Learn how we are working to transform how we use and produce energy.

Corporate Renewable Energy Procurement in China

The State of the Market and Looking Ahead

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

The past year has been an exciting time for corporate renewable energy procurement in China. The Chinese National Energy Administration (NEA) released three drafts of a new Renewable Portfolio Standard (RPS) policy for comment and intends to implement this policy on January 1, 2019. Concurrently, an increasing number of companies have set up sustainability targets, aggressively aiming to procure renewable energy and advance renewable energy development in China. The Business Renewables Center (BRC) China’s new report, State of the Market 2018—Corporate Renewable Procurement in China, is a comprehensive update on corporate renewable procurement in 2018. The report highlights the macro changes in the national renewable energy landscape (which is influencing national policy), summarizes major policy changes impacting corporate procurement, and represents the development of renewable procurement mechanisms. Below we highlight four takeaways from the report.

1. Curtailment will continue to influence national renewable energy policy.

Over the past decade, China has become the world’s leader in wind and solar capacity with 15 percent compound annual growth rate from 2008 to 2017. This growth has been driven by government targets and supported by a feed-in-tariff (FiT), which provides two guaranteed revenue streams to projects, one from grid companies and the second from the national government. While this approach has resulted in extensive solar and wind capacity growth, capacity curtailment has also been persistent in the northern provinces where renewable resources are abundant, and load is (comparatively) light.

The average national curtailment rate improved from 2016 to 2017—from 17 to 12 percent. Three provinces with the highest curtailment ratios, namely Gansu, Xinjiang and Jilin, reduced their curtailment by 9 percent, primarily through:

- Better system operations to allow more flexible dispatch;

- the introduction of an interprovincial spot market for otherwise-curtailed renewable energy, allowing market incentives to purchase renewables; and

- an ancillary pilot market in northeastern provinces.

However, curtailment challenges still remain; eight provinces had annual curtailment rates over the national target of 5 percent, and three provinces were above 20 percent.

Separately, growth expectations outstripped national government forecasts and exceeded budget expectations (funding the second revenue stream). As a consequence, project developers are facing liquidity challenges as subsidy payments are being delayed for up to two years, due to the renewable funding deficit.

2. China is moving toward a reverse auction approach.

To reduce the national funding burden, the government intends to move away from the FiT mechanism, and push for grid parity through a reverse auction process (as is increasingly occurring in other countries) coupled with an RPS system. We believe this change could enable additional market mechanisms to support renewable energy development. To start this transition, two policies were released in May 2018 introducing two significant changes:

- Starting in 2019, all new utility-scale wind projects will be required to submit price bids to be integrated into the grid.

- The FiT rate for solar projects was reduced by 0.05 RMB/kWh for all projects under development and commissioned after the policy was released. No new utility-scale solar projects that need subsidies were permitted in 2018. Also, a cap of 10 GW per year was placed on FiT-qualifying distributed capacity, which effectively ceased development of additional solar projects seeking FiT in 2018 (as the 10 GW cap had already been exceeded in May 2018).

The May 2018 policy changes were not expected so soon by the developer community, and sent a clear message of the national government’s intentions. A byproduct of the May 2018 policy was to raise the profile of corporate offtakers, who seek to procure in the absence of subsidies.

More fundamental policy changes revolve around the upcoming RPS. The RPS could structurally alter the renewable energy market in China, and is expected to encapsulate a wider community of participants. BRC China has issued policy briefs on each successive new RPS policy draft during 2018. Ultimately, corporate renewable procurement is aligned with recent national policy developments, however the devil remains in the unpublished details.

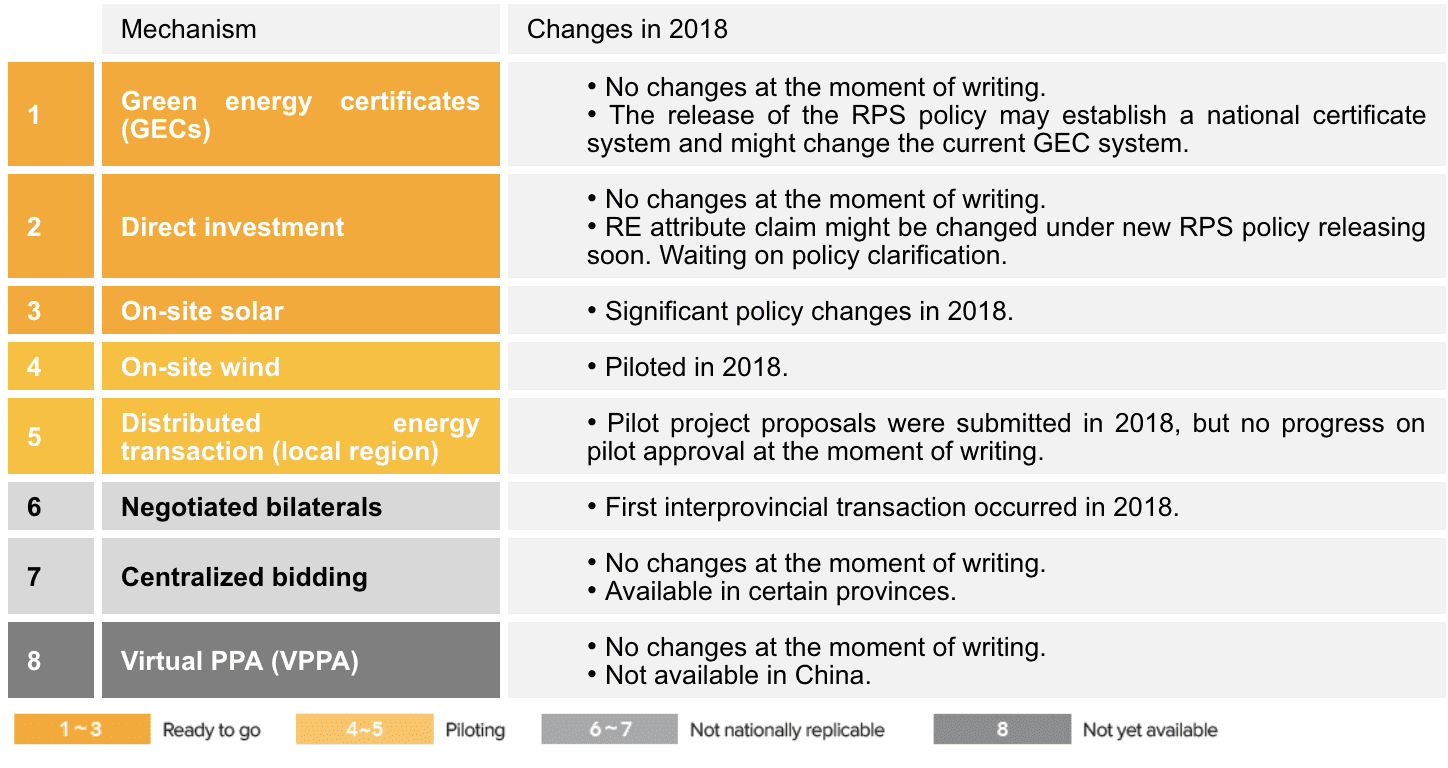

3. Mechanisms for corporate procurement are expanding through small-scale pilots, but significant work remains to enable large-scale transactions.

With policy changes impacting the renewable energy market, we have summarized changes in different procurement mechanisms which occurred during 2018 in the table below. Please refer to the 2017 State of the Market report for more details on specific mechanisms.

There were no major policy updates or changes in green energy certificates (GECs), direct investment, centralized bidding, or VPPAs. In summary:

- GECs remain the easiest option from an execution perspective, however, the high price and lack of additionality has made GECs an impractical solution for most corporations.

- Many curtailment provinces continuously hold centralized bidding to allow users to sign direct power purchase agreements with renewable projects, however, the ownership of environmental attributes is not differentiable.

- The ability to execute VPPAs relies on an active wholesale electricity market, which will require long-term power market reform.

New changes did occur relating to four procurement mechanisms:

- On-site solar: One consequence of the May 31 policy change was a sudden oversupply in the solar PV supply chain, which encouraged equipment price reductions and enhanced the economics of on-site solar.

- On-site wind: In April 2018, the NEA released guidelines on the development and construction of distributed wind to standardize project development and encourage business innovation through on-site wind.

- Distributed energy transactions (local region): In November 2017, the national government released policy guidance to encourage transactions at a local level, on a distributed system basis, and support local generation-consumption balance. About 35 projects filed pilot-project applications; however, project progress stagnated due to controversial pricing of the distribution network.

- Negotiated bilaterals: The first bilateral interprovincial transaction occurred in January 2018 between a metalware production company in Shandong and a wind developer in Shanxi. While very exciting, this mechanism has replicability challenges due to misaligned incentives between provinces and the complexity of government negotiations.

4. Looking ahead to 2019: Grid parity, on-site projects, and declining curtailment.

In 2019, we will see wind and solar developers responding to 2018’s market changes, and will reach grid parity, or zero-subsidy, projects. We also believe the RPS system will create new routes for buyers to meet their targets.

Reaching grid parity at the utility scale

For perspective, China installed over 50 GW of solar capacity in 2017, including 19 GW of distributed solar. The 10 GW annual cap for distributed solar capacity for 2018 created a significant oversupply of solar equipment, which is expected to force consolidation and sustain downward price pressure. Project developers know that to sustain development at scale, zero-subsidy-priced projects must become the norm. Industry experts indicated their view that the grid parity for wind and solar will be achieved in the coming several years. We expect the Chinese developer community to pivot at a typically fast pace.

Enhancing the on-site market

Previously mentioned cost reductions and significant electricity time-of-use (TOU) price differences between day and night periods will increase the attractiveness of on-site projects, especially when combined with storage. We already know of on-site projects not requiring subsidies being developed, and, based on interviews with different developers, market interests have indicated that new distributed renewable capacities will grow quickly in 2019 despite the policy-induced reduction in 2018.

The RPS era

The new RPS will come in effect in January 2019, impacting a plethora of previously quiet market actors at a provincial level. Many non-utility users, especially commercial and industrial users that have participated in direct power purchase transactions, will be forced to play a role in achieving provincial RPS targets. Policy wording will be key, at both the national and provincial levels. For example, allowing a mandated party to procure beyond the provincial RPS target would be an effective mechanism for corporates to meet their targets—providing environmental attribute tracking and retiring systems are sufficiently robust.

Distribution becomes sexy

The destiny of distributed energy transactions remains unknown, despite national policy encouragement. Without agreement on distribution wheeling fees and structure across existing distribution networks, these distributed energy transactions will not advance. It is possible that incremental distribution network expansion initiatives under power-market reforms deploy new distribution assets, and may potentially open new opportunity for the distributed energy pilot transactions. An increasing number of industrial zones and parks are expanding new distribution assets. They may be motivated to pilot distributed energy transactions to become the leader in low-carbon emissions by increasing renewable energy consumption.

National curtailment continues to decline and reduce sector CO2 emissions

Limited transmission capability between the west and east has been one major reason preventing curtailed renewables from being transmitted to the load centers. The government has approved construction of new high voltage transmission projects in 2019 to further expand interprovincial delivery of renewable energy.

BRC China will continue to follow the market and share relevant insights. As part of our ongoing community building, we will host our third annual workshop in 2019, to connect stakeholders for knowledge and experience sharing. We hope more stakeholders will increase the awareness of renewable energy procurement and corporates will actively explore their options to advance this nascent market. If you are interested in learning more about BRC China, our membership, or the upcoming annual meeting, please contact brcchina@rmi.org.

Authors

Jiayin Song

Tian Qiao

Caroline Zhu

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.