Learn how we are working to transform how we use and produce energy.

How to Make Finance Cheaper, More Accessible for EVs in India

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Finance as a Barrier to EV Adoption

If you are looking to buy an electric vehicle (EV) for your business or personal use, you may be surprised to find that the interest rate on the loan for the EV will likely be higher than a comparable diesel- or petrol-powered vehicle. You are also asked for a larger down payment for your vehicle. Why is this?

Risk is the main cause for these financing challenges. An EV is considered a riskier class to finance than an internal combustion engine vehicle. EVs face a range of risks that can be categorized as asset risk and business model risk:

- Asset risk is the risk that is associated with the financing of a vehicle. It includes risks related to technology, policy, manufacturing, and resale.

- Business model risk is the risk that is associated with the use of a vehicle. It includes risks related to customer profile, expected utilization, and operations and maintenance.

As a result of these risks, banks and non-banking financial companies (NBFCs) in India are not only requesting higher interest rates for EVs, but also financing a smaller share of vehicle value. Also, there are few specialized loan products for EVs, and insurance rates can be higher for some segments and use-cases.

Together, these pain points make finance a considerable barrier to EV adoption. As India prepares for increasing levels of EV adoption, leaders in government, industry, and finance must address the growing need to mobilize low-cost capital towards EV assets and infrastructure.

Potential of India’s EV Financing Market

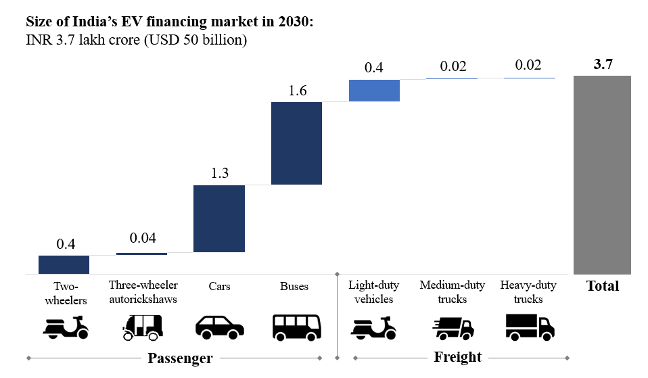

According to our latest report, Mobilising Finance for EVs in India, coauthored with NITI Aayog, over the next decade India’s EV transition will require a cumulative capital investment of 19.7 trillion Indian rupees (₹) (US$266 billion) in vehicles, charging infrastructure, and batteries. By 2030, our analysis indicates that the market size for the financing of EVs in India has the potential to be ₹3.7 trillion ($50 billion), as shown in Exhibit 1.

For reference, India’s retail vehicle finance industry is estimated to be worth about ₹4.5 trillion (US$60 billion) today. Upwards of 50 percent of two-wheelers, 80 percent of private four-wheelers, and 95 percent of light-, medium-, and heavy-duty commercial vehicles sold in the country are financed through loans. Given current levels of financing penetration, it will be important for the vehicle finance industry to proactively engage in the EV transition.

Toolkit of Solutions to Enable EV Finance

Considering the future capital and financing requirements for India’s EV transition, it is important to start developing solutions to enable finance for EVs today. In the report, we have proposed a toolkit of financial instruments for leaders in government, industry, and finance to apply to the EV sector. Five powerful instruments in the toolkit include:

- Priority sector lending (PSL): The Reserve Bank of India requires 40 percent of net bank credit to be deployed towards priority sectors. Inclusion of EVs in PSL guidelines would incentivize banks to increase lending towards the sector.

- Interest rate subvention: Subventions act as a subsidy on commercially offered interest rates, with a government or another entity bearing the balance through associated banks. Such schemes would substantially improve the affordability of loans and have already been enacted at the state level for EVs in Delhi.

- Product guarantees and warranties: Original equipment manufacturers (OEMs) can provide assurances in the form of guarantees (to financial institutions) and warranties (to buyers) on the performance of their products. Reducing the uncertainty associated with EV models would improve the risks they pose to bankers.

- Risk-sharing mechanisms: National and multilateral financial institutions can provide capital to establish risk-sharing facilities that offer loan-loss reserves or loan guarantees to banks and NBFCs to partly or entirely cover possible losses that they could incur when financing EVs. Fleet operators, such as final-mile delivery companies, can also create risk-sharing mechanisms by providing partial credit guarantees for financial institutions and utilization guarantees for drivers.

- A partial credit guarantee acts as a form of insurance for banks and NBFCs, protecting them from a driver that does not make their loan payment.

- A utilization guarantee serves as a contract with the driver for certain amount of work or revenue per day or month, which the driver can show to a bank or NBFC as proof of their ability to repay a loan.

- Secondary market development: Through industry-led buyback programmes and battery repurposing schemes, OEMs and the central government can catalyze a secondary market for EVs. This would improve the residual value of EVs by providing financial institutions with an avenue for resale in case of borrower default.

These solutions would not only help lower the cost of capital and increase the quantum of finance available for EVs, but also play important role in stimulating India’s economic recovery by supporting job creation and local value addition.

Operationalizing EV Finance Solutions

To operationalize this toolkit of financing solutions, the country’s EV ecosystem can first engage more proactively with Indian and international financial institutions. Risk reduction will require a multi-stakeholder approach to identifying, designing, and linking financial instruments like the ones we have outlined.

Second, governments can seek the input of financial institutions on policy making and industry can help familiarize them with EV technology and business models. Third, research and convening work can help pressure test potential financing solutions and identify actionable steps to operationalize them through policy making and decision making within financial institutions. Over time, this can contribute to lowering risk in the EV sector.

While India’s vehicle finance industry is unique, the risks of financing EVs are universal. If India can work towards mainstreaming solutions to lower the cost of capital for EVs, it could not only help lower your interest rates and down-payments, but also accelerate domestic adoption and set an example for other nations to follow.

Authors

Ryan Laemel

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.