Learn how we are working to transform how we use and produce energy.

How Pension Funds Can Help Electrify Africa

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Almost 600 million people in Africa do not have access to electricity. Bringing them clean, affordable, and reliable electricity will require massive investment. At the same time, African pension funds are actively seeking to grow their assets under management (AUM) and diversify their asset portfolios. If these pension funds invest in clean energy projects, they can trigger a positive economic-growth feedback loop. Electricity access will increase productivity and subsequently the income of Africa’s young population (median age of 19.7 years). When coupled with ongoing efforts to extend pension coverage to the informal employment sector, this creates a win-win of growing pension fund AUM.

There is a unique and sizable opportunity for pension funds to invest in long-lived energy infrastructure projects that align with their long-term obligations (in the form of payouts for pension benefits). While there is consensus on the potential for global and local pension funds to invest in African energy projects, which some are already investing in, African pension funds can play a bigger catalytic role for the sector beyond niche projects. However, this requires coordination with other funding sources to appropriately allocate capital while matching project development phases and their associated risks.

The Energy Finance Challenge

As nations in sub-Saharan Africa advance their industrialization and economic growth agendas, renewable energy infrastructure is increasingly at the forefront of discussion. The cost of solar-battery electricity systems has fallen significantly in the past decade, making renewables the cheapest form of electricity generation in many parts of the globe. Recent African Development Bank projects have shown it to often be the least-cost resource in sub-Saharan Africa as well.

IRENA estimates that Africa needs about $70 billion in annual renewable energy investment until 2030. This would improve electricity reliability for communities plagued by brownouts and blackouts like in Nigeria and Ghana and bring electricity to communities across the continent without it. However, only $30 billion and $10 billion were invested in sub-Saharan Africa renewable energy projects in 2019 and 2018 respectively.

This underinvestment is further exacerbated by the imbalance in funding sources. Most of the finance for infrastructure projects including energy, is from foreign investors like development financial institutions (DFIs), with local finance mainly coming from cash-strapped governments. Relying heavily on foreign currency capital creates foreign exchange risks because revenue from energy projects—in the form of electricity tariffs—is collected in local currency. Furthermore, the risk profile of energy projects in markets where international investors are unfamiliar with the ground realities of energy consumers creates information asymmetry that increases perceived risk, raising the cost of capital for projects.

An Alternative Asset Class Opportunity

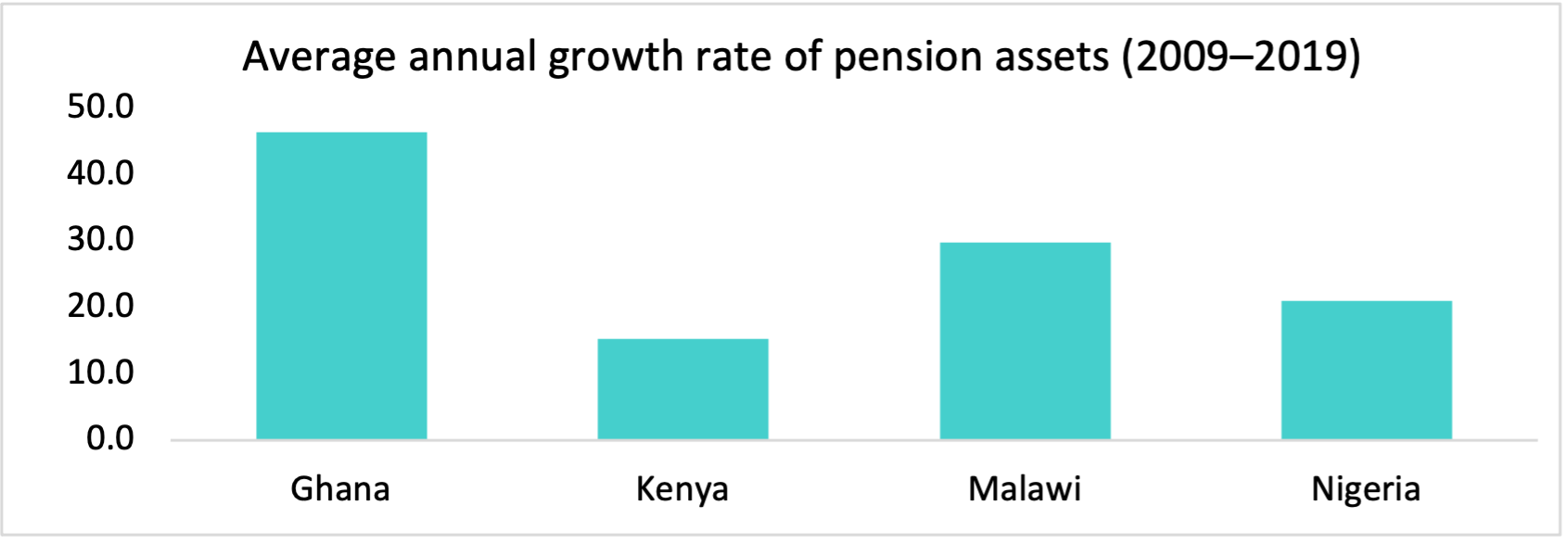

In the past decade, pension funds in sub-Saharan Africa have experienced varied but significant growth of AUM ( Figure 1). Based on a sample of 33 African pension funds (excluding South Africa), the Brookings Institution estimates that African pension funds can invest about $11.7 billion annually in infrastructure projects.

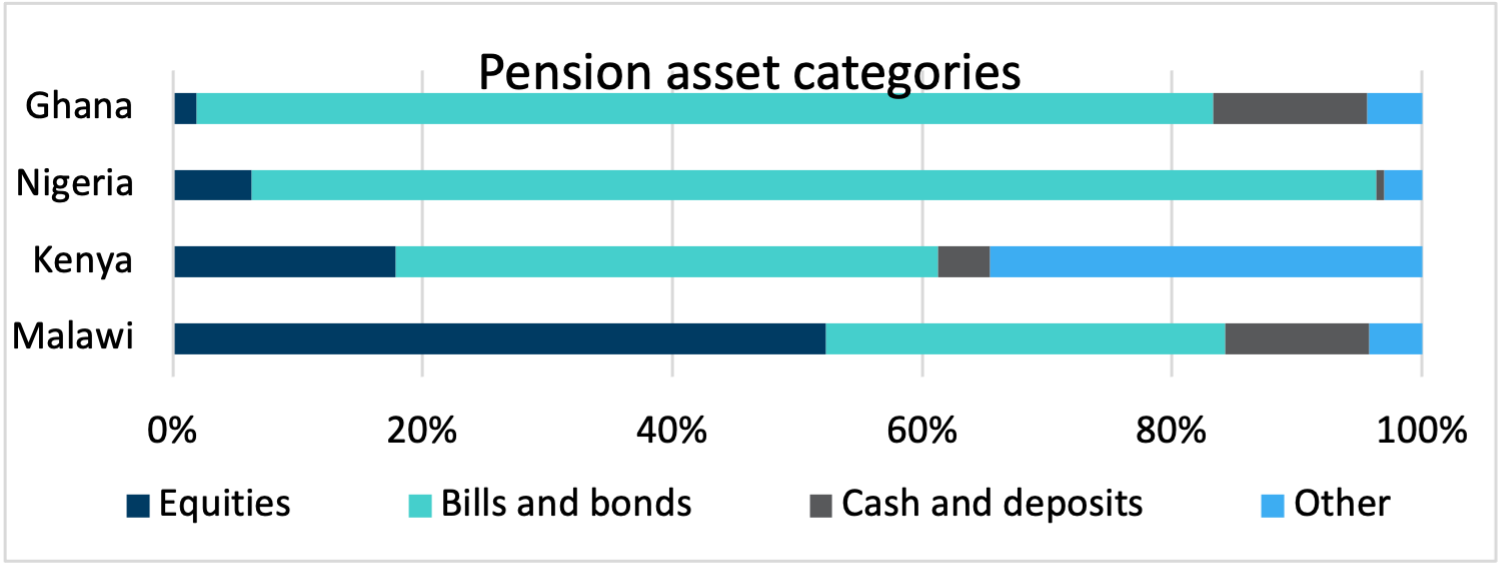

Securitizing the revenues of energy projects and selling them as “renewable energy-backed” bonds (RE bonds) is one way of creating an infrastructure investment product that is suitable for pension funds. African pension funds invest in a diverse range of assets including significant investment in fixed income assets (investments with a fixed periodic return like bonds) as shown in Figure 2. Bonds are a desired investment instrument due to low-risk perception, while in some instances, direct investment in development of infrastructure projects is limited by pension fund regulations.

The risks of investing directly in renewable energy projects at development or construction stage include lengthy bureaucracy of permitting and land acquisition. They can also include delays in construction from underdeveloped logistics and inexperienced technical teams as well as potential inability or willingness of customers to pay for electricity. Developing bond-investable projects will require collaboration with financial institutions like banks and DFIs that have higher risk tolerance to fund these project stages.

At early project development, local developers with local context knowledge and experience can lead on developing portfolios of projects using grants and concessional finance. One example of this approach is the United States Trade and Development Agency (USTDA) grant funded project where Abuja Electricity Distribution Company (AEDC) is collaborating with RMI in derisking portfolios of embedded distributed energy projects, to support private-sector fundraising for construction of viable projects.

International developers with strong balance sheets, experience, and supply chain relationships can construct projects using bank loans and then refinance the loans (pay off debt typically with new debt at a lower interest rate) with RE bonds after project commissioning. Expected return on investment for local pension fund assets can be as low as 2–5 percent for the “fixed income” asset class, which is much lower than bank lending interest rates that can be as high as 15 percent, 13 percent, and 25 percent in Nigeria, Kenya, and Malawi respectively.

RE bonds backed by energy bill payments enable pension funds to invest in commissioned projects with more visibility on the project’s potential to generate future income based on realized electrical system performance and revenues. Bonds are rated by certified credit rating agencies based on their risk profile. Pension funds, due to their fiduciary duty of protecting the pensions of beneficiaries, invest in the highest rated bonds with the lowest risk.

Other financial institutions can support RE bond market development by providing guarantees for credit enhancement to attain high bond ratings that attract pension fund investment. For instance, under Nigeria’s regulatory framework, pension funds can only invest in infrastructure bonds with credit enhancement through guarantee to secure pension assets from project risks.

The Way Forward

The match between African pension funds and electrification projects can be unlocked by RE bonds, which represent a viable asset class similar to pension funds’ existing investments in fixed income assets. For this to happen, three barriers need to be overcome.

- Pension funds need access to appropriate energy investment vehicles.

There is a high level of complexity in coordinating multiple sources of finance for each stage of project development to generate a portfolio of bond-investable projects, which subsequently raises due diligence costs. Green banks can play a key “investment vehicle” role in organizing this kind of multi-financier model as well as bridging funding to portfolios of projects. DFIs and African governments can lead the design and capitalization of green banks by restructuring the role of existing infrastructure investment vehicles like national development banks or infrastructure funds.

- The pension fund regulatory framework needs to support investment in RE bonds.

Currently, there are restrictions across the continent on pension funds liquidity as well as limits on how much they can invest in assets like infrastructure projects, to manage perceived risks. Coupling RE bonds with guarantee schemes funded by governments with support from DFIs will lower the risk perception of these bonds. This lowers their accounting impact on liquidity of pension funds. Public sector investment in credit enhancement schemes is a more efficient use of limited capital to attract broader private sector resources.

- African governments need to clearly define their environmental policies to attract sector investment.

Policies like subsidies for fossil fuel energy, though necessary to ensure affordable electricity tariffs for low-income populations, impact the perception of investors like pension funds on renewable energy competitiveness. Through holistic energy system planning for future investments, African governments can utilize cheap renewable energy and redirect subsidies toward clean energy. They can also increase visibility of their commitment to clean energy by implementing procurement systems like renewable energy auctions. These policy changes lower the risk perception of prospective investors toward renewable energy projects.

African pension funds can be an effective tool to help bring clean, reliable electricity to hundreds of millions of people throughout Africa. However, it is essential to overcome the above-stated barriers now to support economic development across Africa, manage the environmental impact of development, and support adaption to climate change in this decisive decade.

Authors

Patience Bukirwa

Related Insights

Bringing Clean Energy Opportunities to Women and Youth in Nigerian Agriculture

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.