ideal for websites and magazines layouts

Clean Energy Is Canceling Gas Plants

While COVID-19 has disrupted many aspects of the economy and daily life in 2020, the trend toward clean electricity is still going strong. Renewable energy and storage technology costs continue to fall, with expanding adoption by utilities and other investors, while new gas-fired power plants face ever-stronger financial headwinds.

Data from competitive markets is beginning to reflect this emerging reality. As of mid-2020, power plant projects planned for construction in two of the most competitive US electricity markets (ERCOT in Texas and PJM in the Northeast) have shown a remarkable shift from gas to clean energy. Gas generation is now attracting only a small fraction of investor interest compared to clean energy and will soon likely see its market share decline accordingly.

While this evidence from leading markets is positive news for energy customers and the climate, this success needs to be replicated across the country to bring the electricity sector’s emissions trajectory in line with pathways to avoid the worst effects of climate change. Other wholesale markets and vertically-integrated utilities outside of wholesale markets have a clear opportunity to further open up their resource investment process and leverage the benefits of innovation and cost reductions in clean energy.

Investors are Increasingly Prioritizing Clean Energy Over Gas

Interconnection queues—which track new generation projects proposed to be added to regional grids—provide a leading indicator of market trends for new power plants. Not all projects in these queues are ultimately built, but the mix of resources in the queue represents which investments the market is prioritizing.

Over the past two years, interconnection queue data from PJM and ERCOT have shown a drastic shift away from new gas and a steep rise in renewable energy projects. In these two regions, investors finance projects based on expected returns in the competitive market—not based on expectations of cost recovery allowed by regulators of monopoly, vertically-integrated utilities. In other words, this trend represents the shifts in internal risk and reward calculus among investors in highly competitive markets, and reflects a market-based, consensus view of the underlying economic value of different power sources.

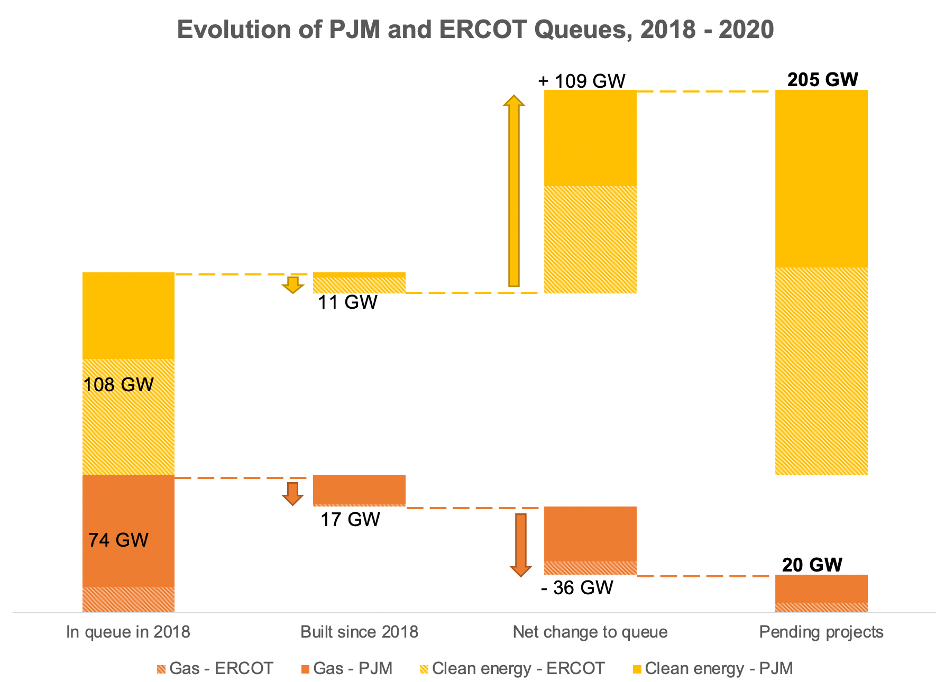

As shown in Exhibit 1, this emerging investor view on the bankability of gas versus clean energy couldn’t be clearer. In 2018, there was already 45 percent more clean energy than gas capacity in the queues of ERCOT and PJM. Since then, slightly more gas capacity has come online than wind, solar, and storage; but while the clean energy queue has more than doubled, the gas queue has been cut in half, with over $30 billion worth of gas projects canceled or otherwise abandoned. Currently, there is over 10 times the capacity of wind, solar, and storage projects slated for construction in ERCOT and PJM than new gas projects.

What Is Driving this Shift?

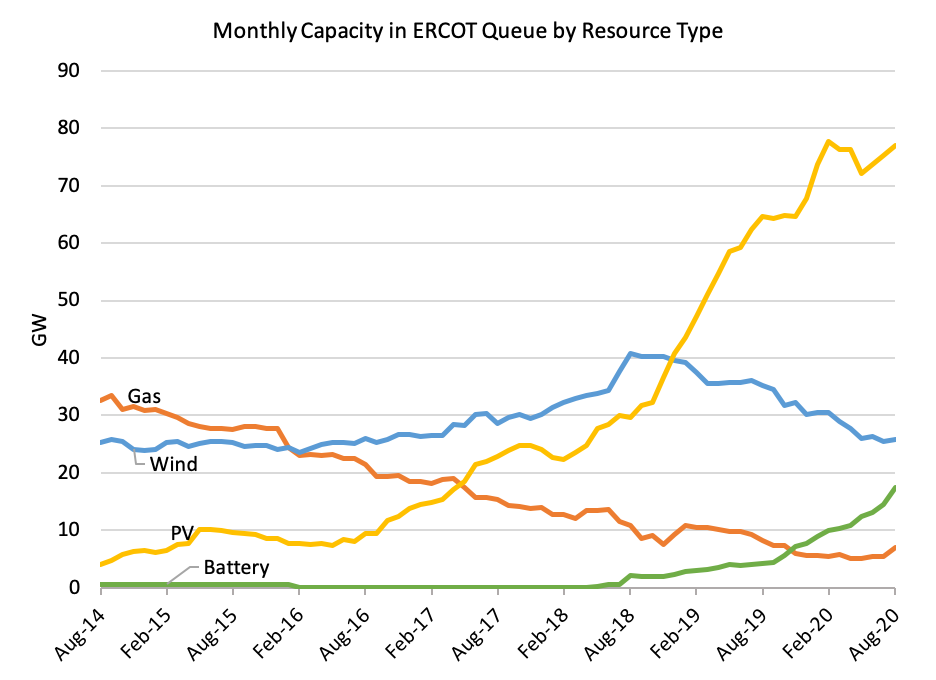

Though COVID-19 may be contributing to some recent decline in planned gas additions, it’s not the only driver. The trend has been building for years and investors more broadly are now waking up to the implications. For example, just five years ago in ERCOT, the interconnection queue contained an even split between proposed gas and renewables generation capacity. However, gas capacity in the queue started falling steadily in 2015, well before the COVID-19 pandemic and associated economic downturn (Exhibit 2). Meanwhile, renewable energy and storage projects in the queue have continued to grow even during the pandemic.

In ERCOT and PJM markets investors prioritize projects based on competitive risk and return profiles as opposed to regulator-allowed cost recovery. Therefore, it is likely that a more fundamental driver is at play: raw economics, driven by the continually falling costs of clean energy and the associated risks of investment in new gas-fired capacity.

The Growing Business Case for Clean Energy

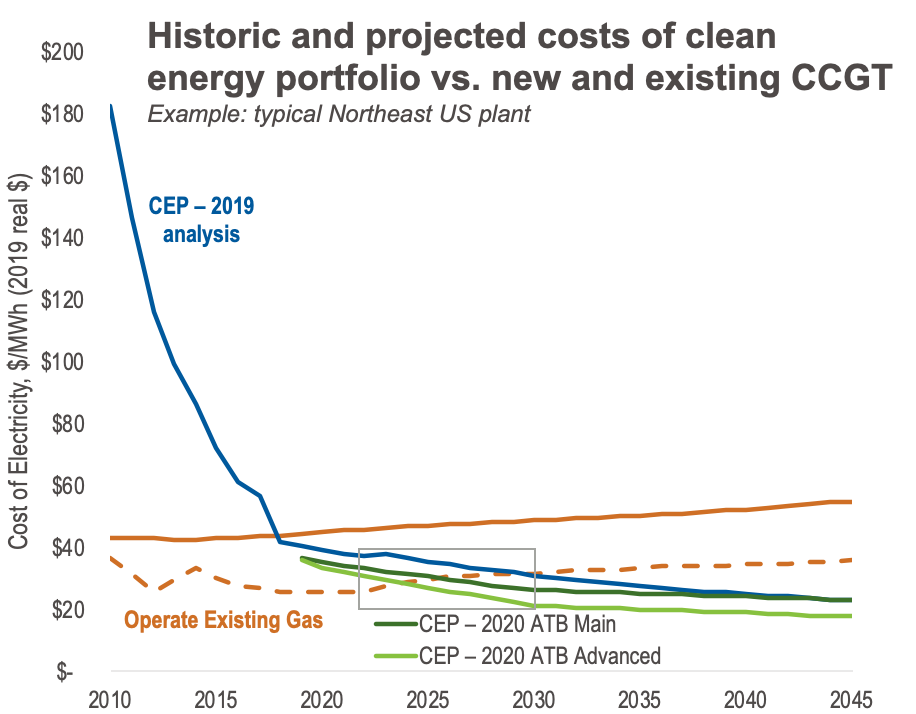

In 2019, RMI published The Growing Market for Clean Energy Portfolios, which found that clean energy portfolios (CEPs)—combinations of renewables, storage, and demand-side management—are lower-cost than the vast majority of capacity in planned gas-fired power plants. Specifically, the study showed that CEPs are cheaper than 95 percent of proposed combined-cycle capacity and 60 percent of combustion turbine capacity.

In addition, the study found that by 2035, the cost of building a new CEP will be less than the cost of operating 90 percent of proposed combined-cycle capacity. This creates a risk that new gas-fired power plants may face stranded cost risks well before the end of their useful lives.

And the benchmark costs of clean energy have fallen meaningfully in the past year. We have updated our analysis, using new data on renewable energy and storage costs from the US Department of Energy-sponsored 2020 Annual Technology Baseline (ATB) and an improved representation of how storage can contribute to meeting peak demand. We have found that CEPs are now even more competitive with new gas plants.

Importantly, this updated analysis shows that most proposed gas plants that do get built will face stranded cost risks within 10 years of construction. If cost and efficiency improvements for clean energy continue at closer to their historical rates (e.g., as shown in the 2020 ATB’s Advanced scenario), 90 percent of planned combined-cycle capacity will face stranded cost risk by 2026. For many gas-fired plants, this could mean that they are already stranded assets the day they enter service.

Cost-Effective Decarbonization through Competition

The evidence is clear: clean energy wins when allowed to compete with gas on a level playing field. But a number of monopoly, vertically-integrated utilities still lag in their approach to competitive procurement, and routinely prioritize adding gas to their systems. These decisions threaten to lock in costs, carbon emissions, or both, increasing the economic burden and slowing the pace of decarbonization necessary to mitigate the worst effects of climate change.

But even without comprehensive climate policy at the federal or even state level, there remains a tried-and-true method to unlock the benefits of clean energy innovation for all utility customers: open competition between energy resources to provide the highest value at the least cost. Fair competition between resources in restructured markets, and emerging best practices around all-source procurement in monopoly markets, can allow clean energy to compete to its fullest potential.

Competitive markets have shown that it’s possible to deliver cost and carbon savings with clean energy portfolios; it’s well past time for the rest of the country to follow.