Shifting Currents

A New Wind Energy Opportunity for Corporate Buyers

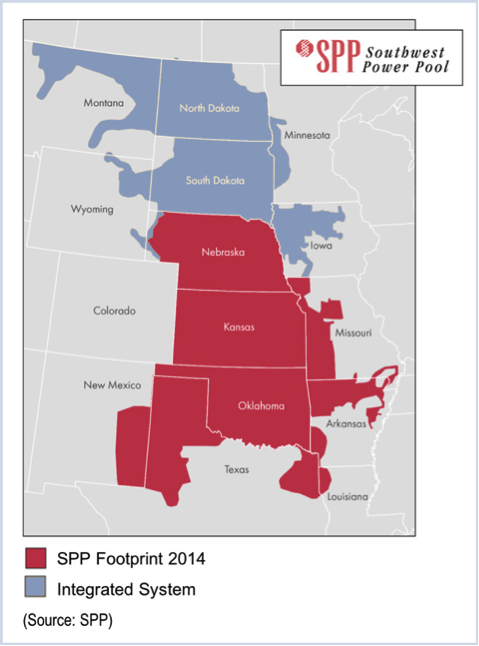

The regional power-grid operator Southwest Power Pool (SPP) has quietly become a leader in renewable energy, and recent improvements to its marketplace signal an opportunity for corporate buyers. With an estimated 19 gigawatts (GW) of planned wind capacity additions (more than three times the current total of corporate off-take deals), corporate buyers will have plenty of projects to choose from. In addition, if the Mountain West Transmission Group decides to join the SPP footprint, customers with load in Colorado or Wyoming could gain access to all that wind generation.

For corporate buyers with significant load in the region, or others looking to diversify their purchases regionally, SPP is a compelling market to explore. A new paper published by Rocky Mountain Institute’s Business Renewables Center, Transmission Investments Affect the Value of Your Wind PPA, examines some factors that influence the value of corporate power purchase agreements (PPAs).

MARKET CHANGES BENEFIT BUYERS

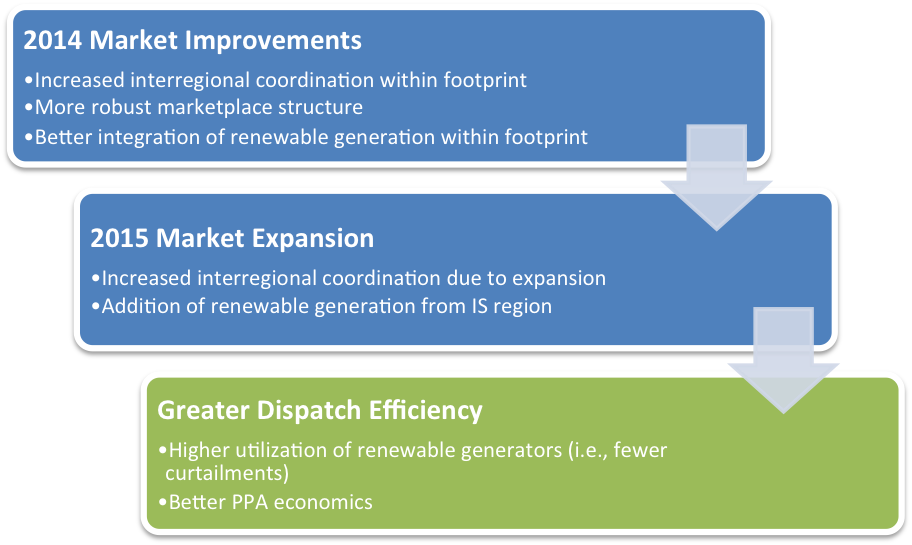

SPP has made two major improvements since 2014. First, SPP made various market improvements that saved $131 million in the first year of operations. Second, it expanded its footprint to include the Integrated System (IS) transmission system. These developments built on a period of strong investment in transmission infrastructure from 2012–2014 and have created a fertile environment for new wind projects, opening the door for more corporations to sign long-term power purchase agreements with developers in the region.

Figure 1: SPP Footprint Expands Northward

SPP made these changes to increase interregional coordination, which facilitates power exchange between regions and allows more renewable energy to flow from high-production regions to high-use ones. The result has been increased dispatch efficiency and lowered energy costs to its customer base. Previously, renewable generators faced more curtailments due to limited local demand and challenges in transmitting production to distant load centers.

Figure 2: SPP Changes Led to Lowered Energy Costs and Other Benefits

Reducing curtailments increases overall production volumes and reduces uncertainty, increasing the value of a PPA for a corporate off-taker.

EXCELLENT WIND RESOURCES RESULT IN LOWER PPA PRICES

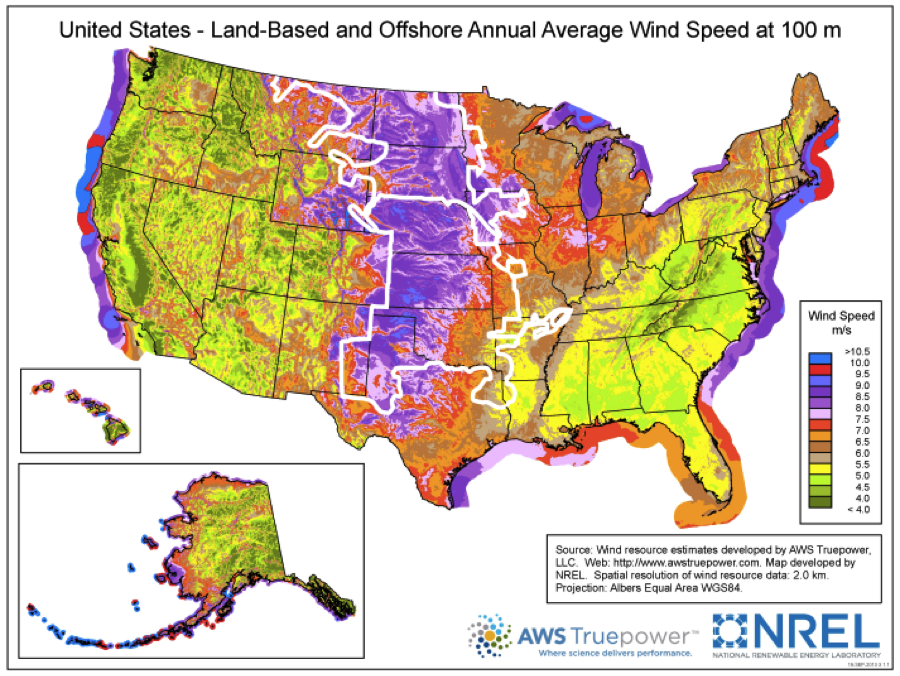

The former service territory of the IS and the service territory of SPP as a whole contain some of the best wind resource in the nation. Wind is already a significant source of generation in the region, making up about 12 percent of capacity for the former SPP region and about 15 percent of capacity for the newly integrated IS region. No other grid serves as high a percentage of its load via wind power—not even the Electric Reliability Council of Texas (ERCOT), which covers most of Texas. This is mostly due to the strength and consistency of the wind resource across the northern plains, as illustrated in the map showing average wind speeds across the U.S. (Figure 3).

Figure 3: U.S. Wind Speed Map, 100m Height

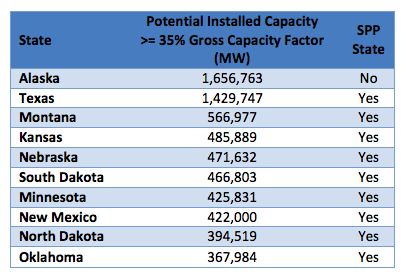

Strong wind leads to more generation over the course of a year per megawatt (MW) of installed capacity. This ratio between the annual output and installed capacity of a wind generator is called its capacity factor. For example, if a 100 MW wind generator were to produce an average output of 35 MW over the course of a year, it would have a capacity factor of 35 percent.

Table 1, based on an analysis done by the National Renewable Energy Laboratory in 2015, illustrates the high output of wind installations in the SPP region. Nine of the top 10 U.S. states in terms of potential for high-capacity-factor wind generation (defined here as having a capacity factor greater than or equal to 35 percent) are part of the SPP footprint.

Table 1: Top 10 U.S. States – Potential for High-Capacity-Factor Wind Generation (Source: DOE)

Generators with higher capacity factors are able to recover up-front capital costs over larger production volumes, resulting in lower unit costs for the energy produced. Lower costs result in lower negotiated PPA prices, improving economics for corporate buyers.

MORE WIND GENERATION TO COME IN SPP

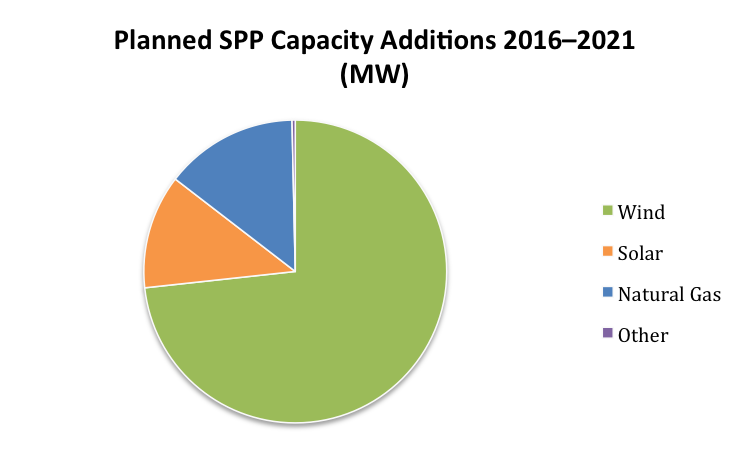

Developers in SPP are already planning to build a significant amount of wind generation over the next few years. SPP’s generation interconnection queue, which lists the status of all planned generation projects in the region, is made up of 73 percent wind generation, as shown in Figure 4. Most capacity is planned to come online in 2017, when almost 7 GW of wind generation are expected to be completed. This is indicative of the favorable development environment for wind generators in SPP and highlights a robust pipeline of potential suppliers of renewable energy for corporate buyers.

Figure 4: Planned SPP Capacity Additions by Generation Type, 2016–2021 (Source: SPP)

There are indications that the pipeline of wind developments in SPP will grow even larger. Despite its large proportion of wind and hydro generation, SPP still serves about 60 percent of its load using coal generation. As a result, states in SPP will face significant challenges in complying with the EPA’s Clean Power Plan. In an April 2015 assessment of the plan, SPP estimated that an additional 5.6 GW of wind capacity (42 percent more than currently planned) would be needed to ensure compliance.

RISKS AND OPPORTUNITIES FOR CORPORATE PPAS

Similar to ERCOT to the south, SPP has made strong investments in transmission infrastructure to support wind development. However, if the pace of wind development outstrips the pace of transmission infrastructure improvements, curtailment will increase and wind PPA economics will suffer. Therefore, it is important for corporate buyers to consider the impacts of future transmission investments when evaluating a potential PPA in the region.

Buyers should also keep an eye on policy changes in the region. For example, this year Oklahoma may eliminate a tax credit benefiting wind generators in the state. If the proposed bill passes the state’s Senate, it could stifle wind development in Oklahoma and push developers to explore other states in the region. At the same time, it will be important to monitor if other states follow Oklahoma’s lead.

For companies investigating renewable energy PPAs, projects in SPP are a good complement to wind generators in ERCOT and elsewhere. Favorable advancements in market sophistication and a robust pipeline of wind development have created an attractive opportunity for corporate buyers. SPP has also shown commitment to improving transmission infrastructure to support wind development. Those corporations looking to diversify their purchases or offset consumption in the region should take a long look at SPP.

Image courtesy of iStock.