Learn how we are working to transform how we use and produce energy.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

India’s energy transition efforts have largely centered on renewable capacity addition and vehicle electrification. While these levers continue to be critically important, they will need complementary interventions to adequately address the decarbonization challenge, especially in hard-to-abate sectors such as refining, ammonia, steel, methanol, and some aspects of long-haul trucking. Green hydrogen (hydrogen produced from electrolysis powered with renewables) is one such intervention, where it can be either used as a feedstock or as an energy fuel in these sectors and promote rapid decarbonization.

Green hydrogen will play a critical role in India’s clean energy future due to three distinct characteristics. Firstly, India has the potential to become one of the cheapest producers of green hydrogen, owing to its abundant and low-cost renewable supply. This will enhance the domestic manufacturing market, industrial competitiveness, and economic growth in the nation. Secondly, adoption of green hydrogen can enable India to become energy independent and address its energy security concerns by cutting down natural gas and oil imports. Third, green hydrogen adoption will be crucial for India to reach its net-zero goal.

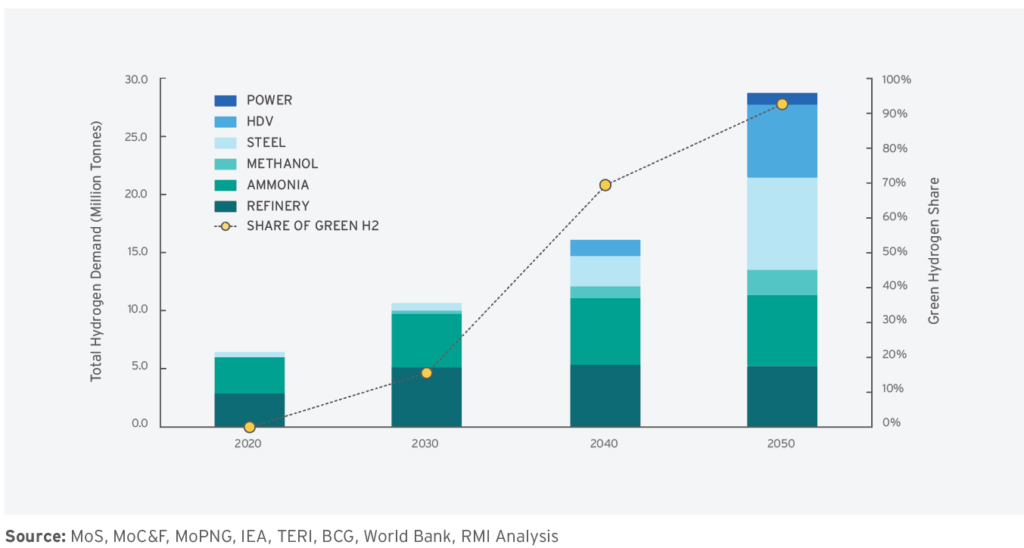

In recognition of these opportunities, India recently announced the Green Hydrogen Policy. Within this context, this report aspires to serve as one of the key knowledge bases. In this report, NITI Aayog and RMI have analyzed the opportunities that green hydrogen presents for India. Our analysis suggests that the total hydrogen demand will increase from 6 million tons in 2020 to around 29 million tons by 2050. 94 percent of this hydrogen demand in 2050 could be green. If these demand projections and the associated penetration of green hydrogen materialize, India will be able to abate 3.6 gigatons of CO2 and save $246 billion to $358 billion in energy imports cumulatively over the next three decades.

Exhibit 1: Hydrogen Demand Outlook and Potential Green Hydrogen Share

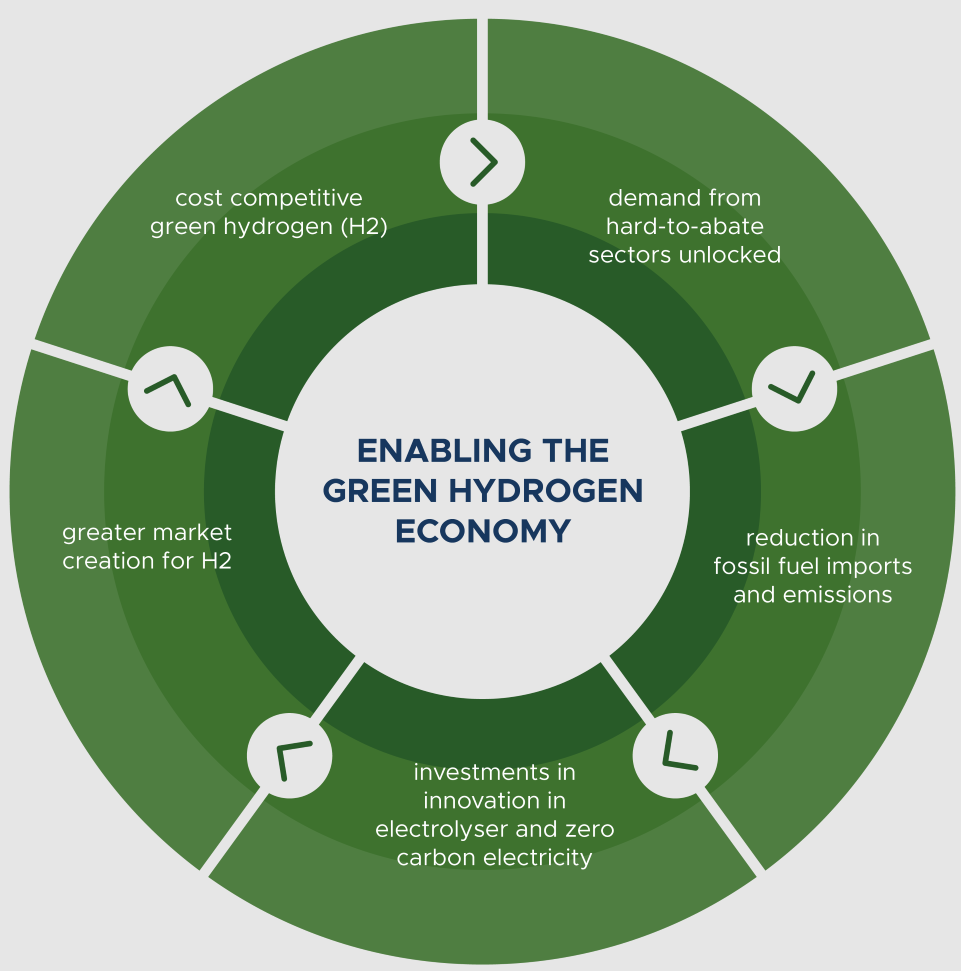

The report also highlights potential solution areas that can enable widespread adoption of green hydrogen in key end-use sectors:

- Near- and long-term policy support in the form of waivers and tax cuts, mandates, production linked incentives, and viability gap funding to bring the cost of green hydrogen down, so that it can start competing with natural gas-based hydrogen production.

- Initial deployment that centers around industrial clusters, where resources can be shared and where production can be close to demand centers to minimize transportation costs.

- Enabling a market for exports of products such as green steel (steel produced via green hydrogen-based DRI process) and green ammonia (ammonia produced via green hydrogen as feedstock).

Exhibit 2: Enabling the Green Hydrogen Economy

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.