Micropower’s Quiet Takeover

In a cover story and article 14 years ago about the emergent disruption of utilities, The Economist’s Vijay Vaitheeswaran coined the umbrella term “micropower” to mean sources of electricity that are relatively small, modular, mass-producible, quick-to-deploy, and hence rapidly scalable—the opposite of cathedral-like power plants that cost billions of dollars and take about a decade to license and build. His term combined two kinds of micropower: renewables other than big hydroelectric dams, and cogeneration of electricity together with useful heat in factories or buildings (also known as combined-heat-and-power, or CHP).

Besides being cost-competitive and rapidly scalable, why does micropower matter? First, as explained below, its operation releases little or no carbon.[1] Second, micropower enables individuals, communities, building owners, and factory operators to generate electricity, displacing dependence on centralized, inefficient, dirty generators. This democratizes energy choices, promotes competition, speeds learning and innovation, and can further accelerate deployment—because “vernacular” technologies accessible to many diverse market actors, even if individually small, tend to deploy faster in sum than a few big units requiring specialized institutions, complex approvals, intricate logistics, and hence long lead times.

Thanks to Bloomberg New Energy Finance, which tracks investments and generating capacity, and the global expert network REN21.net, which tracks capacity and (where known) electrical output, global progress in renewables has become rather transparent. Starting in 2005 and updated with a fifth edition in July 2014, RMI’s Micropower Database added a third source: industry sales data for cogeneration equipment. Tracking renewables, minus big hydro, plus cogeneration, this database documents the global progress of distributed, rapidly scalable, and (as we’ll see) no- or low-carbon generators.

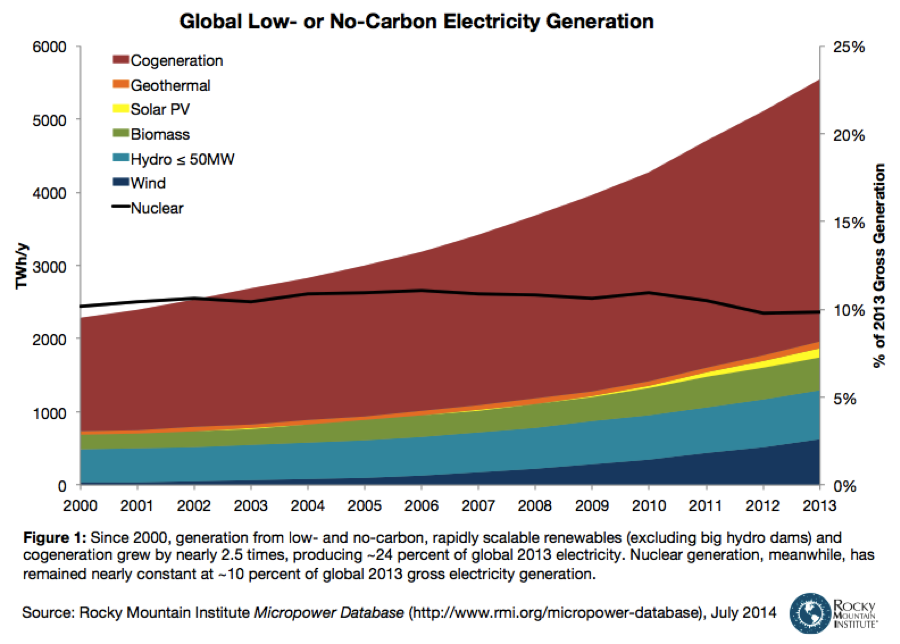

The update’s most astonishing finding: micropower now produces about one-fourth of the world’s total electricity (Fig. 1).

MICROPOWER’S CLIMATE IMPLICATIONS

Operating modern renewables is essentially carbon-free, except for minor subsets fueled by biomass grown using unsustainable practices that gradually deplete soil carbon.[2] Of the estimated 3–5 percent of cogeneration fueled by biomass, most is in the forest products industry, whose biomass wastes produce most of its electricity and process heat.

Cogeneration in refineries often burns waste fuels that would otherwise be uselessly flared. Similarly, much industrial cogeneration harnesses waste heat previously thrown away. Where extra fuel is burned to make electricity as well as heat, typically far less is burned than when making them separately. If cogeneration also produces cooling and other services, it can convert as much as 93 percent of fuel energy into useful work, both in industry and in buildings. Moreover, the natural gas that fuels most cogeneration is only about half as carbon-intensive as the coal-fired power-only generation it often displaces.[3]

Big hydroelectric dams and nuclear power are also carbon-free in operation. Thus in 2013, nearly half of the world’s electricity was produced with little or no carbon release: 8.4 percent by modern renewables [4], 10.2 percent by nuclear power (set to be overtaken by modern renewables in 2015), 15.5 percent by cogeneration [5], and 13.5 percent by big hydroelectric dams (excluding the 2.8 percent small hydro classified under modern renewables).

The other half came from power-only plants, burning mainly coal. Those plants cost more to build, and often more just to run, than their competitors, so their orders are fading, their operations are dwindling, and over decades, they’ll retire in favor of cleaner, cheaper substitutes—both micropower and efficient use.

WINNERS AND LOSERS

Far from recognizing that they’re being rapidly overtaken, many advocates of coal or nuclear power stations don’t even acknowledge micropower as an important competitor—even as it grabs their markets and destroys their sales. In 2009, a senior strategic planner for a major nuclear vendor told me micropower was trivial—having failed to find it in official databases of utility-owned central power stations, without understanding the difference. And even at minor market share, micropower can have major effects. The solar 4.7 percent of Germany’s 2013 generation destroyed the incumbent utilities’ business model and wiped a half-trillion Euros off their market cap.

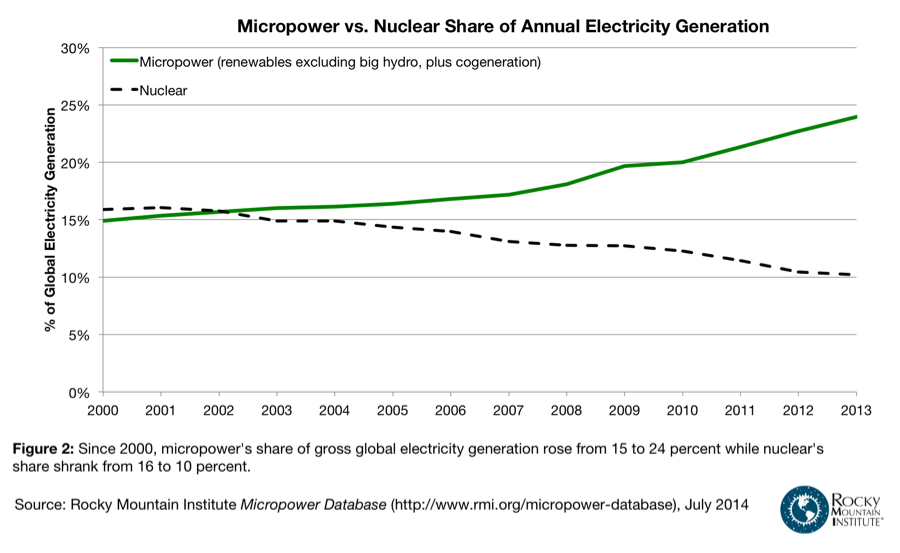

Yet by the end of 2013, the rapid output growth of both modern renewables and cogeneration (Fig. 1) had eclipsed shrinking nuclear power by 3.34-fold in capacity and 2.35-fold in output. Modern renewables alone, those other than big hydro dams, reached 1.95 times nuclear power’s capacity in 2013 and should exceed its annual electricity output by 2015. This role reversal (Fig. 2) is accelerating, due mainly to economics and to modular renewables’ extraordinarily dynamic scaling mechanism.

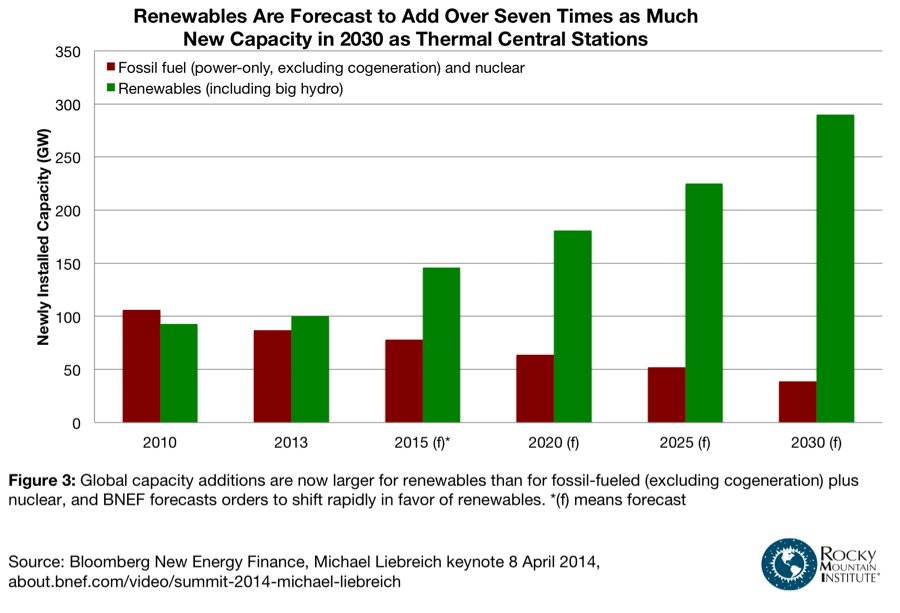

The trends are even clearer when we look at where today’s money is invested, because power plants built long ago tell us only about the past, while those now being ordered reveal the future. More new renewable capacity than fossil-fueled plus nuclear capacity was added in 2013. As orders grow for renewables but shrink for central thermal stations, Bloomberg New Energy Finance expects that by 2030, new renewable capacity, including big hydro, will exceed new thermal capacity by 7.4-fold (Fig. 3), without even counting cogeneration.

For micropower as for cellphones and personal computers, the race goes to the quick—but photovoltaic power worldwide is scaling up even faster than cellphones. Advocates who assume renewables can’t do much without a breakthrough in bulk storage of electricity are in for a rude awakening.

Banking giant UBS calls the big, slow, lumpy, expensive coal and nuclear plants “the dinosaur of the future energy system: Too big, too inflexible, not even relevant for backup power in the long run.” Such obsolete technologies are less at risk from regulatory mandates than from market defeat by a swarm of agile competitors that their promoters don’t even recognize. What a sad epitaph—Devoured by Invisible Ants.

[1] Carbon emissions embodied in the energy and materials used to produce different kinds of energy equipment are separate, relatively small, and broadly consistent with their relative economic costs, so they’re not further examined here. New hydro dams that flood big areas can also release large amounts of methane from the rotting of submerged vegetation.

[2] U.S. woodchip exports, chiefly for cofiring Britain’s Drax coal plant, raise such concerns but aren’t in RMI’s database because Drax is a giant power-only station, not a smaller cogenerator.

[3] However, this comparison ignores the unknown degree of methane leakage from both the gas and the coal systems, the export of displaced coal that is then burned abroad, and cogeneration’s potential displacement of some carbon-free generation.

[4] RMI’s estimate of 2013 electricity production exceeds the ~6 percent stated by the authoritative REN21.net global expert network. That’s because RMI includes 191 GW of small hydropower <50 MW, based on Bloomberg New Energy Finance (BNEF) transaction-based capacity data, while REN21’s 6-percent figure excludes all hydropower.

[5] Conservatively excluding large industrial installations: RMI’s database includes all cogenerating turbines up to 30 MW, but fractions decreasing down to 5 percent for ≥120 MW.

This article originally appeared on Forbes.com.