Learn how we are working to transform how we use and produce energy.

Growing the Minigrid Market in Sub-Saharan Africa

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Download the report Energy Within Reach: Growing the Minigrid Market in sub-Saharan Africa here.

Businesses lining the rusty red dirt road of the commercial thoroughfare of Segbwema in Sierra Leone (pronounced shuh-BOY-ma) sell cold Coca-Cola and local ginger ale, their dry goods in the front of shops lit by pairs of large compact fluorescent bulbs. However, there is no grid to provide electricity here. Even in the neighboring city 40 kilometers away where the grid does reach, it provides only six hours of intermittent electricity during the six-month dry season.

Until recently, these businesses were powered at a high cost by diesel generators, when they were powered at all. But for the past several months some commercial businesses have been receiving power from a local minigrid, an isolated distribution network powered by solar and battery storage. And it’s not just local businesses that are receiving power; residential customers are connecting to the minigrid, too, and hundreds more will connect over the next few years. This approach not only provides energy access, but also drives economic growth in rural areas, and is being replicated across sub-Saharan Africa and southern Asia.

Enthusiasm for the growth of minigrids in Africa and South Asia is shared by young companies looking to provide the hardware, software, and services to build them. Commercial investors and energy majors are likewise eyeing the opportunity. Development partners like the UK’s Department for International Development and Germany’s GIZ are committing hundreds of millions of dollars to explore the potential for minigrids and support their growth, and groups like The Rockefeller Foundation are investing time and money with the goal of speeding economic development. Most promisingly, governments in countries as varied as Tanzania, Rwanda, and Sierra Leone are beginning to think about how the off-grid energy provided by minigrids could help them achieve energy access and economic growth targets.

However, minigrid market share is currently extremely small, even in leading markets like Kenya, and its growth is slow. To live up to the promise attributed to them by hopeful companies, enthusiastic development partners, and anxious governments, minigrids must demonstrate they can compete on cost with other energy-access alternatives with a commercially viable business model. RMI’s recently released report, Energy Within Reach: Growing the Minigrid Market in Sub-Saharan Africa, describes the economics behind minigrids and compares them to the competing or complementary alternatives of solar home systems and grid extension. Establishing the commercial viability of minigrids is the first step toward attracting the significant concessional and commercial finance necessary to have a real impact on energy access and economic growth in Africa.

MINIGRIDS VS. OTHER ENERGY ACCESS ALTERNATIVES

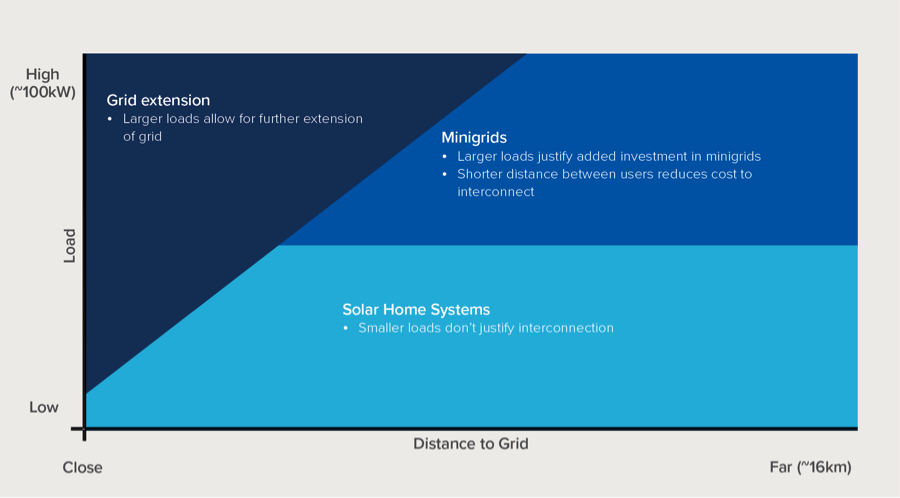

We found that the cost competitiveness of minigrids versus alternatives depends on two key factors: the load size served and the distance of the minigrid site from the existing grid.

THE LEAST-COST OPTION FOR ENERGY ACCESS DEPENDING ON LOAD SIZE AND DISTANCE FROM THE EXISTING GRID

As shown in the figure above, the cost of extending the grid increases the farther a site is from the existing grid. The two primary off-grid energy access options—solar home systems and minigrids—can serve customers who are too far from the existing grid or in places where the grid is not reliable enough for customer needs. Solar home systems are better suited to serve smaller load sizes (typically less than 5 kWh/month). Slightly larger load sizes allow the cost of distribution lines to be affordably amortized. Other factors, such as using more of the available solar generation and battery storage capacity by balancing evening residential use with daytime commercial use, can also improve minigrid economics.

REDUCING MINIGRID COSTS

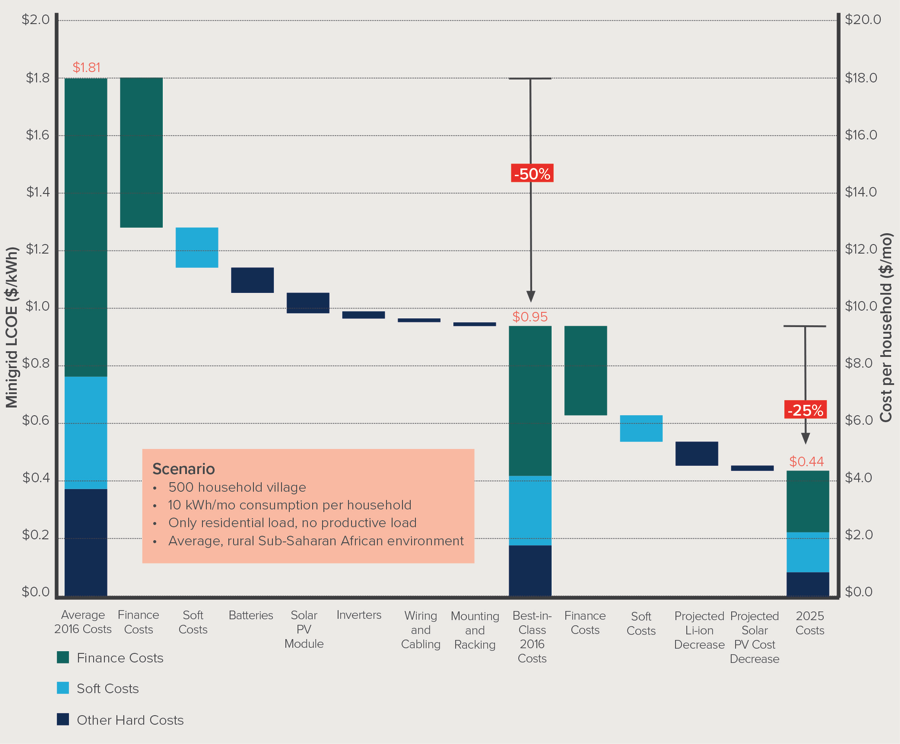

The difference between average minigrid costs in Africa and best-in-class costs is enormous. Average levelized cost of electricity (LCOE) for solar-diesel-battery minigrids could be as high as $1.80/kWh, while best-in-class costs for the same technology are around $0.95/kWh. This gap can be attributed to poor site selection, improper system sizing, a lack of competitive tenders, and the overwhelming reliance on donor-supplied grant financing. If the minigrid market is going to grow more quickly, these costs must be brought down.

Solar and storage costs, which comprise nearly 30 percent of costs for solar-battery-diesel systems, are projected to decrease by half in the next decade. Other hard costs could be brought down by emphasizing increased asset utilization through energy efficiency and load management. Industry consolidation could also drive down hardware costs. Site clustering, standardized customer acquisition processes, and aggregated software could help reduce minigrid soft costs in Africa.

As shown in the figure below, the cost of capital available to minigrid companies in Africa (15 percent to 20 percent) is an additional impediment to growth, and a tremendous cost burden for those accessing market-rate debt. Development partners could help coordinate project finance for minigrids, along with patient equity and venture debt, to both reduce finance costs and free up company capital to accelerate growth.

AVERAGE INSTALLED SOLAR-DIESEL-BATTERY MINIGRID COSTS CAN BE REDUCED BY 75 PERCENT

To realize the potential for minigrids to drive economic growth and energy access in Africa, the following actions are needed from the private sector, development partners, and governments:

- Coordinated trials to test the commercial viability and scalability of minigrids are needed. Carefully planned minigrid trials can provide valuable data regarding cost, pricing structure, system specifications, and management of collection and theft.

- The private sector should focus on continued cost-reduction and service improvements. Opportunities include better site selection, integrated hardware and software packages, modular capacity, specialized local project development and management expertise, aggregated finance, and a focus on end-use service instead of power consumption.

- Development partners should play a coordinating and financing role for the early stage minigrid market. By facilitating discussion between governments and the private sector, and providing carefully placed technical assistance and advocacy for a clear set of minigrid-enabling policies, they can support governments with ambitious electrification targets that prioritize off-grid growth.

- Governments need to provide predictable enabling environments for minigrids if they are to achieve their ambitious energy access targets. Governments can reduce regulatory risk for companies and their investors with clear, comprehensive off-grid energy plans; streamlined import procedures; dependable incentives for renewables and energy efficient appliances; and education/awareness campaigns that communicate to their citizens the role of off-grid products and minigrids in particular.

Providing energy access to the hundreds of millions of unelectrified households in sub-Saharan Africa quickly, cost-effectively, and sustainably is a daunting challenge. Minigrids will play a key role in addressing this challenge, particularly for the isolated commercial and industrial customers, like the shopkeepers and grain mill operators in Segbwema, that are driving real economic growth.

Download the report Energy Within Reach: Growing the Minigrid Market in sub-Saharan Africa here.

Photo credit: Eric Wanless

Authors

Kelly Carlin

ManagerRelated Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.