Learn how we are working to transform how we use and produce energy.

Planners Have Tools to Manage Large Load Forecast Uncertainty. Are They Working?

While data centers’ unprecedented scale, speed, and uncertainty present undeniable challenges for the grid, power sector decision makers are already using tools to manage them.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Data center demand has quickly become one of the most consequential uncertainties facing electricity system planners. After decades of low growth, utility forecasts now estimate national peak load could grow sixfold to 166 GW by 2030 — equivalent to adding 15 times the peak load of New York City. If these forecasts are correct, the industry would need to build new generation and transmission at more than six times the pace seen in recent years.

At the same time, electricity prices are rising, raising the stakes for getting the timing and scale of these investments right. Underforecasting and underbuilding can lead to missed economic opportunities, while overforecasting and overbuilding can lead to unnecessary infrastructure, stranded costs, and higher electricity rates. Grid planners at utilities, public service commissions, and regional transmission organizations (RTOs) are now challenged with creating credible forecasts that guide infrastructure investments without exposing ratepayers to unnecessary costs.

Fortunately, tools for making sense of large load forecasts are emerging. We published a guide to forecasting large loads last year. And, earlier this year, the National Association of Regulatory Utility Commissioners (NARUC) released a framework outlining several actions regulators can take to reduce forecast uncertainty, including strengthening large load tariffs provisions, building forecasts from tariff provisions, and back-testing forecasts against observed outcomes.

Over the past 18 months, grid planners and regulators have started to put these tools into practice. Evaluating how their load forecasts have changed can shed light on these tools’ ability to manage large load uncertainty.

Exhibit 1

The scale of uncertainty

Grid planners are getting conflicting signals about the pace of data center load growth. A growing body of analysis based on metrics like processing chip supply and AI workloads suggests current forecasts may be overestimating data center demand. For instance, Grid Strategies estimates that utility forecasts may overstate national data center load growth by 25 GW by 2030. This discrepancy is even more pronounced in the near term: A May 2026 analysis from JP Morgan found that more than 60% of data center capacity originally planned for completion in 2027 isn’t yet under construction, corroborating findings from Sightline Climate’s Data Center Outlook, which tracked 190 GW across 777 data center projects and estimated that up to half of data center projects expected online by 2026 may not materialize by the end of the year.

At the same time, data center operators continue to increase capital expenditure plans, signaling expectations for significant computing demand. And, where utilities regularly report the status of data center projects in their territories, cumulative requests and attendant demand continue to grow. Taken together, these trends indicate that while current load forecasts may not be firm, the long-term trajectory of data center demand remains highly uncertain — and getting load forecasts right is critical to delivering affordable, reliable power for ratepayers.

Georgia Power Company’s large load economic development pipeline highlights the scale of uncertainty that planners must contend with. As of May 2026, the maximum potential 2032 demand from large loads in its pipeline exceeds 68 GW — roughly four times the utility’s historic whole-system peak demand (Exhibit 2). Yet, more than 60 GW, over 80% of the pipeline, remains in early “technical review” stages, without binding contractual or financial commitments. At this stage, projects are not committed to take electric service from the Company, and may also be negotiating with other utilities. If all projects in the pipeline materialize, large load growth could exceed 11 GW per year over the next five years. By comparison, the Company served only 100 MW of large load projects annually before 2021.

Exhibit 2

The scale of uncertainty, speed of onset, and total size of Georgia Power Company’s large load pipeline illustrate the challenges of forecasting large, speculative loads. Planners must develop forecasts that drive long-term infrastructure investments based on sparse historical precedent and limited customer-provided information. And, because data center developers generally do not disclose the status of alternative site plans, regulators and utility planners must manage the risk of planning for loads that may be committed elsewhere.

We outline three tools from NARUC’s framework for reducing large load uncertainty below, and show real-world examples of where these tools are already reducing uncertainty for planners.

Strong tariff provisions screen speculative load

First, regulators and utilities across the country are increasingly adopting large load tariffs to increase the level of commitment behind proposed large load projects and minimize stranded asset risks. These tariffs commonly include provisions, such as special contracts, rates, and service agreements between utilities and large-load customers. They can also involve financial requirements, such as interconnection study fees, minimum monthly billing demands, contributions in aid of construction, or exit fees.

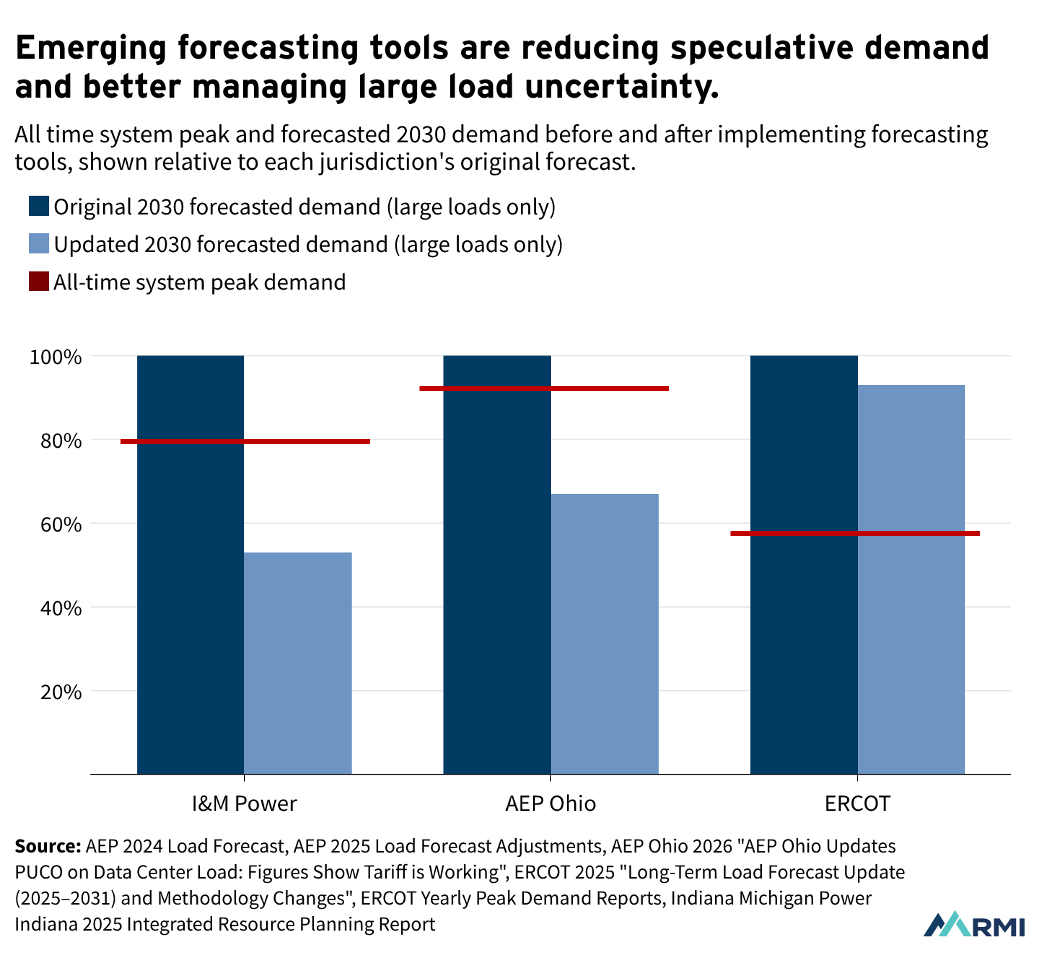

Increasingly, large load tariffs are designed to encourage data center developers to advance projects with stronger commitments and withdraw those that are more speculative or duplicative. Tariff provisions that encourage commitment yield a pipeline of large load projects — and ultimately a system-wide demand forecast — that more accurately reflects realistic timelines, reliable revenue, and committed load. For example, following the implementation of new tariffs for their large load customers, system-wide forecasted 2030 demand declined by roughly one-third in AEO Ohio and by about half in Indiana Michigan Power (Exhibit 3). Importantly, the projected 2030 remains substantial: 3.2 GW in Indiana Michigan Power (66% of its historic peak demand) and 7.6 GW in AEP Ohio (73% of historic peak demand). AEP Ohio and Indiana Michigan Power’s experiences suggest that tariff provisions that encourage large load commitment can preserve economic development while firming up short-term demand forecasts.

Exhibit 3

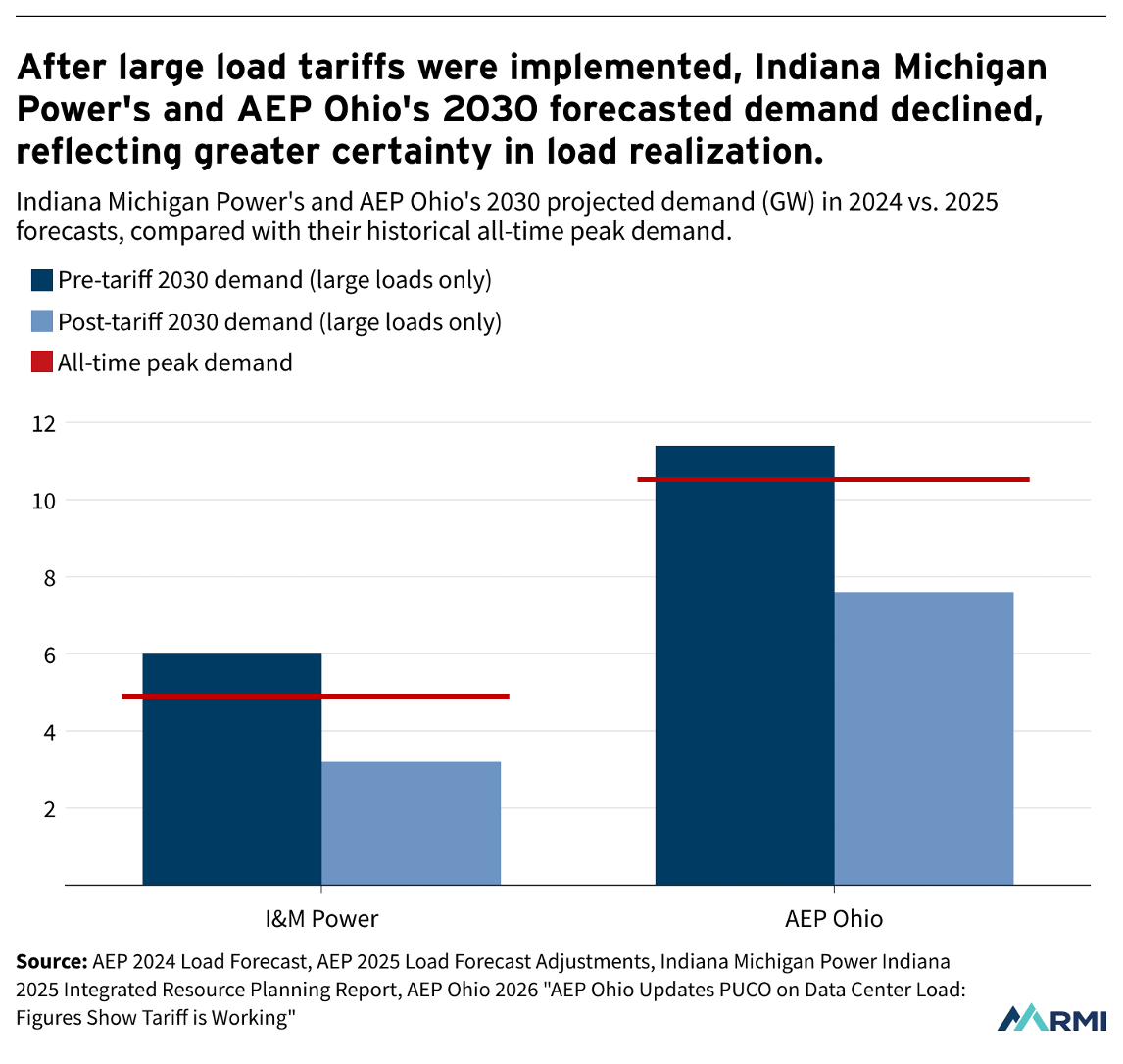

Let’s look at each of these tariffs in detail. The Public Utilities Commission of Ohio approved a Data Center Tariff for AEP Ohio in 2025 that required developers to demonstrate financial viability, pay nonrefundable study fees, and face exit fees if they fail to meet contractual obligations. Prior to the tariff, data centers or developers had requested 30 GW of load — nearly three times AEP Ohio’s typical peak demand of 10.5 GW. Under the tariff, only 5.6 GW of new data center contracts were signed, adding to the 12.2 GW already under contract, for a total of 17.8 GW of contracted data center projects expected to come online through 2035. This contracted pipeline represents a significant opportunity for economic development while helping ensure that infrastructure investments are aligned with committed projects rather than speculative requests.

Similarly, the 2025 large load tariff settlement for Indiana Michigan Power included provisions such as long-term financial commitments and Commission approval for any reductions in contracted capacity. These tariff requirements helped screen out speculative projects and encouraged developers to only commit to viable loads, resulting in smaller but more credible project pipelines that reduce risk of overbuilding infrastructure while preserving opportunities for economic development.

Well-designed forecasts leverage tariff provisions

Second, planners can build large load tariff provisions directly into how they forecast future demand. While the previous example showed that effective large load tariffs can filter out speculative projects, other tariff provisions provide valuable details for when and how large loads will appear.

How these tariffs are folded into future demand forecasts depends on the forecast’s purpose — whether it is conducted at the utility or regional level, intended for resource planning or market auctions, and focused on near- or long-term horizons. Given data center construction timelines and the importance of aligning near-term energy supply and demand, forecasts could apply stricter inclusion criteria by excluding or discounting early-stage projects with limited commitments while assigning greater confidence to more advanced projects.

For example, PJM’s Load Adjustment, which was first implemented in the 2026 Long-Term Forecast, uses project commitments to establish criteria and derating factors that improve near-term forecast certainty. In particular, projects expected online within three years must demonstrate firm commitments, such as an Electric Service Obligations or construction commitments. Meanwhile, projects with later in-service dates must either demonstrate key development milestones, such as site control or financial commitments, or be subject to derating factors that reflect greater uncertainty.

Exhibit 4 shows NARUC’s framework for how specific tariff provisions, such as contractual and financial obligations, may be mapped to load forecast assumptions, scenarios, and sensitivities. By explicitly and transparently mapping their own tariffs to their application in load forecasts, grid planners can generate more credible expectations for future demand.

Exhibit 4

PJM provides a clear example of how key tariff provisions can reduce speculation. First implemented in the 2026 Long-Term Forecast, PJM’s Load Adjustment uses project commitments to establish inclusion criteria and derating factors that improve near-term forecast certainty. In particular, projects expected online within three years must demonstrate firm commitments, such as an Electric Service Obligations or construction commitments. Meanwhile, projects with later in-service dates must either demonstrate key development milestones, such as site control or financial commitments, or be subject to derating factors that reflect greater uncertainty.

Back-tested forecasts improve accuracy

Third, planners can refine their forecasts over time by back testing, comparing their previous forecasts against on-the-ground results. Over time, these insights can be used to periodically update forecasting methodologies and critical assumptions, such as project inclusion criteria and materialization probabilities.

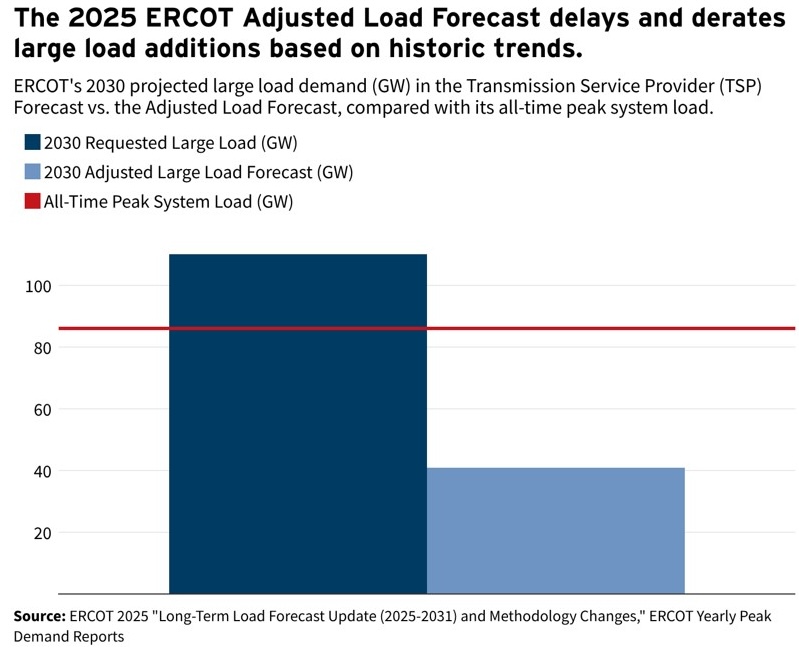

The Electric Reliability Council of Texas (ERCOT) provides an early example. It found that large loads with 2022–2024 in-service dates were delayed by about 220 days on average, and that data centers ultimately reached only about 50% of their requested load. In response, ERCOT’s 2025 Adjusted Load Forecast — which will inform transmission planning, resource adequacy, and outage coordination analyses — applies a 180-day delay to contracted loads and assumes only 50% of requested load will materialize on the grid. As a result, ERCOT’s 2030 Adjusted Load Forecast included only 37% of the total requested load in its 2030 forecast (Exhibit 5), reflecting a more evidence-based projection. These delay and derate assumptions will continue to be refined over time as additional projects come online and more performance data becomes available.

Exhibit 5

The emerging path for reducing uncertainty

Large load uncertainty is one of the most consequential challenges facing the power system today. However, tools for managing that uncertainty, from screening uncommitted projects to learning from the past, are emerging to manage it. Early evidence from the leading edge of data center growth suggests that these tools (implementing stronger tariff provisions, building forecasts from tariff provisions, and back-testing forecasts) can help planners develop forecasts that they can be more confident in and plan their grid accordingly.

Early adopters’ experiences point to several further actions that regulators and planners can take to make the most out of their large load forecasting tools:

- To effectively integrate tariff provisions and validate forecasts, planners can coordinate with large load developers to exchange transparent and regularly updated data about their projects. Some state legislators and regulators are already facilitating this transparency. For example, Georgia Power Company files public quarterly Large Load Economic Development Reports with the Georgia Public Service Commission, tracking announced load and contractual commitments as projects progress through the large load pipeline.

- Using large load project data, grid planners and external reviewers can coordinate and validate forecasts with neighboring jurisdictions to reduce the risk of double counting projects. For instance, Pennsylvania’s recent Load Forecast Accountability Act gives the public utility commission access to utility-customer contracts and promotes coordination with PJM and other state regulators to prevent the same project from being counted in multiple territories.

- Regulators and planners can also build in flexibility for evolving arrangements with load load customers. As flexible interconnection for data centers continues to mature, forecasters can integrate large load flexibility into demand forecasts and resource adequacy assessments.

- Finally, regulators and planners can periodically report on the accuracy of large load forecasts over time to support periodic improvements from back-testing and regulatory oversight.

While data centers’ unprecedented scale, speed, and uncertainty present real challenges for planning and operating the grid, power sector decision makers increasingly have the tools to manage them. When used wisely, tools like tariff provisions, commitment screens, and forecast back testing can not only reduce risks to ratepayers today, but also present a clearer picture of the future. When used in coordination with grid planning stakeholders, these tools could build the more stable, reliable forecast that planners need to build the grid of the future.

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.