An electric car is plugged into a charging station as a glowing sunset sky reflects off its sleek metallic surface, symbolizing modern sustainability.

Electric Vehicles Are on the Road to Mass Adoption

EV purchases are rising, costs are decreasing, and battery technology is improving.

Adoption of electric vehicles (EVs) is gaining serious momentum around the world. Multiple countries, including the United States, have already passed a passenger EV tipping point— when sales reach critical mass, after which adoption accelerates. In the United States, owning a light-duty EV is now cheaper than owning a gas-powered car over a vehicle’s lifespan. This lower cost of ownership is thanks to ongoing savings from using electricity rather than fuel, less maintenance, and other recurring benefits.

The number of electric medium- and heavy-duty (MHD) trucks also continues to grow globally. MHD trucks’ purchase prices are trending toward parity with diesel, with some segments reaching parity as early as 2028. Given fleets are incredibly price sensitive, cost parity is the determining factor in their switch to electric.

In addition, battery recycling technology is improving. By 2040 we estimate that enough battery minerals will be in circulation to significantly reduce or possibly eliminate the need for additional mining — supporting electric transportation into perpetuity. This is in sharp contrast to the ongoing need to extract oil to fuel gas-powered vehicles.

EV adoption continues to grow in multiple countries, passing tipping points.

More than 17 million electric cars were sold worldwide in 2024, 20 percent of all new cars purchased. Most of those cars (11 million) were sold in China, maintaining its multiyear lead as the largest EV market.

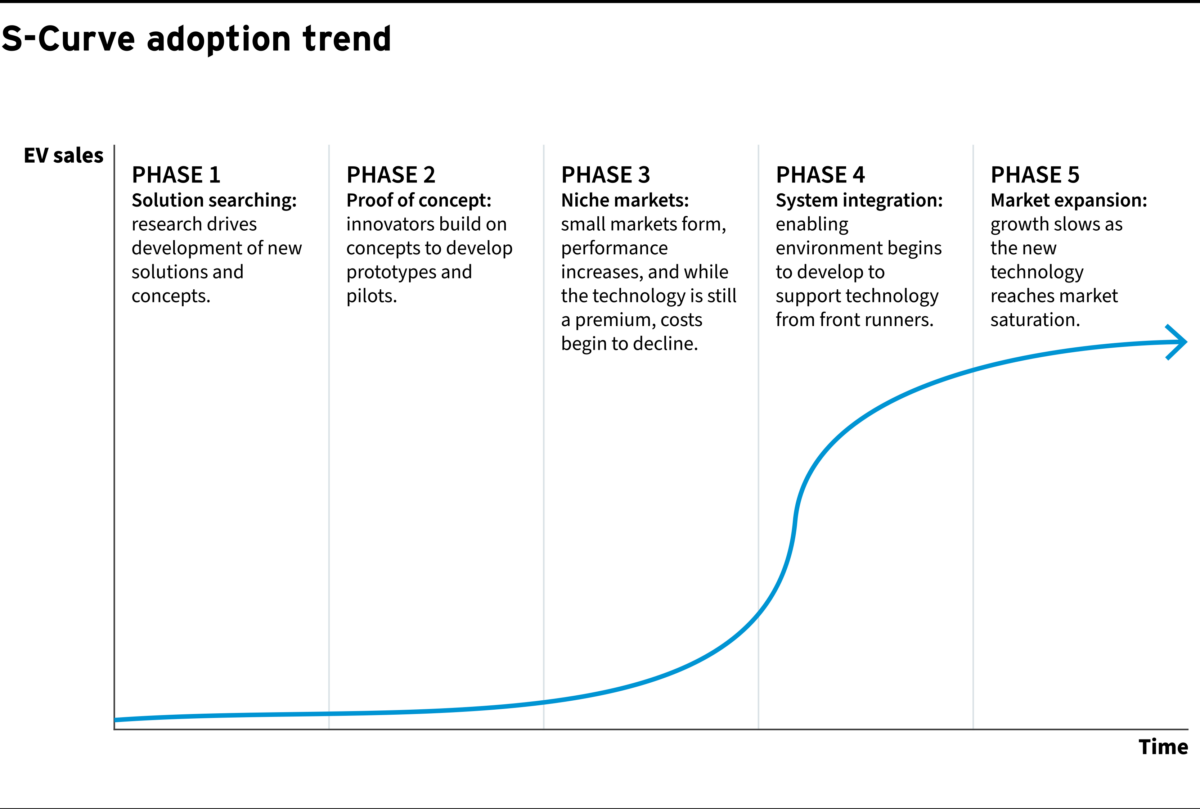

EV adoption is following an S-curve trajectory in many countries. Adoption of other innovative technologies like wind and solar have also followed S-curve trajectories — driven by factors that make technology adoption easier over time, such as learning curves, economies of scale, technology reinforcement, and social diffusion. One of the defining aspects of S-curves is that they accelerate — as markets reach certain thresholds, adoption rates typically increase. Exhibit 1 shows a high-level S-curve trend, and the different phases of the curve.

Exhibit 1

Exhibit 2 below shows when various countries have and will cross specific adoption thresholds. Presently, China is the only country in Exhibit 2 that is transitioning into the late majority adoption phase, but most major markets have already crossed the tipping point for EV adoption acceleration (roughly 1–5 percent). The United States passed 1 percent adoption in 2017, 5 percent in 2022, and 10 percent in 2023.

Exhibit 2

Although the United States has passed critical adoption tipping points, it only saw 10 percent year-on-year growth in 2024 — in stark contrast to the 40 percent seen in 2023. As more and more countries continue along their EV S-curve, the United States risks being left behind if increased adoption slows. The United States needs to seize the narrowing window to establish itself as a leader in EV technology development, carry on supporting EV adoption, and realize cleaner air, household cost savings, and the other compound benefits of EVs.

The total cost of ownership is lower for an EV than for a gas-powered vehicle in the United States

Battery prices, economies of scale, and increasing market competition have made electric cars more affordable. While, in some countries EVs still have higher up-front costs than combustion engine vehicles, they typically have lower operating costs. This is due to EVs requiring less maintenance, and the cost of electricity for charging being significantly lower than the cost of fuel. In the United States, the gap in operating expenses is so significant that it more than offsets the higher up-front purchase price of an EV over time.

Exhibit 3 shows the annual savings the average household would see from driving an EV instead of an internal combustion engine car in the United States. This is an important metric to track because consumers are responsive to opportunities for cost savings. The reduction in cost savings beginning in 2026 reflects removal of the federal EV tax credit, per recent legislative changes which go into effect September 30, 2025. However, Exhibit 3 shows that the reduced operating costs for an EV over time still present overall savings for EV drivers compared to drivers of combustion engine vehicles.

Additionally, it remains to be seen how state, cities, and other governments and private entities may respond with their own programs to counterbalance the removal of the federal tax credit, and how any such programs might impact total cost of ownership calculations.

Some states already have their own incentive programs. For example:

- New York State’s Drive Clean Rebate offers up to $2,000 off the purchase or lease of an EV.

- Connecticut’s Hydrogen and Electric Automobile Purchase Rebate (CHEAPR) program offers incentives up to $7,500 plus additional supplemental rebates with income qualifications.

- The Massachusetts Offers Rebates for Electric Vehicles (MOR-EV) program offers incentives of $3,500–$6,000 for electric vehicles, depending on income and ability to trade in a qualifying vehicle.

Exhibit 3

The 2025 annual savings shown in Exhibit 3 translate to real savings for US families, as shown in Exhibit 4.

Exhibit 4

Note: The TCO cost savings in this graphic reflect an up-front vehicle cost that is reduced by the federal EV tax credit of $7,500, which is available until September 30, 2025.

Electric medium- and heavy-duty trucks are approaching cost parity with diesel.

Trucking has long been considered one of the harder-to-transition sectors of the economy. Truck fleets compete on price and so are very sensitive to cost increases. Electric MHD trucks today are more expensive than their diesel counterparts, in large part because MHD truck batteries make up much of the overall vehicle price. Historically, MHD batteries have been more expensive per kilowatt than the batteries in light-duty vehicles, largely due to more significant design and testing needs, and reduced economies of scale.

But the market for electric trucks is accelerating globally and will soon erase the cost premium for electric trucks. The number of electric truck models is growing in all major markets — there are now more than 100 electric MHD truck models available in the United States, China, and Europe. As the market expands, manufacturing efficiencies will drive down costs and truck battery prices are expected to converge with general vehicle battery costs in the next five years. Battery price drops will hasten the arrival of price parity for electric trucks. This point of price parity represents a fundamental shift in how fleets will think about decarbonization.

Exhibit 5

What this EV adoption means for mining battery minerals.

In one year, the world extracts 40 percent more oil than the total weight of all the ore needed to electrify the world’s entire transportation system.

Currently both EVs and gas-powered vehicles require mined and extracted resources — EVs require minerals for batteries and gas-powered vehicles require gasoline derived from oil. Gas-powered vehicles require fuel on a regular basis, whereas making a vehicle battery only requires resources to be mined one time.

Lithium batteries are already largely recycled and even today more than 90 percent of lithium and 95 percent of nickel and cobalt are recovered from recycled batteries. As battery recycling, which has the potential to reduce both costs and environmental impacts, continues to improve and costs come down, there will be even less need for newly mined battery minerals. Mineral recovery rates are improving, and recycled minerals are meeting or exceeding standards for virgin minerals. The electrification of the global transportation system will require a total of approximately 125 million tons of battery minerals by 2040. After reaching this equilibrium, robust battery recycling can significantly reduce the amount of newly mined materials required. If we can combine that with better batteries, more efficient material use, and more efficient transportation systems, there could be enough battery minerals in circulation to support the battery supply chain in perpetuity.

Exhibit 6

Electrification is happening all around the world, and advances in the battery recycling industry have the potential to reduce both costs and environmental impacts. This is a critical moment for the United States to decide whether it will compete on the global stage or be locked into obsolete technology with non-renewable fuel sources. Fortunately, there are still opportunities for the United States to embrace vehicle electrification. The total cost of owning EVs is decreasing, and electric trucks are anticipated to reach cost parity with gas- and diesel-fueled trucks in the next few years. Both dynamics should support increased adoption.