted, energy demand plummeted — so that only the lowest cost resources were really needed to provide energy to consumers — driving prices down even further. Many coal-fired power plants responded by decreasing overall generation.

RMI research looking at the hourly operation of power plants during 2020 shows that there was a huge opportunity for even further reduced reliance on coal, a move that would also have driven $2.5 billion in consumer savings in the first year of the pandemic alone. In fact, since 2012, utilities could have driven $1–$2 billion in savings per year to customers by turning down coal and relying on lower-cost, less polluting resources. To ensure these savings are delivered to customers moving forward, utilities must modernize the way they select the resources they will run each day.

Organized Markets Allow for Transparency

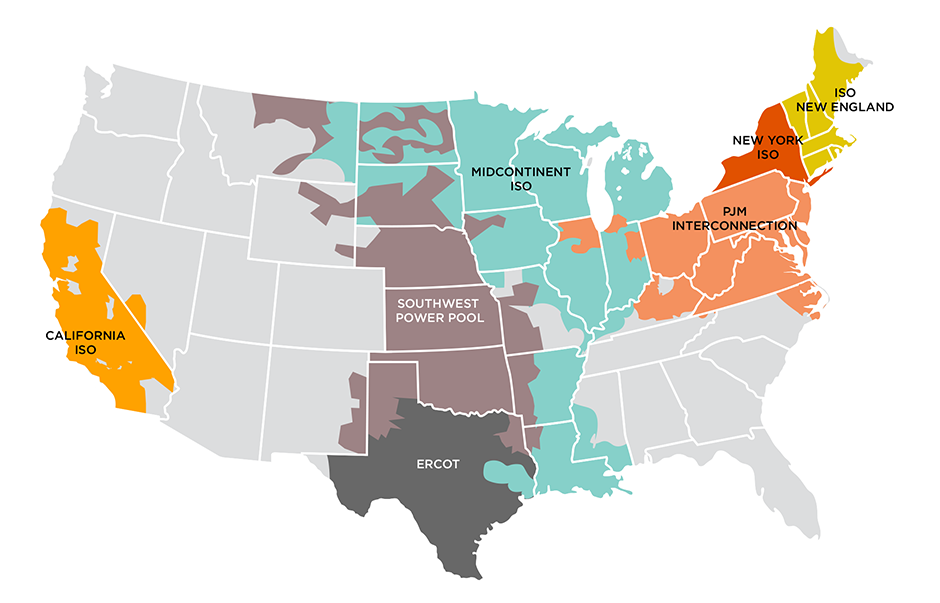

Every day, power plant operators make decisions about which resources will run and which won’t. Operators then commit those resources to operate over the coming days. Some states have independent system operators (ISOs) or regional transmission organizations (RTOs) that coordinate and control the electric grid in that area. In other states, the electric grid is run by individually regulated utilities.

In both ISO/RTO and non-ISO/RTO states, those commitment decisions are supposedly dictated by “merit-order” — a mechanism to ensure that the lowest cost resources get used first. ISO/RTOs have specific protocols that incentivize utilities in their states to commit resources economically, whereas non-ISO/RTO states do not. ISOs and RTOs also publish data in such a way that onlookers can easily determine when or if a utility is economically (or uneconomically) committing coal plants.

The transparency that RTOs offer is why most research on this topic has focused on the Southwest Power Pool (SPP) and Midcontinent Independent System Operator (MISO) — the two regions that are predominantly vertically integrated and also have centralized dispatch through an ISO/RTO. Increasing attention to this issue has resulted in utilities, regulators, and even the market monitors beginning to make slow but tangible improvements in both regions over the past few years.

However, RMI research shows that while there is still room for improvement in SPP and MISO, it is the non-ISO/RTO states that deserve a lot more attention.

Outside Organized Markets, Utility Decision-Making Drives Customer Costs

The full results of RMI’s research on potential savings can be found on RMI’s Utility Transition Hub, an interactive clearinghouse of utility industry data. The economic dispatch hub has the monthly results for every coal plant currently operating. The results can be filtered at the national, regional, state, utility, or plant level and will show when coal was economic to dispatch. Some interesting findings include:

- Since 2012, the US coal fleet incurred aggregated monthly losses of $1-$2 billion per year, with cumulative losses of $14.3 billion over that period. The majority of these losses were borne by rate regulated utilities.

- Since 2012, utilities in the Southeast uneconomically committed coal at a $5.6 billion price tag for customers; those losses account for over one-third of all losses associated with uneconomic commitment. This is unsurprising because utility companies in the southeast haven’t had access to transparent market prices.

- In the ISO/RTO regions, utilities appeared to be making progress in improving commitment decisions until 2020. When the COVID-19 pandemic hit power markets, many previously “economic” coal plants became uneconomic to run. In fact, RMI analysis shows that for the first six months of 2020, the entire US coal fleet lost more money than it made.

Necessary Changes

The largest opportunities for saving are in the West and Southeast, where there isn’t a sufficiently liquid energy market with transparent pricing. Implementing a robust day ahead and real-time energy market with centralized dispatch based on merit order has the potential to reduce energy costs by hundreds of millions of dollars each year. Luckily, price transparency is on the menu for both the West and Southeast with both regions currently considering how wholesale power markets can expand into those regions. However, the Southeast proposal (the Southeast Energy Exchange Market or SEEM) doesn’t include centralized dispatch optimized over multiple balancing authorities, which means that the current proposal won’t be delivering on all the potential benefits of a wholesale market.

In regions that already have liquid energy markets, power plant operators will have to adopt new strategies and approaches for committing resources. Some large coal-fired power plants were once economic to run year-round, but markets have quickly changed in dramatic fashion. Formally “baseload” resources — resources that were economic to turn on and stay on — might now only be economic to run for a few months of the year, if that.

State utility commissions are uniquely positioned to put a stop to practices that cost consumers billions of dollars while providing no benefit. By creating a constructive regulatory environment, commissions can create huge incentives (or disincentives) to encourage utilities to operate their fleet in the most economically efficient way possible. These approaches might include close scrutiny of utility commitment decision-making processes. Further, they could leverage advanced ratemaking processes to create a profit/loss-sharing mechanism that incentivizes better operations.

Utilities can choose to continue to operate coal plants the way they have for decades, but ignoring the realities of an evolving market is a risky endeavor, especially for an industry known for being risk averse. Failure to modernize and optimize how they operate resources will eventually result in scrutiny from regulators who could force the companies’ shareholders to absorb the above-market costs, something utility investors would not be happy about.

It is much better for utilities to be proactive and take action on their own. And they should take advantage of the considerable opportunity to both reduce their emissions and save their customers money.