heavy traffic moving at speed on UK motorway in England at sunset.

How China Can Achieve Carbon-Neutral Transport by 2060

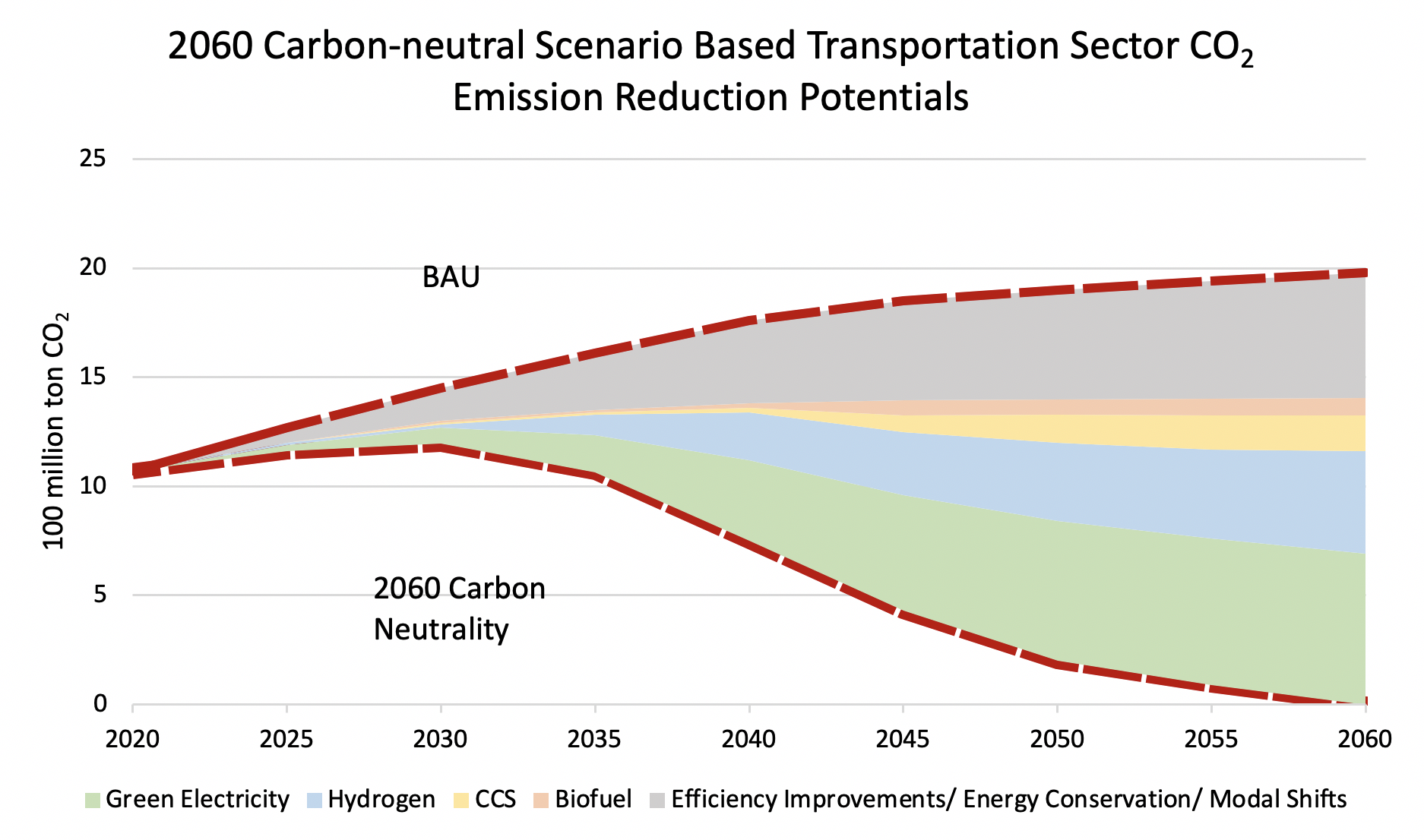

Since 2015, China has been actively implementing its commitment to peak carbon emissions by 2030 in line with its nationally determined contribution under the Paris Agreement. And the recently announced 2060 carbon neutrality goal has set higher requirements for different sectors in terms of carbon reduction approaches. RMI estimates that approximately 30 percent of transportation sector carbon emissions can be reduced through energy conservation, efficiency improvements, and modal shifts. However, achieving full carbon neutrality requires a comprehensive energy transition to replace conventional fossil fuels with clean energy.

Unlike the power, building, and industry sectors, transforming the transportation sector will require clean fuel solutions that can be transported and stored. Therefore, in many cases, these applications will face difficulties directly using clean energy such as wind and solar.

Additionally, the transportation sector comprises multiple modes including rail and short-haul road transport, long-distance ocean shipping and aviation, which all have different needs for clean fuel. A 2060 carbon-neutral scenario, in addition to implementing demand reduction and energy efficiency solutions, will rely on a variety of clean energy forms depending on the characteristics of these different modes (Figure 1).

- For rail and short-haul road transport, electrification with renewable power provides viable pathways. In certain sectors of the trucking market where existing battery technologies are not viable, either advanced chemistry batteries or hydrogen will be needed.

- In sectors where electrification is never likely to be viable, such as long-distance ocean shipping, hydrogen and ammonia can be used to replace the heavy fuel oils that are currently used.

- Finally, for aviation, the most difficult sector to decarbonize, multiple technologies will compete. Sustainable biofuels (which do not increase carbon emissions through altered land use patterns) will have a critical role. However, the biomass to produce sufficient fuel may not exist. Other technologies will need to step in. The possibilities with the greatest potential are planes fueled by hydrogen, ultra-efficient electric aircraft, or synthetic jet fuels created from electricity, water, and CO2.

While it is impossible to know which technology portfolio will ultimately win out, this blog evaluates the characteristics and current situation of the above clean energy sources, and proposes short-, mid-, and long-term goals for carbon neutrality in China’s transportation sector.

Figure 1

Short-Term Goal: Electrification is the Core Task

Transportation electrification is currently the most accessible and cost-effective clean transportation solution with the highest energy conversion rate. Thanks to the rapid development of batteries in the past few years, transportation electrification has expanded from railways to light vehicles, small ships, and even shorter-range airplanes.

Given the anticipated volume of road and rail travel in China, electrified transportation will consume more than 2 trillion kilowatt-hours of electricity in 2060, equivalent to 268 million tons of standard coal and accounting for half of the total energy consumption of the transportation sector. In the short-term, accelerating the electrification of road transportation is the core task to realizing the low-carbon or even zero-carbon transformation of the transportation sector. This requires the coordination between policies, technologies, markets and infrastructure.

Accelerating electrification will require coordination between policy design, technology development, market creation, and implementing infrastructure. Some key policies including setting up ambitious EV promotion targets and raising the emission standards, as well as establishing phase-out schedules to gradually withdraw ICE vehicles from the market. In addition, road privileges policies and subsidies can support electric vehicle (EV) market growth and incentivize technology innovation that will enhance the competitiveness of EVs.

Progress in battery technology and optimization of vehicle technical quality are the key technology drivers, which can be accelerated by setting more stringent technical standards and supplying funds to support industry. Moreover, large-scale deployment of charging infrastructure and efforts to build a robust operation and maintenance service system could effectively drive down the cost of using EVs and lead to rapid EV scale-up.

Mid-Term Goal: Large-Scale Commercial Application of Hydrogen

The energy density of existing batteries is relatively low. With these technologies, about 50 percent of the energy needs of China’s transportation sector cannot be solved by electrification using battery storage. While battery chemistries will certainly improve in the future, just how much is unknown.

Given the large gap between current technologies and what the transportation sector needs, other forms of electricity storage will be needed. Two key forms of storage, hydrogen and ammonia, are likely to play a significant role in China’s transition to zero-carbon transportation. The primary by-product of hydrogen combustion is water, making it one of the cleanest energy sources from an emissions point of view. Currently, most hydrogen in China is produced via industry by-products and coal gasification. Future technology development and cost reductions for water electrolysis will strongly push green hydrogen to become the dominant way to produce carbon-free hydrogen under the scope of carbon neutrality.

Ammonia is another promising future fuel. Ammonia is a more efficient way of carrying hydrogen because it has higher volumetric energy density and is more easily liquified. But it also has its own shortcomings, such as its toxicity. Since the production of ammonia gas is based on hydrogen production and these two gases have similar applications, this blog will put these two gases under the same broad “hydrogen power” category.

Cost is still the main barrier to hydrogen applications in the transportation sector. The current cost of hydrogen vehicles is still comparatively high. In China, the price of a hydrogen fuel cell truck is currently more than five times the price of an internal combustion engine truck of the same size.

In addition, the price of fuel is expensive. Even in the case of hydrogen produced using low-cost fossil fuels, the total cost of hydrogen production, storage, and transportation is much more expensive than fossil fuel, as hydrogen is very hard to liquify and tends to escape from pipelines. These two cost problems will be difficult to solve in the near future. However, in the long run, as hydrogen fuel technology advances and economies of scale play a bigger role, the cost of hydrogen will begin to fall.

In order to achieve the large-scale commercial utilization of hydrogen by around 2040, China needs to accelerate the development and research of related technologies and reduce costs by applying hydrogen technology to achieve maturity and scale. According to the Development Plan for the New Energy Automobile Industry (2021-2035) issued by The General Office of the State Council in November 2020, China is focused on vigorously developing hydrogen fuel cells and hydrogen energy storage and transportation technologies.

In 2016, the Ministry of Industry and Information Technology also put forward the goal of 50,000 hydrogen fuel cell vehicles in use by 2025 and 1 million by 2030 in the Technology Roadmap for Energy Conservation and New Energy Vehicles. More recently, in the 2020 Notice on The Development of Fuel Cell Vehicle Demonstration Application, the Ministry of Finance, Ministry of Industry and Information Technology, Ministry of Science, National Development and Reform Commission, and National Energy Administration together explicitly proposed to support the development of the fuel cell vehicle industry by providing financial awards to city clusters that reach identified standards.

Long-Term Goal: Supplementary Role of Biomass Fuel and Carbon Capture

Despite the rapid development of electrification and the future role of hydrogen in solving higher energy density transportation needs, analysis of production and demand shows that hydrogen and electrification can only contribute about 80 percent of the total transportation sector energy demand in 2060. A large proportion of the remaining 20 percent of demand is from large-scale aviation and long-haul shipping. Due to the requirements for the type and density of energy needed by these two forms of transportation, it is difficult to completely meet these demands with electrification or hydrogen clean energy sources.

Compared to other clean energy sources, biomass fuel is one feasible solution. Biomass fuel can demonstrate similar performance as fossil fuel, with many vehicles able to directly use biomass fuel without modification. The disadvantage of biomass fuel is that its supply is difficult to improve. Biomass fuel primary comes from food crops and food residues as raw materials, and the supply does not meet demand. While secondary biomass fuel technology can use straw and wood from deciduous trees as raw materials, much of the technology is still not available in a commercial sense.

Conservative estimates suggest that biomass fuel could provide China’s transportation sector with the energy equivalent of 30 million tons of standard coal, or 5 percent of the total needed by 2060. It is worth mentioning that power-to-fuel is also a possible future solution for carbon-free aviation and heavy transportation, but due to its slow progress it’s very hard to predict where this technology will be in 40 years. To avoid giving misleading information, this blog will only consider a scenario where this technology will not be ready in 2060.

The carbon-neutral solutions we outlined and emphasized above are majorly focusing on reducing demand, shifting modes, and transitioning remaining energy demand to clean alternatives. However, based on the current outlook, adding these up together will only address 85 percent of total transportation sector energy consumption in 2060.

For the remaining 15 percent—about 480 million tons of coal equivalent (tce) from aviation, 50 million tce from shipping and 300 million tce from road transportation—it is likely to be relatively difficult to achieve a complete clean energy substitution with cost-effective, technically and commercially viable alternatives. Negative emissions technologies, including carbon sinks or carbon capture and storage, will therefore likely serve as cheaper supplementary approaches to achieve full carbon neutrality. It has been calculated that the remaining 15 percent of transportation energy consumption will produce about 250 million tons of CO2 emissions per year in 2060.

Summary

Addressing emissions reductions in the transportation sector will play a key role in China’s overall goal to achieve carbon neutrality by 2060. But despite the huge potential for carbon emissions mitigation, achieving carbon neutrality in the transportation sector is fraught with challenges. To achieve mid- and longer-term objectives, it is necessary to maintain heavy investment and advanced deployment in technology research and development of clean energy alternatives such as hydrogen and biomass.

In addition, China must seize the golden opportunity in the decade ahead by utilizing solutions such as EVs and high-speed railways to quickly achieve peak road transport emissions ahead of schedule and start to decline as soon as possible. The road ahead is long but promising. China has made solid progress in emission control in the transportation sector. With the joint efforts of all industries, a clean, low-carbon, and efficient transportation system is not far away.