Catalyzing Change: The New Wave of Innovation in the Chemicals Sector

Why now is the moment for investing in the next frontier of chemical innovation, and how Third Derivative’s latest cohort of startups is leading the way.

The global chemicals industry is deeply embedded in our everyday lives. Across various industries, including healthcare, packaging, agriculture, textiles, automotive, construction, and more, approximately 96 percent of manufactured goods originate from chemicals industry products. This $4.7 trillion industry currently produces 719 million tons of products annually. That’s about the same weight as almost 2,000 Empire State Buildings being produced every year, and still, the chemicals industry is projected to expand production by up to 46 percent by 2050.

The sector stands at a crossroads; chemicals are not only essential for today’s products, but also for the technologies of the future. The outputs of chemical manufacturing support more than 75 percent of emissions reduction technologies, including ethylene vinyl acetate in solar panels, refrigerants in heat pumps, batteries in electric vehicles, and lubricants for wind turbines. However, it is also one of the world’s most emissions-intensive industries, responsible for approximately 4 percent of global greenhouse gas emissions. In addition to the climate impact, a growing body of research links the extraction and refining of petrochemicals with disproportionate rates of cancer, reproductive harms, respiratory ailments, and other public health crises in frontline communities around the world. The rising overconsumption of plastics, driven largely by single-use packaging and fast fashion, negatively affects human health and safety at both the global level and the individual level; plastics pollution amplifies the consequences of all nine planetary boundaries, and disruptive pollutants like microplastics and “forever chemicals” have been found from the middle of the arctic to the inside of the human brain.

Rapidly decoupling fossil fuels from the global chemicals sector is imperative to preventing the worst consequences of climate change and improving global human health. However, in the United States alone, over 50 percent of the emissions reductions needed in this sector depend on innovative technologies that are still in the early stages of development. The decisions made today will influence not only the trajectory of this sector but also every downstream industry reliant on chemical inputs for decades to come.

The chemicals sector faces a dual emissions challenge, as it is dependent on fossil fuels for both production feedstock and energy. This dependence makes reducing emissions complex but also opens the door to breakthroughs in circular feedstocks, electrified processes, and modular manufacturing. A tightening regulatory landscape (e.g., proposed EU restrictions on toxic substances and single-use plastics, the future inclusion of chemicals in the EU Cross Border Adjustment Mechanism [CBAM], and California’s extended producer responsibility law on plastics used in packaging) and global volatility for low-emissions feedstocks make it clear that early movers will gain a long-term competitive edge. This presents a rare window for high-impact investment and partnership; whether the goal is market leadership, climate impact, or resilience building, now is the time to act.

Today’s chemical innovation landscape

The chemicals innovation ecosystem remains undercapitalized relative to its climate impact potential. Over the past five years, only 3 percent of climate tech venture capital investment has gone towards chemicals and plastics. Similarly, defossilized chemicals and catalysts received approximately $7 billion in investment in 2022, which is only 3 percent of the global annual capital expenditure in the chemicals industry.

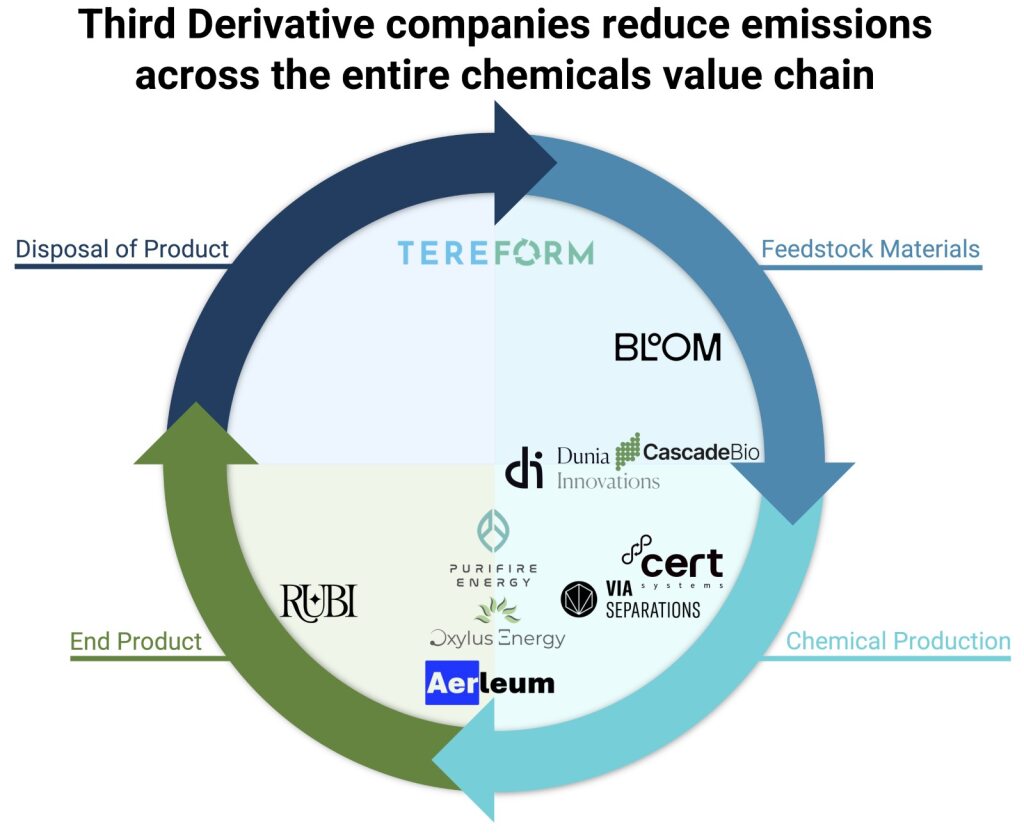

Reaching net-zero emissions in the chemicals sector requires innovation across the value chain. Third Derivative and RMI recently launched the inaugural Industrial Innovation Cohorts to support groundbreaking startups in the cement, steel, and chemicals sectors. Through the process of developing robust technical investment theses, the team categorized three types of innovation that are needed to reach net-zero emissions across heavy industry, including the chemicals sector:

- Make Less: Innovations to reduce demand for virgin feedstocks through materials substitution, recycling, upcycling, and increasing efficiency in supply chains and material use — in addition to non-technology efforts like reducing overconsumption and overproduction.

- Make Better: Reducing emissions in existing processes through direct electrification, materials feedstock innovations, and process efficiency.

- Make New: Disruptive technologies and novel processes to fundamentally change how materials are produced, with low or zero emissions from the start.

Make Less: Scaling the circular economy

Plastics circularity is a critical innovation frontier for reducing demand for virgin plastics and for mitigating emissions from products’ end-of-life. Startups in this space are advancing technologies such as molecular or chemical recycling (e.g., depolymerization), bio-based polymers, lignocellulosic fibers as substitutes for fossil fuel-derived thermoplastics, and reusable packaging. These innovations aim to displace virgin fossil-based plastics and reduce waste-related pollution, aligning with rising consumer and regulatory pressures. The current technology readiness levels of bio-based thermoplastic substitutes and chemical recycling technologies, such as depolymerization and solvent extraction, range from lab to demonstration scale.

Despite their promise, these solutions face challenges such as high capital costs for scaling new feedstock aggregation infrastructure, feedstock contamination that impacts the feasibility of chemical recycling and bio-based production, and the performance gap between mechanical recycling-derived plastics and traditional plastics. Tereform is tackling some of these challenges with a proprietary chemical recycling process, which uses oxygen and bio-based solvents to break down complex, contaminated streams of synthetic textile waste into pure monomers. Durability and material performance are key metrics for customers, so chemical recycling solutions like these that return materials to monomers and preserve the quality of plastics are gaining traction.

Additional opportunities for innovation include upstream design for reuse and infrastructure for local recycling, with a focus on modular systems and digital traceability for recycled content. Other upstream solutions, such as building infrastructure to aggregate, sort, and clean feedstocks, can be critical enablers of circular technologies.

Make Better: Improving existing processes

Process and energy efficiency innovations are key to addressing today’s highly energy-intensive production methods. For example, Third Derivative analysis shows that 90 percent to 95 percent of liquid separation operations for petrochemicals are carried out using thermal-based distillation technology, which represents 40 percent of the energy used in a typical chemical plant. Via Separations is reducing energy use through membrane separation as an alternative to distillation. Via’s electrified filtration process uses a graphene oxide membrane to deliver up to 90 percent energy savings. Further high-impact opportunities in this area include retrofitting incumbent systems or high-temperature batch processes, both of which have significant emissions reduction potential.

Incumbent producers are already deploying many existing energy efficiency technologies, with $3.4 billion invested in efficiency in 2022. Newer innovations such as heat pumps, thermal battery storage, electrified steam cracking, membrane-based separations, low-temperature distillation, and artificial intelligence and machine learning (AI/ML) for process optimization also offer compelling economics, with some solutions showing internal rates of return above 10 percent. In many cases, these technologies can be retrofitted into existing chemical production facilities. Incumbents and original equipment manufacturers are leading the charge in developing efficiency solutions by partnering with national labs for research innovation. For example, Lawrence Livermore National Laboratory partnered with incumbent TotalEnergies and the startup Twelve in 2022 to develop a new catalyst that improves the energy efficiency of electrochemical ethylene production by 15 percent.

The key challenge for many of these solutions is access to low-cost and reliable clean energy, which can be partially mitigated by securing long-term power purchase agreements or co-locating new facilities with renewable energy installations. Some solutions, such as membrane technologies or electric steam crackers, can be bottlenecked by lengthy capital planning cycles despite compelling returns, as extensive retrofits in existing facilities often require aligning the installation with planned shutdowns. Modular retrofit solutions and as-a-service business models can help chemical plants deploy new technology with lower capital expenses and shorter deal cycles.

Make New: Reimagining the future

At the heart of decoupling the chemicals sector from fossil fuels lies innovations in defossilized chemical production, meaning production that does not rely on fossil fuels for feedstocks or energy. This includes replacing fossil-derived feedstocks with low-emission sources of carbon, biomass, and green hydrogen, as well as new reactor designs and novel catalyst development. Technologies such as electrochemical and thermochemical CO₂ conversion and bio-based platform chemicals offer a radical rethinking of the chemicals value chain by transforming captured climate pollution into valuable chemical feedstocks. In the near term, methanol-to-olefins is a promising and lower-risk opportunity for defossilized chemical production. This technology is currently available at a commercial scale utilizing fossil fuel-derived methanol. Emerging green methanol can serve as a drop-in replacement for fossil sources, significantly reducing the emissions of the end product.

Carbon conversion technologies are gaining significant traction in the pursuit of defossilized chemical production. Oxylus Energy, PuriFire Energy, and Aerleum are producing e-methanol and other chemicals from CO₂, water, and renewable electricity. CERT Systems is initially targeting plastics with a single-step CO₂-to-ethylene process. Rubi Laboratories is utilizing enzymes to convert captured carbon into pure cellulose pulp, which is then spun into textiles using existing methods, thereby reducing emissions in the fashion industry.

Bloom Biorenewables is taking a different approach to carbon conversion. Rather than working directly with the greenhouse gas, Bloom’s assisted aldehyde fractionation process converts biomass (which naturally sequesters CO₂ during its lifespan) into cellulose, hemicellulose, and lignin. These feedstocks can be utilized in a variety of applications across cosmetics, plastics, adhesives, and more.

Novel catalyst solutions to improve reactions are another key innovation area for defossilized chemicals. Cascade Bio offers a coating to stabilize enzymes for industrial biocatalysis, increasing productivity and reducing costs through their cell-free approach. Dunia Innovations is accelerating R&D for new materials and catalysts with AI- and robotics-powered platforms, which enable a fully autonomous laboratory to run continuous electrochemical experiments for novel catalyst discovery.

Defossilized chemical production holds the highest potential for emissions reduction compared to conventional pathways, with the possibility of achieving near-zero emissions. However, progress is constrained by limited feedstock availability, lack of existing infrastructure, long commercialization timelines, and the high total cost of ownership (often four to six times higher than that of incumbents on a dollar-per-ton basis, largely due to the cost of electricity. Driving down the cost of electricity, via electrolyzer efficiency and access to cheaper renewable power, will be integral to scaling these technologies. Modular, decentralized systems that can co-locate with feedstock sources, such as the modular electrochemistry reactors developed by Mattiq, address this need.

While defossilized production is the most active innovation space in the chemicals sector, significant systemic gaps still exist in intermediates like aromatics and the enabling infrastructure for feedstock transport and aggregation.

In addition to the technologies in these three categories, several types of cross-cutting enablers can accelerate commercial deployment and de-risk investment in chemicals innovations. Digital solutions like AI/ML can accelerate catalyst discovery, optimize reactor designs, simulate new chemical reactions, and enable predictive maintenance to improve equipment reliability. Some companies are pursuing flexible business models that include both one-time equipment sales, which have higher upfront costs to the customer, and as-a-service offerings, which spread costs over time, to expand their commercial pipeline to meet a variety of customer preferences. Across the entire innovation landscape, certifications for low-carbon products help customers validate sustainability claims and, in some cases, pursue incentives designed to drive market adoption.

Industrial innovation insights

Through the process of sourcing, conducting diligence on, and onboarding this cohort of startups, Third Derivative identified several common commercialization challenges across the innovation landscape that startups are addressing creatively.

Customer willingness to pay varies: Consumer brands tend to show more flexibility on green premiums, while commodity buyers remain cost sensitive. In industries like textiles and cosmetics, environmentally conscious luxury brands have the margin to pay a premium to help startups scale production while gaining early access to low-carbon products. This has proven vital to bringing new technologies down the cost curve, enabling them to break into the commodity market. For example, Patagonia and Reformation are apparel brands that have strong sustainability platforms; these first movers are helping to commercialize Rubi Laboratories’ CO₂-derived textiles.

With commercial agreements, startups can face “the chicken or the egg” dilemma: Customers and investors require de-risked technology, but de-risking requires commercial traction. Some startups are navigating these dynamics through creative options, such as prepurchase agreements to guarantee revenue, as-a-service business models to reduce capital expenses and shorten deal cycles, and joint venture production models to reduce capital burden, share risk, and gain credibility by partnering with incumbents. For example, Hexion, a global leader in adhesives, is partnering with Bloom Biorenewables to commercialize Bloom’s renewable bio-adhesive.

Access to long-term contracts for feedstocks and product offtake is a bottleneck: Key renewable inputs such as carbon, hydrogen, and biomass are currently supply-constrained and expensive (e.g., the cost of clean hydrogen is around $6.50/kg today, which is two to three times more expensive than fossil-derived hydrogen, but is expected to come down to about $2.30/kg by 2050). Securing long-term offtake agreements for end products is seen as essential to de-risk business models and attract additional capital. While policy levers can incentivize long-term contracts through regulations, subsidies, and tax incentives, there is currently uncertainty around much of the US federal policy infrastructure. Startups that were previously pursuing federal US incentives are now exploring alternative non-dilutive funding sources, such as state-level incentives, the EU Innovation Fund, or Canada’s Clean Growth Hub.

Climate investing is down, and heavy industry is feeling the impact: After record-shattering investment levels in 2023, global investment in clean industry fell nearly 60 percent in 2024. Amid a challenging fundraising climate, non-dilutive capital has proven critical to advancing research and development, deploying pilots, and unlocking commercial traction. Philanthropic capital and government grants can fill crucial gaps for early-stage technologies where risk is high, but impact potential is significant, enabling follow-on funding from the private sector. For example, the Colorado Office of Economic Development & International Trade awarded a catalytic grant to Tereform through its Advanced Industries Accelerator Program. That same office offers an Advanced Industries Investment Tax Credit to incentivize follow-on investments in Colorado advanced industries businesses, thereby increasing the impact of the awarded grant funding.

Investing in innovation

To unlock the next wave of climate-aligned innovation in the chemicals sector, investors and corporations must take a proactive and strategic approach. Founders need partners with extensive networks who understand the complexity of scaling hard tech in an incumbent-driven sector to help bring breakthrough solutions to market. Several key considerations can help startups optimize their value proposition and enable investors and corporates to increase their impact.

Certifications from reputable standards bodies such as ISO, SCS, and ISCC build credibility: Low-carbon product certifications are increasingly vital for validating emissions reductions, enabling access to premium markets, and securing offtake agreements, particularly in chemical markets with strict procurement standards or evolving regulatory mandates (e.g:, varying regulations across states in the United States on restricted dyes and chemical additives in textile manufacturing). However, conducting in-depth life cycle analyses to obtain these certifications requires time, money, and expertise that many startups lack in-house. Providing startups with dedicated funding for these efforts and connecting them with technical experts can accelerate certification.

Regional adaptability is vital: Startups are developing localized strategies that match or can adapt to feedstock availability, policy environments, and infrastructure readiness. Technologies with clear demand signals for low-emission chemical products and a path to commercialization that aligns with regulatory shifts (e.g., CBAM in the EU) are well-positioned to scale. Rapidly growing economies and industries in Asia and the Middle East provide immense market opportunities in the coming decades. Many countries in these regions have both strong net-zero commitments and established or emerging carbon pricing and/or emissions trading schemes, making them particularly well suited to support homegrown innovation and serve as a landing spot for US companies seeking more favorable markets.

Strategic partnerships with incumbents are a critical accelerator: Startups benefit from access to existing infrastructure and operational expertise, while incumbents can experiment with new solutions without the time and expense of launching or expanding an in-house research and development team. The venture capital arms of large corporations can play a key role in facilitating joint development agreements or pilot programs at production plants, helping startups meet critical technical validation milestones. Early adoption of new technologies allows incumbents to future-proof themselves, enabling them to remain competitive in new markets and shifting regulatory landscapes.

Investing in early-stage climate tech startups can unlock transformative impact in the chemicals sector. Catalytic capital and strategic partnerships can shape not only individual technologies but also the broader trajectory of industrial decarbonization. With the chemicals industry’s projected growth, investors, corporates, and startups have the opportunity to accelerate systemic change and build a sustainable and profitable future together.

References

https://www.systemiq.earth/wp-content/uploads/2022/09/Main-report-v1.20-2.pdf

$80B Ammonia market size, 2023: https://www.statista.com/statistics/1391399/global-ammonia-market-size/

$37B Methanol market size, 2021: https://www.statista.com/statistics/1350272/methanol-global-market-size/

$240B Olefins market size, 2022: https://www.zionmarketresearch.com/report/olefins-market

$212B Aromatics market size, 2023: https://www.verifiedmarketreports.com/product/aromatic-compounds-market/

The authors wish to thank The Lemelson Foundation for funding the Industrial Innovation Cohorts. The authors also wish to thank Brianne Cangelose, David Hynek, and Ali Rotatori for their contributions to this article.

Accelerating the Future of Chemicals Together

Momentum is building in the chemicals sector, and Third Derivative and RMI are supporting a curated pipeline of startups tackling some of the toughest climate challenges. Now is the moment to engage by investing capital, sharing expertise, or forming partnerships that bring these solutions to market. If you are interested in joining Third Derivative’s network of investors, mentors, and corporate partners to help advance industrial innovation, we welcome you to reach out here.