Learn how we are working to transform how we use and produce energy.

Charting the Course to Climate-Aligned Finance

Five Barriers to Alignment and How a Sectoral Approach Can Help

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

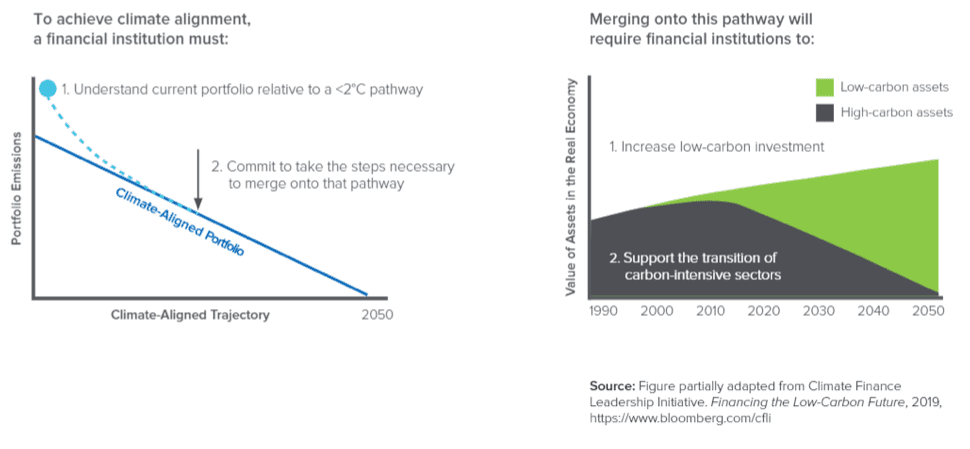

By the end of 2019, financial institutions representing $17.2 trillion had committed to align their investment portfolios with the decarbonization goals of the Paris Agreement. The scale of ambition is exciting, but the question remains: How can banks and other financial institutions meet these climate alignment objectives?

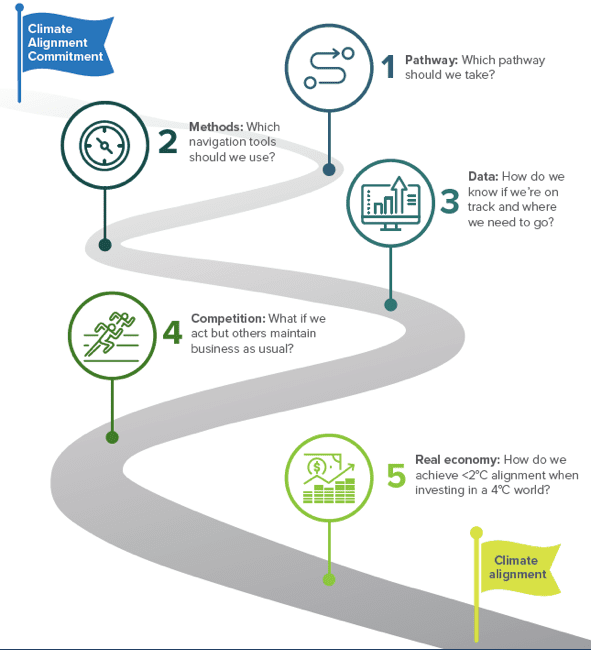

This brief offers key insights for financial institutions who are considering or are have already begun to align the emissions impacts of investment portfolios and activities with global decarbonization targets. The brief outlines five common barriers that institutions face when attempting to achieve climate alignment, and details how a sector-by-sector approach to alignment can provide an efficient, pragmatic, and effective way forward.

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.