Learn how we are working to transform how we use and produce energy.

Energy and Affordability in Housing Finance

How Fannie Mae and Freddie Mac are reducing the energy burden for underserved markets

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Utility costs place a significant financial burden on the 35 million very low- to moderate-income (LMI) single-family households in the United States. On average, low-income households spend three times as much to heat and cool their homes as the average household—from 20 percent to 50 percent of their monthly earnings in some parts of the country. These costs create real hardships, making living costs untenable and families more vulnerable. If left unaddressed, this affordability crisis will also present a growing risk to lenders. But Fannie Mae and Freddie Mac, which together account for over 70 percent of the $6.4 trillion residential mortgage-backed securities market, recognize the extent and importance of this housing affordability challenge and have committed to do something about it.

The GSEs’ Duty to Serve

The mission of the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac is to provide liquidity, stability, and affordability to the US residential mortgage industry by creating a secondary market. Given the scale of their operations, they also have significant influence in setting underwriting standards and requirements for lenders and appraisers nationwide. After the financial crisis, the Housing and Economic Recovery Act of 2008 assigned both GSEs a “Duty to Serve” specific underserved markets—rural, manufactured, and affordable housing preservation—by improving the liquidity and distribution of mortgage capital for families of modest means.

At the end of 2016, both Fannie Mae and Freddie Mac submitted three-year Duty to Serve plans to their regulator, the Federal Housing Finance Agency (FHFA). Both GSEs reevaluated and restructured their approaches to better serve these underserved segments of the housing market and create opportunities for enhanced access to capital in these markets. As part of that process, they opened up their plans to comprehensive public review and comments from a diverse group of stakeholders.

Rocky Mountain Institute—along with a coalition of partners—actively advocated for the inclusion of energy and water conservation considerations as part of FHFA’s initial Duty to Serve criteria for single-family and multifamily affordable housing preservation. RMI also participated in the ensuing process of commenting on Fannie Mae’s and Freddie Mac’s underserved market plans, organized and informed other stakeholder responses, and submitted detailed comments relating to energy considerations for the preservation of affordable single-family housing stock. Many of these suggestions were successfully incorporated into the GSEs’ final Duty to Serve action plans for 2018 through 2020.

“The challenges of providing a stable supply of homes that are affordable to those with very low, low, and moderate incomes are many and complex,” said Mike Dawson, vice president of Freddie Mac’s single-family affordable lending strategies and initiatives. “The Duty to Serve rule is an opportunity—one we truly welcome—for us to lead the entire mortgage industry. It allows us to look beyond housing, to understand the broader problems facing underserved markets, and to test and apply a new generation of comprehensive solutions. We’re grateful for our partnership with RMI and its expert guidance and insights on the impacts energy costs have on these underserved markets.”

Energy Efficiency and Affordable Housing

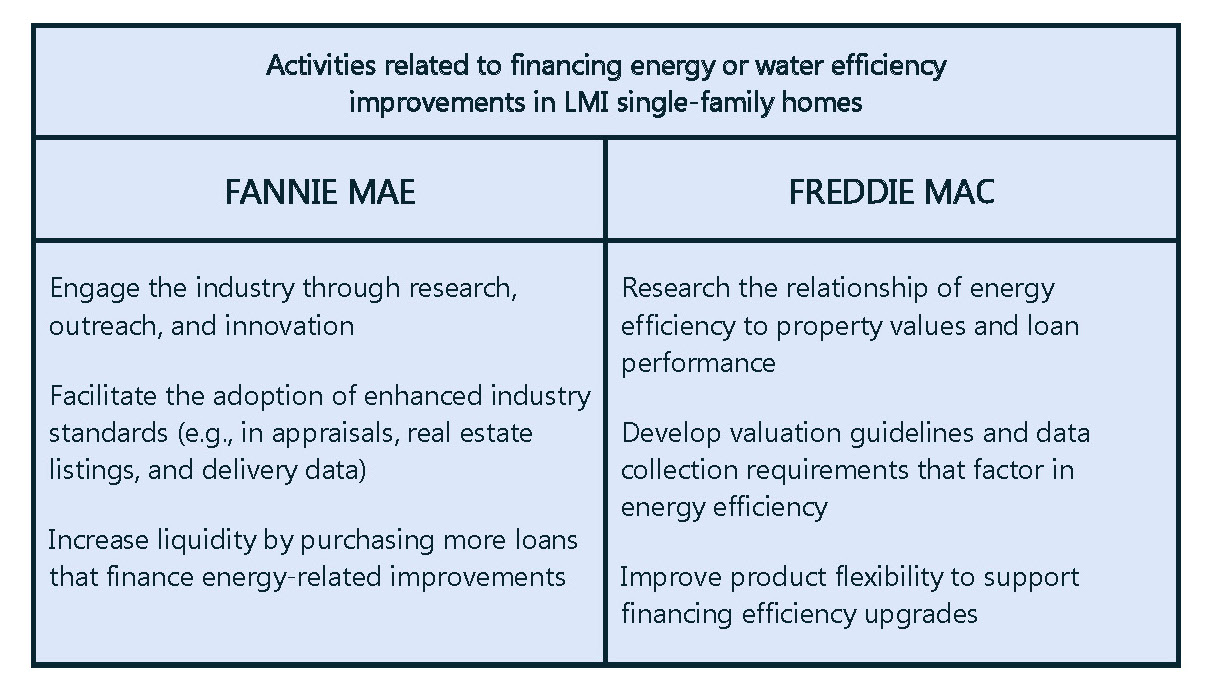

In both of the GSEs’ ambitious action plans, specific sections outline key activities they will pursue to improve financing for energy efficiency improvements in affordable single-family housing. These activities are summarized at a high level in the table below:

Both action plans reflect the importance of addressing the higher energy burdens of LMI households and demonstrate Fannie Mae’s and Freddie Mac’s openness to updating standards and processes through research, innovation, and collaboration. More importantly, the GSEs show in the plans an intent to change the products they offer to improve service to this segment of the market. Their commitments send powerful signals to the marketplace, elevating the conversation and increasing awareness of these issues—not only for lenders but also for borrowers, appraisers, brokers, and other real estate market participants nationwide.

Progress

The GSEs are updating existing products and guidelines to improve liquidity in the LMI market while providing the right market incentives for LMI homeowners to upgrade their existing homes to be more energy efficient and resilient and derisking the underlying assets for lenders. Both GSEs have begun work on their proposed plans for underserved markets.

As set forth in its action plan, Freddie Mac is embarking on a comprehensive study to determine the impact of energy efficiency on loan performance and home valuations. Fannie Mae recently announced updates to its selling guide for lenders that remove constraints and add certain flexibilities that support the increased use of its energy improvement financing product, HomeStyle® Energy. Additionally, this loan product can now be used for repairs or upgrades that strengthen a home’s ability to withstand environmental disasters such as floods, storms, and earthquakes—which goes a long way toward better supporting LMI households that are often hit harder by these events.

“We are excited our Duty to Serve efforts include exploring innovative solutions and strengthening our current offerings that help very low- to moderate-income homeowners and tenants save money and afford housing costs,” said Rita Ballesteros, manager of Fannie Mae’s Single Family Duty to Serve Affordable Housing Preservation initiatives. “Our collaboration with RMI is opening new relationships and concepts to support this complex but important underserved market.”

Beyond Duty to Serve

The GSEs’ leadership is creating exciting possibilities for improving residential energy performance and access to financing for this purpose, starting with the market segments that need it most. And, given their scale, these new commitments are likely to create long-lasting ripple effects that can transcend underserved segments by establishing standard guidelines and precedents for better valuation and pricing signals that reward higher-performing homes. Fannie Mae and Freddie Mac’s work under Duty to Serve is a big step in the right direction and will not only support the American dream of affordable and resilient homes for all, but will also help support growing city leadership across the United States to address climate risk in the buildings sector.

RMI’s Residential Energy+ team continues to cultivate industry collaborations and market interventions that improve the energy performance of the US residential housing stock. Specifically, our Finance the Future work aims to increase the availability of capital for home energy improvements and improve the transparency of energy performance information throughout the real estate process. We look forward to following and supporting the progress of Fannie Mae and Freddie Mac under their Duty to Serve commitments and beyond.

Related Insights

What Michigan’s Clean Community Financing Ecosystem Can Teach Other US Regions

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.