The Energy Transition in 2025: What to Watch For

Progress powered on in 2024. What does that mean for the year ahead?

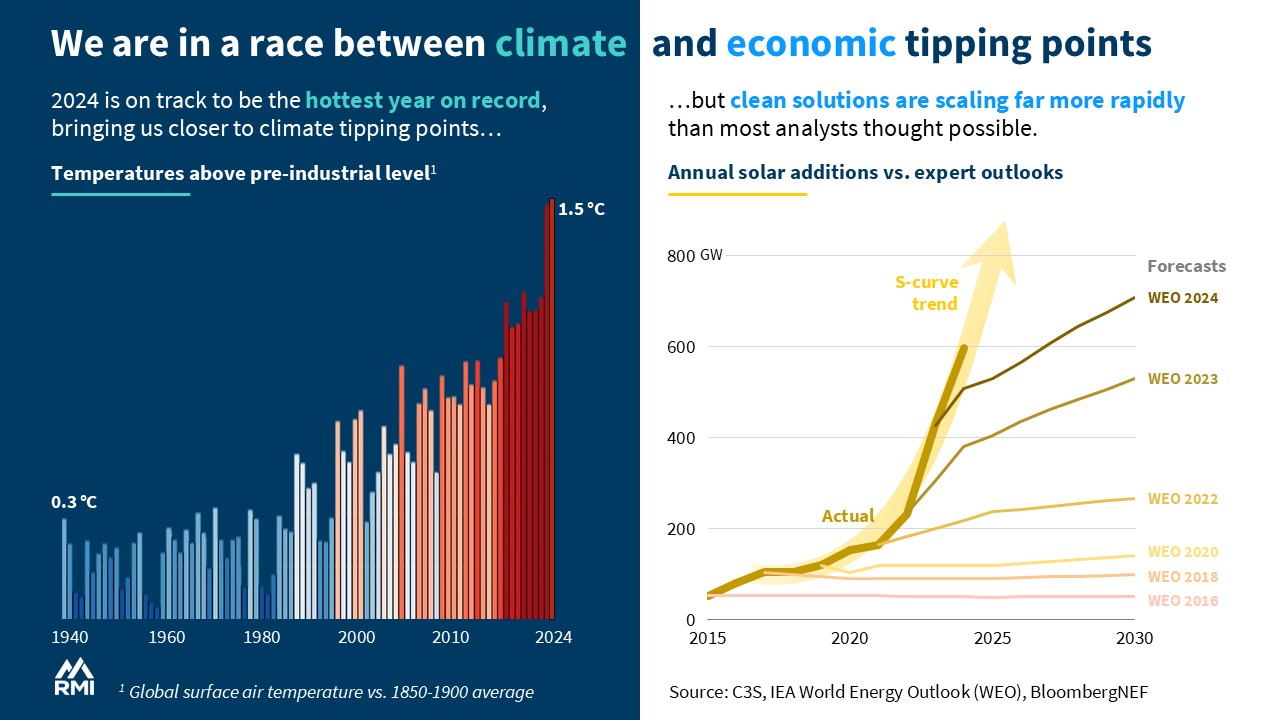

As we enter a new year, the race between tipping points is clearer than ever. 2024 was likely the hottest year on record, raising the risk of earth system tipping points if we fail to speed up solutions.

But despite warnings of a slowdown, solutions continue to race forward. As cleantech becomes cheaper than ever, 2024 saw record uptake in renewable energy, electric vehicles (EVs), and more. These positive tipping points are happening worldwide — with major progress in China and the Global South. Let’s review what that means for the year ahead.

- Costs falling fast. Solar module prices fell 35 percent to 9 cents per watt; EV batteries are now below $100/kWh and often at cost parity with their fossil-fueled competition.

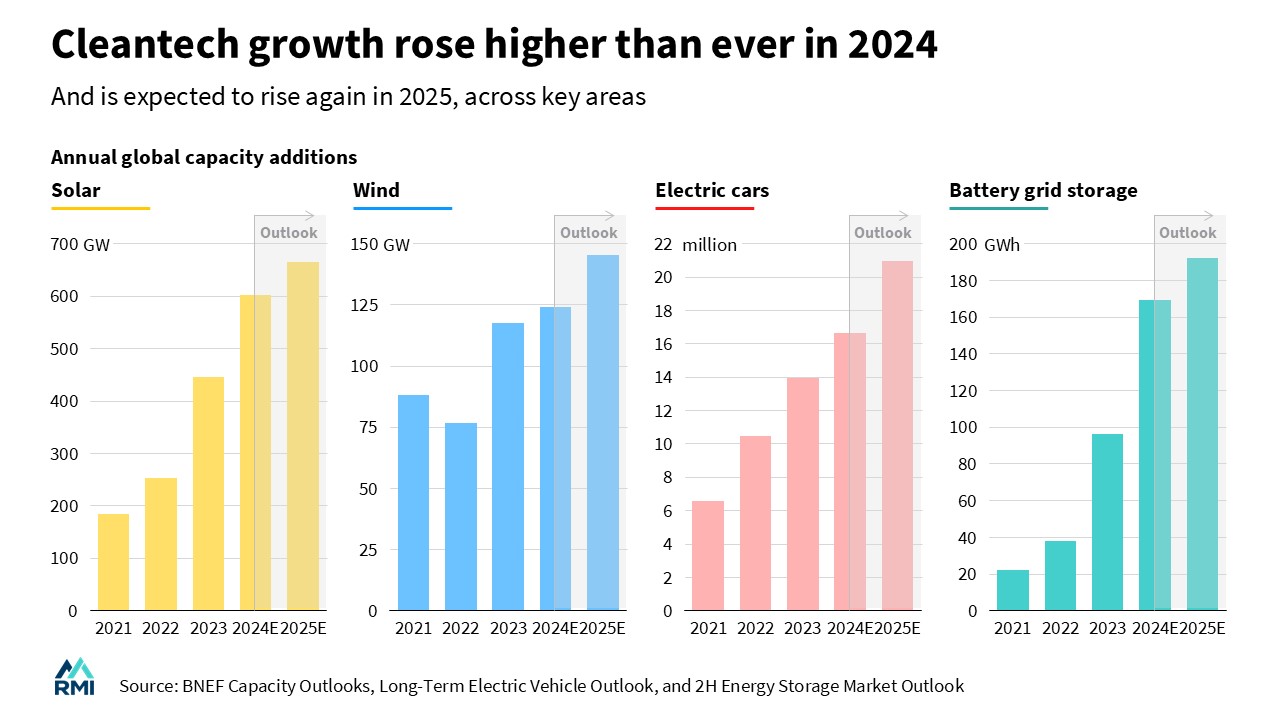

- Cleantech growing globally. Solar additions grew to 600 GW, EV sales climbed 25 percent, and battery storage additions nearly doubled.

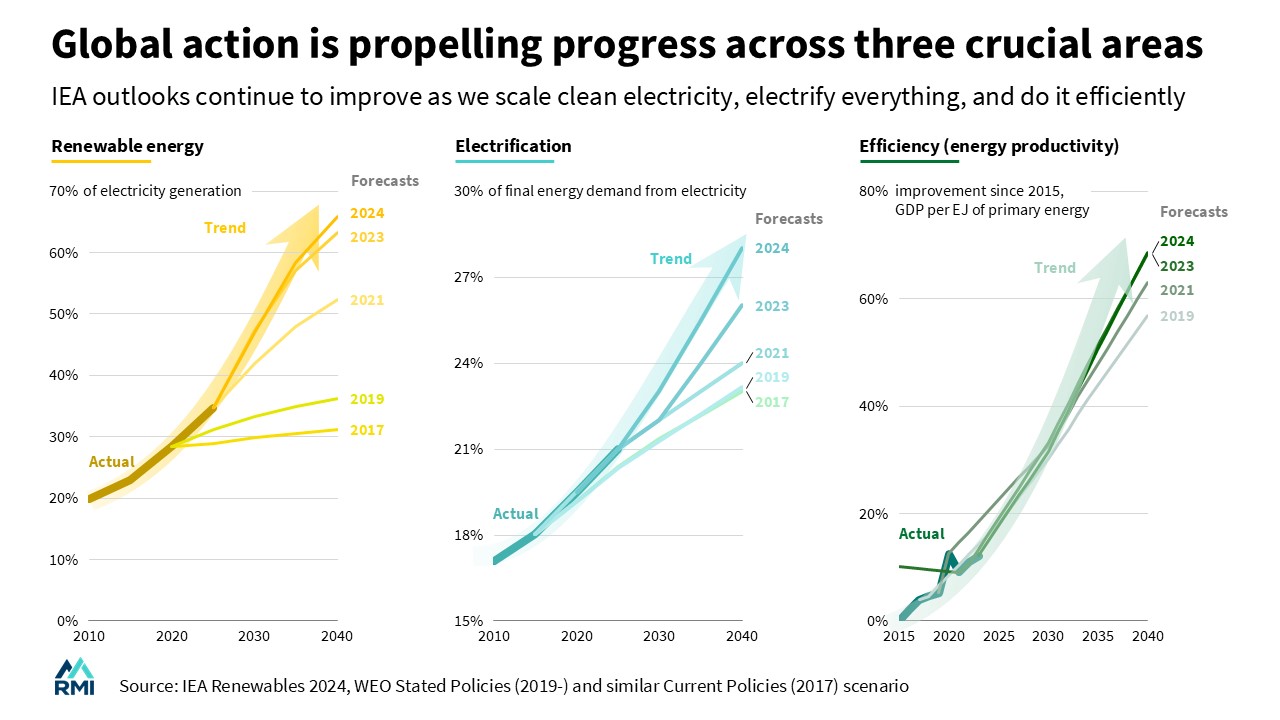

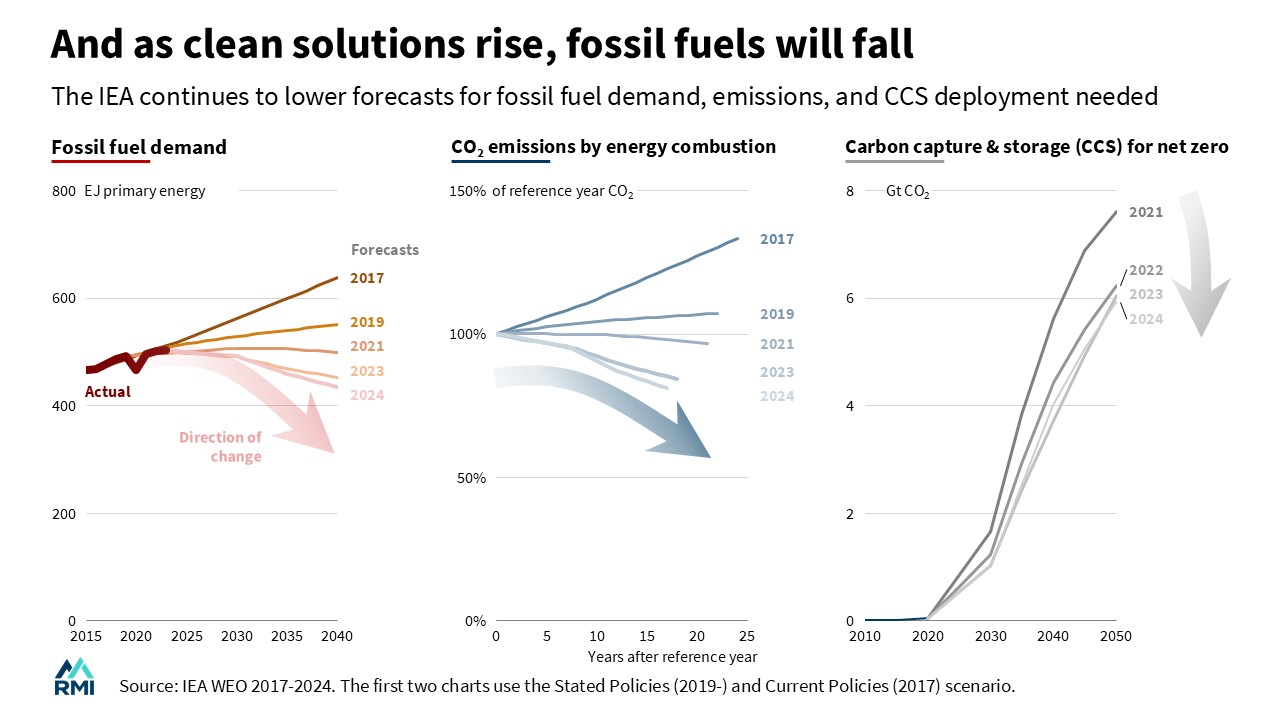

- Changing perception. IEA forecasts have improved for cleantech and fallen for fossil fuels several years in a row.

- New year, new progress? Energy efficiency and methane are the two fastest ways to cut warming, but also the two furthest off track.

- From ambition to action. With national climate plans due in February, it is time to include all sectors, pollutants, and solutions — and then hit the ground running.

With falling costs, be ready for a cleantech revolution

After 2024, clean energy is cheaper than ever. Global solar module prices fell 35 percent to less than 9 cents/kWh. EV batteries saw their best price decline in seven years, dropping ~30–50 percent for cathodes and 20 percent for the full battery to below $100/kWh. EVs are now at cost-of-ownership parity in the United States and purchase price parity in China — with that milestone expected around now for Europe, in 2026 for the United States, and in 2027 for India’s two- and four-wheelers.

Thankfully, lower cost does not mean lower quality. Take batteries: the average cell in 2024 used less than half as much nickel and cobalt as a decade ago, and new technologies could double energy densities in the next five years. As we see improving safety, charge time, and longevity, uptake will follow and drive down cost in a virtuous cycle.

Adoption is going global

Cleantech uptake is more widespread than ever. Renewable energy additions grew 17 percent with a record ~600 GW of solar, ~125 GW of wind, and near-doubling of grid storage installations to ~170 GWh in 2024. Renewables now outpace fossil electricity investment by 10 to 1, with more investment in solar than all other power sources combined. As a result, renewables are poised to overtake coal as the leading power source in 2025.

This progress is truly global. As a share of electricity, solar and wind is scaling twice as fast in the Global South as in the Global North. Countries like Pakistan and Namibia have used Chinese solar exports to nearly double their total electricity capacity in just two years.

Meanwhile, EV growth rose 25 percent (and faster for trucks), with more than 16 million vehicles sold in 2024 — driven by China, which has electrified more than half of its new cars since July. Last year started with unfounded fears of a major EV sales drop — but this is the cycle every year, as all car sales tend to be lower in Q1. Naysayers may point to a similar drop in Q1 2025, but the expected annual growth is larger than ever.

Advancing policy from pledges to progress

New national pledges can accelerate change. Led by the EU, countries on five continents redoubled their commitments to a 1.5oC-aligned emissions path, while the UK pledged an 81 percent reduction by 2035 and Mexico committed to net zero by 2050. All G20 nations now have net-zero goals that could help limit warming to well below 2oC, if realized.

Governments are also taking direct action to transition away from fossil fuels. Indonesia has announced plans to switch fully to renewables in the next 15 years — retiring all coal, oil, and gas power plants despite coal’s current dominance. And Ethiopia became the first nation to ban imports of non-electric cars, citing efforts to clean the air and save billions of dollars in annual oil imports.

Next year will be crucial. With national climate plans due in February, it is a key opportunity to include all sectors, pollutants, and solutions like energy efficiency. Then, the focus turns to implementation — including for nature, with the next UN climate conference in Brazil.

Global outlooks get more bullish

Are we doing enough to meet the 2030 targets? It depends — but, based on the latest trends, progress-as-usual would meet the 2023 goal to triple renewable energy capacity, as well as the 2024 goal for a six-fold increase in grid energy storage. And from vehicles to heat pumps to industry, annual electrification progress doubled in the past year — a key step for the energy efficiency pledge and its many benefits.

Fossil fuel emissions appeared to rise 0.8 percent to 37.4 GtCO2 in 2024, but multiple analyses show that they may well peak and decline in 2025. Half the world or more has passed peak demand for residential gas and gasoline, and more than half of countries are 5+ years past the peak for fossil electricity.

As a result, leading outlooks such as the International Energy Agency (IEA) have once again raised their forecasts for renewable energy and electrification, while lowering their forecasts for fossil fuels, emissions, and carbon capture. Time will tell if they do the same in 2025.

New year, new avenues for progress?

But we can do much more. According to the IEA, we can triple the rate of progress if we fully implement recent global pledges. Efficiency and methane are the two fastest ways to cut warming, but also the two furthest off track. And scaling finance remains a global challenge.

After agreeing to double energy efficiency progress, the rate of primary energy intensity improvement got halved from ~2 percent in 2022 to 1 percent in 2023. Improving this will save trillions of dollars while helping to manage electricity load growth — from data centers to the air conditioners that could otherwise cause much more demand.

Meanwhile, methane continues to gain attention as non-negotiable. But despite the year’s satellite launches and organic waste commitments, pollution levels are rising twice as fast as predicted. Along with new campaigns on nitrous oxide and tropospheric ozone, 2024 has shown the importance of super-pollutants that drive half of current warming. Measuring alone is not enough; we need to act.

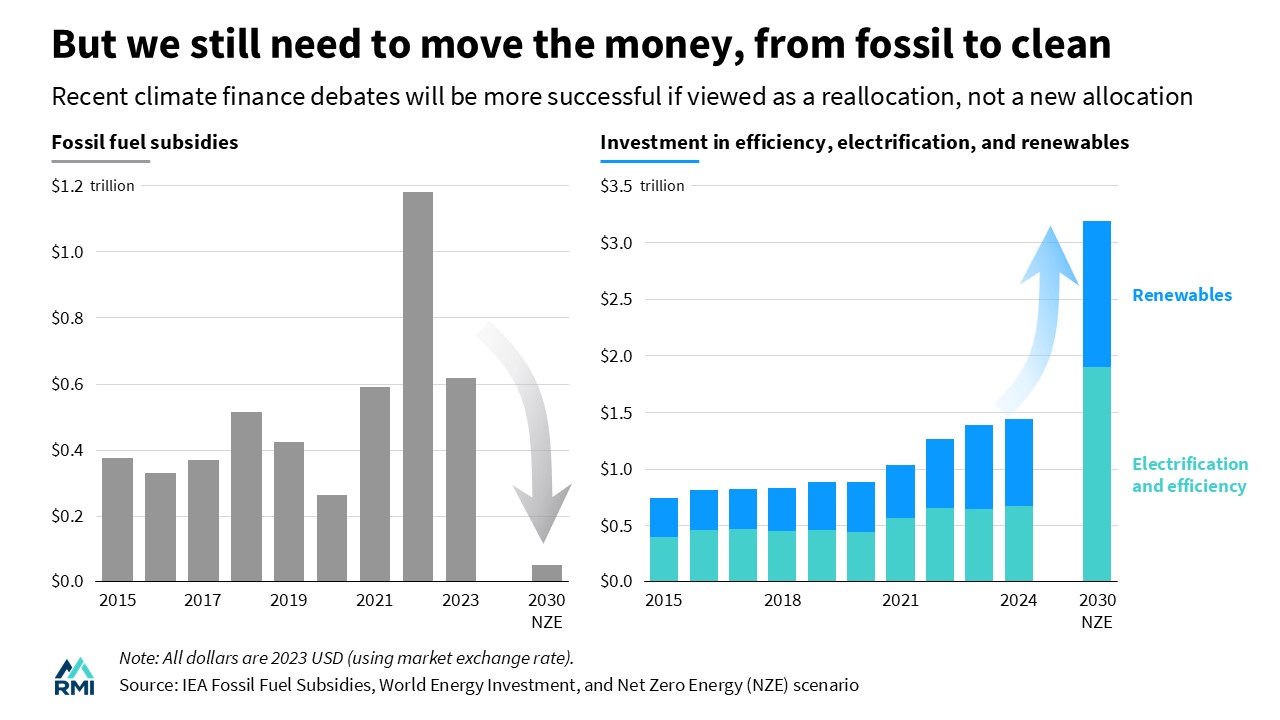

Can we move faster in 2025? Moving fast means moving the money — a bitter fight at the past UN climate conference. But RMI has shown that investment goals are achievable if viewed as a reallocation from fossil to clean. For example, governments spent 10 times more on fossil fuel subsidies than clean energy support in 2023. Shifting that near-trillion into clean solutions will help fill investment gaps from efficiency to grids to forest protection — especially in emerging economies.

A pivotal moment

Halfway through this decisive decade, such change cannot come fast enough. The months ahead are full of uncertainty, but the energy transition has thankfully come a long way.

In the US, we now have 10x more EVs on the road, nearly twice as many heat pumps, and 100x as much battery storage capacity as in 2016. Approved corporate commitments have multiplied from 32 to ~5,000 globally, while national net-zero goals have spread from 2 percent to 90 percent of the world.

The time is now for leaders and locals around the world to see these signs of progress — and hit the ground running in the new year.