Learn how we are working to transform how we use and produce energy.

The Fed’s Climate Tests Are Missing the Next Big Failure

By focusing only on large banks, the Fed is overlooking the greater climate risks facing smaller institutions.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Following signs of severe financial distress at SVB and Signature Bank last week, financial regulators stepped in to take control of these banks and protect depositors by using authority designed to protect the banking system from systemic risk. In doing so, the US Federal Reserve determined that SVB and Signature Bank are systemically important financial institutions (SIFIs) because they are so large and interconnected that their failure could have a significant impact on the broader financial system. The move of designating a mid-sized, state-chartered bank as a systemic threat to the stability of the broader financial system — in just 48 hours — demonstrates that regulators don’t always know where the next threat to financial stability will come from.

In the wake of the 2008 financial crisis, the Dodd-Frank Act established a tiered bank regulatory system which requires enhanced supervision and regulation for the largest banks (SIFIs), while providing less oversight for smaller and mid-sized banks. This oversight was further relaxed in 2018 for many regional banks like SVB. The driving assumption of the current regulatory framework is that only the largest banks are interconnected enough to threaten the stability of the overall financial system. In the wake of the actions regulators took for SVB and Signature Bank, that assumption is clearly wrong.

Let’s not make the same mistake again

That same flawed assumption underlies the approach the Fed is taking to understand the threat of climate risks to the financial system. In January, the Fed announced that six of the nation’s largest banks will participate in a much-anticipated pilot climate scenario analysis exercise designed to assess their climate-risk management practices.

This exercise is primarily focused on banks’ exposure to climate-related physical risk in their residential and commercial real estate loan portfolios and climate-related transition risk in their commercial real estate portfolios. The reason that the Fed is focusing on real estate is clear: the real estate sector is highly exposed to physical and transition risk. Over the past five years, insured property losses due to natural catastrophe globally averaged about $100 billion, with 71 percent of those losses occurring in North America. If you included uninsured losses that amount increases to $270 billion.

From a transition risk perspective, the real estate sector is responsible for almost a quarter of all US GHG emissions. Accordingly, there is no credible transition pathway or scenario that can be achieved without reducing the carbon generated by the building stock. The cost of making these changes, or the failure to do so, creates the risk of a market shock to values, demand, or both.

But we need to look beyond the largest banks

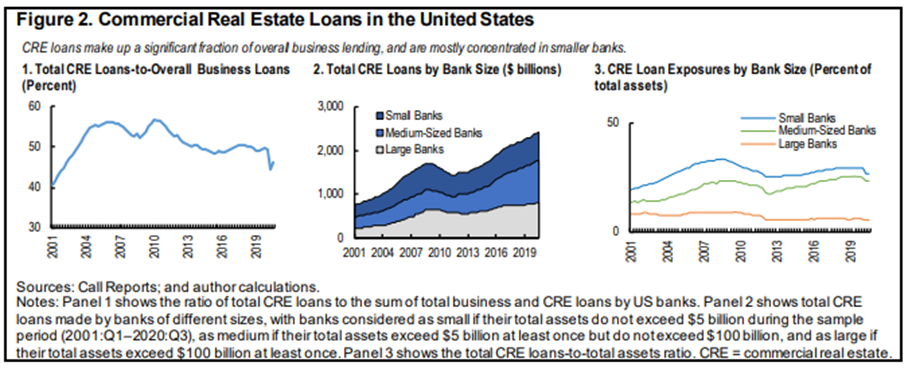

While real estate makes up half of all banks’ business loan exposure, as the next charts show, more than half of that exposure is held at small and medium sized banks. Further, that exposure represents a significantly greater percentage of small- and medium-sized banks’ overall assets. This point was made clear in a 2020 report from the Commodity Futures Trading Commission which stated that “ climate-related shocks that affect commercial property in a particular region can take a much heavier toll on small institutions, which tend to be regional and community banks, than on banks with nationwide or global balance sheets.”

Source: International Monetary Fund (IMF).

When we look at the GHG emissions coming from real estate, we again see that small and medium sized entities have an outsized impact.

Working with data from the National Renewable Energy Lab’s (NREL) ComStock Analysis Tool, Energy Information Administration’s (EIA) CBEC and REC surveys, and Environmental Protection Agency’s (EPA) Inventory of Greenhouse Gas Emissions, RMI has developed a model that allocates the greenhouse gas emissions generated by the entire U.S. building sector by building type, size and state. The model also determines whether the carbon is a result of on-site fossil fuel usage or of electricity used at the property. The chart below shows that allocation for the commercial real estate sector.

Just like the biggest banks don’t necessarily have the most real estate exposure, the properties financed by the big banks don’t necessarily generate the most greenhouse gas emissions. Some of the largest sources of carbon are medium-sized retail (like strip malls), small multifamily properties, and small restaurants — all property segments much more likely to be financed by smaller regional banks, as opposed to large national banks.

Taken together, it is clear that the Fed’s pilot is likely to miss significant concentrations of climate related risk.

While the Fed should be applauded for recognizing the risk climate change can pose to the banking system, at least as it applies to real estate financing, the recent impact of the SVB collapse shows that the largest banks may not be the right place to start.

The Fed needs to be aware that the results of the pilot will be highly biased based on the composition of the portfolios it examines and may be skewed to show that the climate risk exposures faced by banks are either well-managed or non-significant. In reality, neither is true. Smaller and mid-sized banks are likely to be more underprepared and poorly equipped to deal with climate risk, and the significance of the threat (as illustrated by SVB) shows that we need to take the risks coming from these entities much more seriously.

Authors

Drew Ades

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.