Learn how we are working to transform how we use and produce energy.

We Read a 130-Page Report on Climate Regulation So You Don’t Have To

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

In October 2021, the Financial Stability Oversight Council (FSOC)—an oversight body for federal financial regulators—chimed in on the climate conversation by way of a dense, 133-page report. The FSOC Report on Climate-Related Financial Risks examines how US regulators are already addressing climate-related financial risks, discusses ongoing challenges in assessing those risks, and offers more than 30 recommendations for regulators to improve the resilience of the US financial system to climate change.

While the highly anticipated report has been critiqued as a missed opportunity that didn’t go far enough, the effort, led by US Secretary of the Treasury Janet Yellen, laid down a marker on an issue of critical importance. Because FSOC comprises leadership from all major federal financial agencies, the report essentially documents the US regulatory brain trust speaking among themselves about climate change. Approved via (nearly unanimous) group consensus, the report also reflects the floor of ambition across these agencies—and the floor has been raised considerably.

Given the report’s significance—and because it’s long, dense, and chock-full of jargon—staff at RMI’s Center for Climate-Aligned Finance have broken it down into key takeaways. Those takeaways are outlined here, along with reflections on what comes next.

FSOC Acknowledges Climate Change as a Systemic Risk

Why it matters: regulators understand that the scope and magnitude of climate-related financial risks go beyond individual assets or a single firm’s financial portfolio.

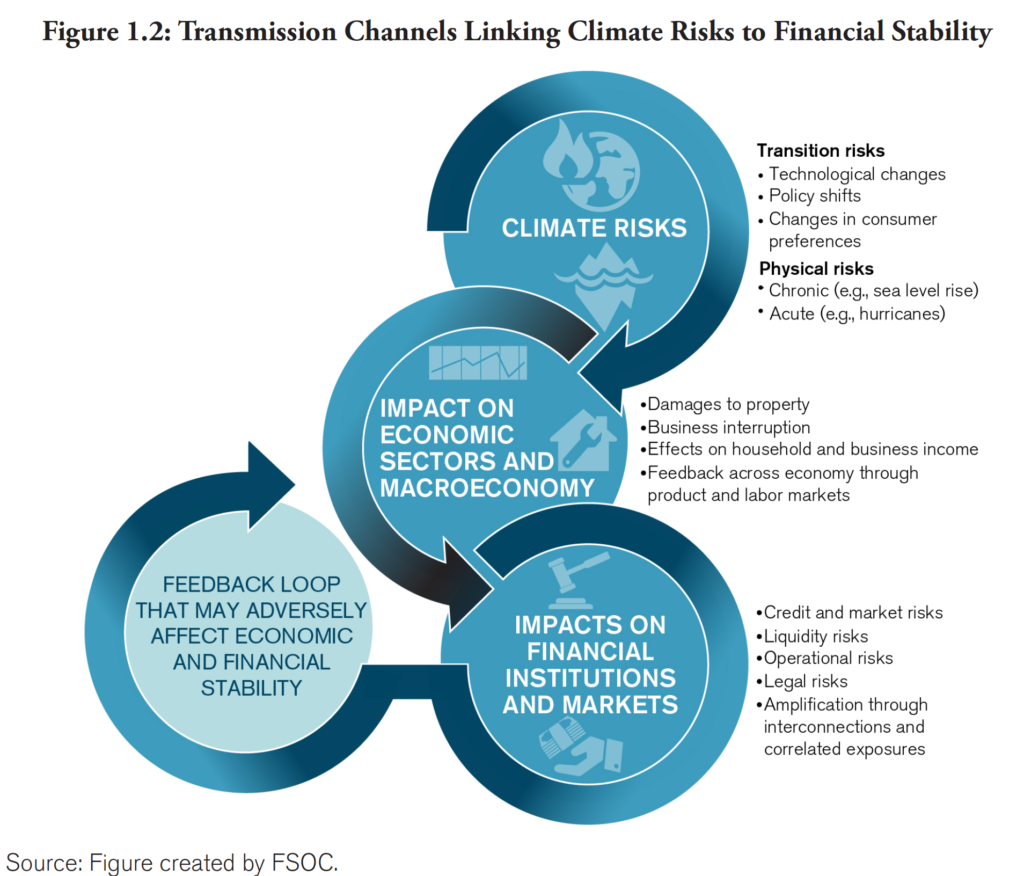

Climate risks—which are widespread and interconnected—pose a multifarious threat to the stability of individual financial institutions and the US financial system. Graham Steele, the assistant secretary of the US Treasury for financial institutions, has warned of a “climate Lehman moment,” highlighting similarities between systemic risks presented by climate change and those that spurred FSOC’s creation following the financial crisis of the late 2000s.

Systemic risk means that one financial actor’s vulnerability (or climate risk exposure) can jeopardize the well-being of other financial actors, corporates, and households economy-wide. Like dominoes, systemic risks can be passed through “transmission channels,” impacting seemingly disconnected parts of the economy. Acknowledging that climate risks are dynamic and interconnected directly challenges traditional approaches to assessing materiality and risk on an individual asset basis. Instead, systemic risks such as these must be assessed across an entire portfolio or the financial system as a whole.

“The resiliency of the financial system is, in part, dependent upon the resiliency of the firms that comprise it.” —FSOC Report on Climate-Related Financial Risks, p. 71

Notably, FSOC emphasizes that low-income and historically disadvantaged communities are especially entangled in the climate risk web. Not only will climate change disproportionately impact these communities, but they tend to be the least equipped to cope with the shocks. This, in turn, amplifies risks to the broader financial system.

“Financially vulnerable households, businesses, and communities are less likely to have the resources to protect and guard against damage to their properties or adequately deal with loss of income from an adverse climate or weather event. Such hardships can adversely affect the economic and financial strength of regions of the country and aspects of the financial system.” —FSOC Report on Climate-Related Financial Risks, p. 25

FSOC Acknowledges the Transition Is Inevitable

Why it matters: decarbonization is happening, and unprepared actors augment systemic risks by impeding a smooth and orderly transition, justifying government intervention.

“If appropriate policy actions are not taken by U.S. […] policy makers, the risks of both climate-related impacts to the financial system and of a disorderly transition will increase.” —FSOC Report on Climate-Related Financial Risks, p. 14

Efforts to keep global temperature rise below 1.5oC aim to prevent the worst physical risks of climate change, such as property damage from increasingly severe storms and wildfires. Yet decarbonization poses a double-edged sword, as the transition itself can introduce risks. Evolving market conditions, asset revaluation, and regulatory changes can either reduce or exacerbate costs of transitioning to a low-carbon economy. If actors ignore climate change, if assets are left stranded, or if abrupt triage policies become necessary, then climate-related costs will be significantly higher. This dynamic clarifies a role for regulators and policymakers to address the systemic risks introduced by unpreparedness and inaction.

Despite Data Shortcomings, FSOC Urges Regulators to Act Now

Why it matters: alongside mounting efforts to improve climate data and disclosures, regulators have the green light to assess resilience of financial institutions in a changing climate.

The pursuit of consistent, high-quality climate data continues to hamstring financial sector action on climate change. Data challenges include issues with tracking (monitoring emissions in real time), modeling (projecting forward-looking conditions), accounting (attributing emissions across real economy stakeholders), and operational barriers (integrating climate-related data into conventional financial models, especially for smaller institutions).

“Council members recognize that the need for better data and tools cannot justify inaction, as climate-related financial risks will become more acute if not addressed promptly.” —FSOC Report on Climate-Related Financial Risks, p. 13

Data and disclosures are constantly improving, but climate risks are already snowballing. In the absence of perfect data, FSOC promotes a proactive response, encouraging regulators and financial institutions to leverage the best available resources while working to improve those resources in parallel. As FSOC points out, not only can tools like scenario analysis be used in the absence of perfect data, but their use can actually lead to better data over time.

FSOC Stops Short of Addressing What Comes Next

Why it matters: regulator attention on climate-related financial risks is a milestone on the path to a climate-aligned financial sector, but there is much more work ahead.

While US regulators like the Securities and Exchange Commission (SEC), Federal Insurance Office (FIO), and Office of the Comptroller of the Currency (OCC) seem to be leaning forward on climate-focused actions, much regulatory focus remains on climate risk disclosure. Understanding climate-related risks and portfolio hot spots helps prioritize where action is needed, but it doesn’t provide a strategy for mitigating those risks. FSOC’s recommendations stop short of signaling how improved data, disclosures, and scenario analyses can be translated into strategies for transitioning the real economy toward a 1.5oC future. What happens after we know the extent of climate-related value at risk? How should an insurer balance solvency while keeping premiums affordable in high-risk areas? How does an asset manager move into greener investments when return uncertainty could run afoul of fiduciary duties?

Beyond Risk and Recommendations

The financial sector is at a crossroads. The reality of climate change guarantees tomorrow’s markets will look different than ever before, but the future depends on how and when financial institutions and regulators move forward. Risk measurement may provide signposts, but financial institutions and regulators will need novel techniques and roadmaps to steer their way to financial and economic stability.

The Center for Climate-Aligned Finance is committed to supporting financial actors on their alignment journey—helping them understand, leverage, and capitalize on their role in the transition. Beyond reacting to and managing risks, we envision a more proactive role for investors and lenders to drive decarbonization in the real economy. Active engagement with regulators is one of many influence levers financial institutions have at their disposal. We encourage financial institutions to communicate to regulators the barriers and opportunities they foresee on the path to climate alignment. And we encourage regulators to strive for a regulatory environment that equips financial institutions with the clarity, incentives, and long-term goals needed to enable, and make the most of, an inevitable transition.

Looking ahead, we need concrete action—initiated by financial institutions, with guidance and support from regulators—to translate recommendations into action toward 1.5oC-aligned, prosperous, and inclusive economies.

Interested in continuing the conversation? Get in touch!

Related Insights

Improving Energy Transition Assessments with Regional Pathways

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.