Learn how we are working to transform how we use and produce energy.

Opportunities for Near-Zero-Emissions Steel Production in the Great Lakes

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Introduction

Ore-based, near-zero-emissions steel technologies offer an immense opportunity for new investment in the US steel industry.i Although scrap-based steel production has proliferated rapidly across the United States in recent decades, ore-based assets remain the industry linchpin for high-quality production, sectoral greenhouse gas emissions, and community impact. In the Great Lakes region, investments in ore-based technologies could help maintain high-quality jobs, offer an opportunity for employment growth, and contribute to the health and financial stability of local communities. Recent federal legislation represents a unique and significant opportunity to de-risk investments, spur innovation, and secure demand in this sector. That said, states and economic developers have a critical role to play in determining the industry’s outlook and its impact across the region.

Capitalizing on federal incentives and recent technological advancements requires aggressive action. Thus, policymakers and economic development organizations (EDOs) in the region are well positioned to (1) provide a steel-specific regional and comprehensive strategy to guide and maximize industry efforts; (2) leverage investments and regulatory frameworks as catalysts for bold and complementary action; and (3) ensure the industry’s competitiveness while promoting regional development and delivering economic benefits to local communities.

To date, states in the Great Lakes region have been slow to implement coordinated industrial strategies to support the development of a near-zero-emissions steel industry in the region. Figure 1 summarizes this report’s industrial policy gap analysis among Great Lakes states and the federal government, illustrating how even in large steel-producing states like Indiana, Ohio, and Pennsylvania, there is modest progress in strategic coordination, production incentives, and demand-pull measures to nurture the industry’s development. It also demonstrates how the federal government is leading from the front and creating a range of opportunities for states to implement complementary strategies.

Figure 1: Near Zero Emissions Steel Policy Gap Analysis in the Great Lakes

This brief provides an overview of the economic, social, and environmental opportunities for the Great Lakes of a robust near zero-emissions steel sector. It includes an overview of the steel industry in the United States and an assessment of the challenges of transitioning to a near-zero-emissions future. It describes recent global trends in the industry and the anticipated impacts on labor and the environment. Finally, it provides an overview of the federal and state policies supporting the industry and identifies the gaps where additional policies are needed to develop a competitive sector in the region.

[i] Definitions and terms to describe lower emissions steel vary across voluntary and compliance-based standards. RMI aligns with the First Movers Coalition definition.

Steel Industry Overview

History and Strengths of Steelmaking in the United States

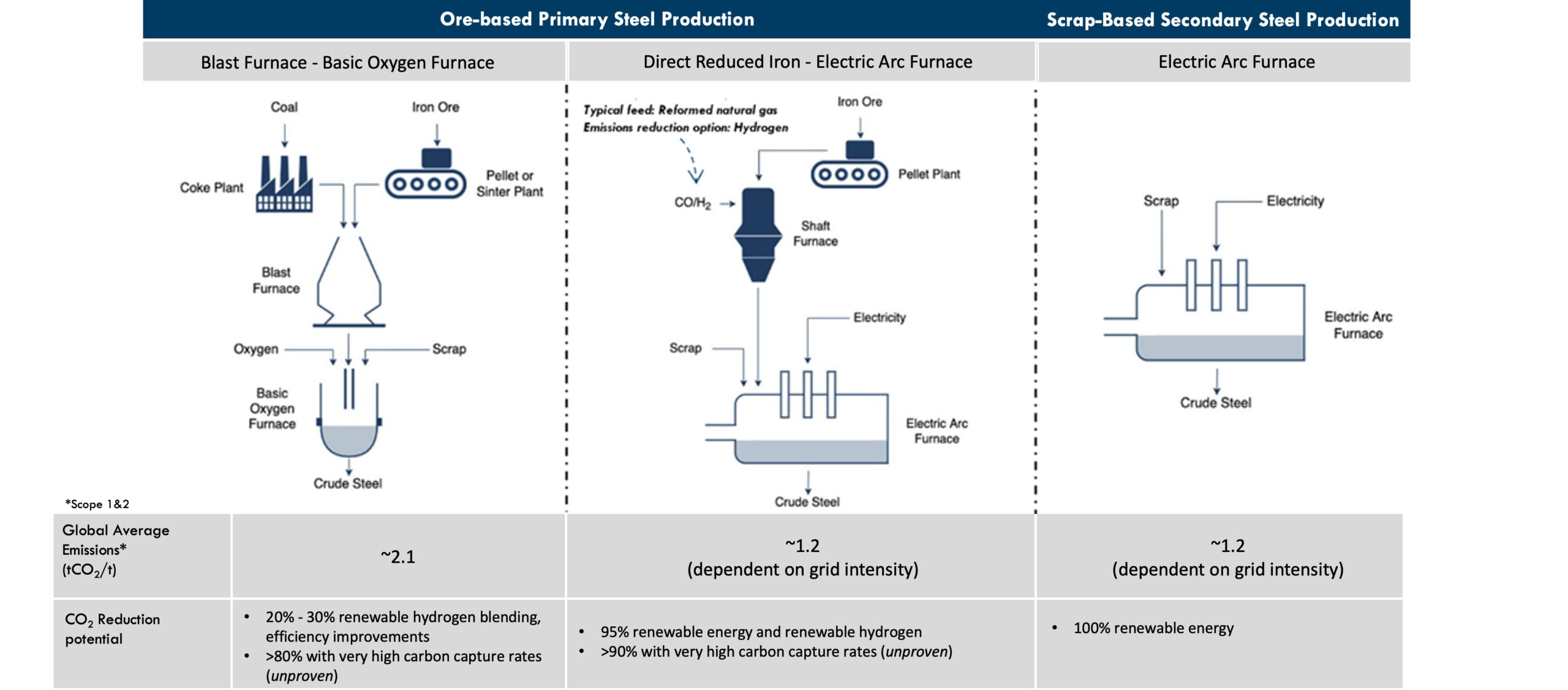

In the United States, steel is currently produced by one of three methods. The simplified process flow for each method is depicted in Figure 2. Blast furnace–basic oxygen furnace (BF-BOF) steelmaking, often referred to as integrated steelmaking, is responsible for ~30% of US supply and ~73% of CO2 emissions from the sector. BF-BOF and direct reduced iron (DRI) steelmaking are known as primary production methods, converting iron ore into crude steel. Secondary steelmaking, the reheating of recycled steel scrap in electric arc furnaces (EAFs), represents about 70% of US steel production.

Figure 2: US Steel Production Archetypes

The BF-BOF production pathway relies on coal and coke to reduce iron oxide pellets into crude steel. The DRI pathway also reduces iron oxide pellets but does so with natural gas, reducing average emissions intensity by almost half. Although natural gas has historically been used as the reducing agent for DRI operation in the United States, steel producers now have the option to use pure hydrogen gas. Swapping out natural gas for renewably produced hydrogen has the potential to reduce emissions from DRI operations by approximately 95%. EAFs rely on electricity as their primary energy source; emissions intensity is significantly affected by the electrical generation source. The full suite of meaningful decarbonization options for these production pathways are listed in the bottom row in Figure 2.

In 2021, the United States was a net exporter of crude steel and the world’s fourth-largest crude producer. Primary US steel production occurs at nine BF-BOF facilities and three DRI facilities. The production capacity from these assets and the companies that operate them are depicted in Figure 3.[ii][iii]

Figure 3: US Steel Production Capacity (Million Tons per Year)

Over the past several decades, the United States has been steadily increasing its EAF production share. US EAF production began more than 100 years ago, but its adoption really began to take hold in the 1960s, from which point it has consistently grown, increasing production share by about 1% to 2% annually. The United States has one of the highest global production shares of EAF steelmaking, contributing to the relatively low average emissions intensity of US steel. Increasing EAF production has helped US steel producers realize increased profits with lower capital and operational expenses while also reducing CO2 emissions and local air pollution. While the proliferation of EAF steelmaking in the United States continues, the need for primary steel production persists. Certain high-quality steel products — classified by their low impurity concentrations — require production via primary methods. So long as demand exists for these products and EAF technology remains unable to produce them, primary production assets will require continued investment.

Figure 4: Map of Steel Production Facilities by Technology and Capacity

Figure 4 displays the geographic distribution of both the primary and secondary steelmaking assets as well as the active iron ore mines, coke-making facilities, and major off-takers (automotive manufacturing/assembly plants). The seven mines clustered in Minnesota and Michigan are all majority owned by Cleveland-Cliffs and US Steel as vertically integrated assets. The southeastern region of the United States has seen considerable investment recently with EAFs opening near automotive manufacturing facilities and major waterways that are used for material transport. DRI operations are spread out across the eastern half of the country in Louisianna, Ohio and Texas. The facilities in Louisiana and Texas are operated by Nucor and ArcelorMittal, respectively. These companies have no US iron ore mining operations but leverage their proximity to major international ports for material transport.

[ii] US steel Granite City Works is currently idled while a lease agreement is being negotiated with SunCoke.

[iii] Cleveland-Cliffs’ Riverdale facility in Illinois is unique in that there is no blast furnace onsite, pig iron along with other iron bearing material are imported and converted to crude steel using a standalone basic oxygen furnace.

Industry Changes and Trends

Global demand for near-zero-emissions steel is growing rapidly and could hit 200 million tons by 2030. In the United States, demand for low-emissions steel is being led by the automotive sector, as indicated in Figure 5. Strong demand signals in the form of steel-specific buyers’ alliances, such as the First Movers Coalition and Steel Zero, along with Scope 3 emissions reduction commitments indicate the commitment of steel buyers to source near-zero-emissions steel. The federal government, through Buy Clean public procurement initiatives, is also signaling it will drive considerable low-emissions steel demand in the construction sector. These demand signals indicate there is the potential for more than 6 million tons of low-emissions steel demand in the United States by 2030. This volume of steel demand would require the construction of multiple low-emissions production facilities.

Figure 5: Automotive Sector Leads Corporate Commitments for Low-Emissions Steel Demand in the US (Million Tons per Year)

Technology transitions are nothing new for the steel industry. The increasing adoption of EAF technology in the United States and the ongoing transition away from open-hearth technology globally are examples of critical junctures for steel producers, which risk losing market share if they do not transition along with the market. In addition to expanding their EAF production profiles, US steelmakers have also begun to invest in new primary production methods. The pace of these investments, however, remains very slow. In the past decade, Nucor (2013), ArcelorMittal (2017), and Cleveland-Cliffs (2020) each began natural gas DRI operations to produce a less emissions-intensive iron product compared with the blast furnace alternative. Just this year (2023), Nucor made it public that it will be investigating carbon capture feasibility at its DRI plant in a partnership with ExxonMobil. US Steel has also announced its intention to pursue carbon capture feasibility at its Gary Works BF-BOF facility in Indiana. Cleveland-Cliffs has conducted hydrogen injection trials at its BF-BOF facility in Illinois and recently announced that it will conduct similar trials at one of its BF-BOF facilities in Indiana.[iv]

Figure 6: Decarbonization Investments Made by US Steel Producers

Nucor and US Steel are now offering lower-emissions steel products, Econiq and VerdeX respectively, labels given by company-own certification/requirements, which are both being produced at EAF facilities. US Steel produces the VerdeX product at its new Big River Steel facility in Arkansas. This facility represents US Steel’s largest investment in lower-emissions steel production to date.

As indicated in Figure 7, the most common decarbonization investments made globally involve the conversion to or new construction of DRI assets. Carbon capture systems have been incorporated at BF-BOF and DRI facilities across the Middle East, Mexico, Asia, and Europe. Multiple hydrogen DRI facilities are being developed in Sweden, leveraging renewable power for electrolytic hydrogen production.

Beyond technological investments, policies are also taking shape that will influence the global low-emissions steel market. The steel industry is highly globalized, with 25% of the steel produced globally traded in 2021. Countries are looking to implement regulations to address global excess steelmaking capacity and minimize carbon leakage by supporting the reduction of steel’s carbon intensity. Examples include the European Carbon Border Adjustment Mechanism initiative and the US–EU steel and aluminum deal. In a market with companies highly exposed to global market volatility and narrow profit margins, 14% of steel companies face value risk if they are unable to decrease their environmental impact.

Figure 7: Global Steel Decarbonization Trends

[iv] Hydrogen incorporation into BF-BOF operations has the potential to reduce emissions from fossil fuel inputs by 20%–30%.

Transition Challenges

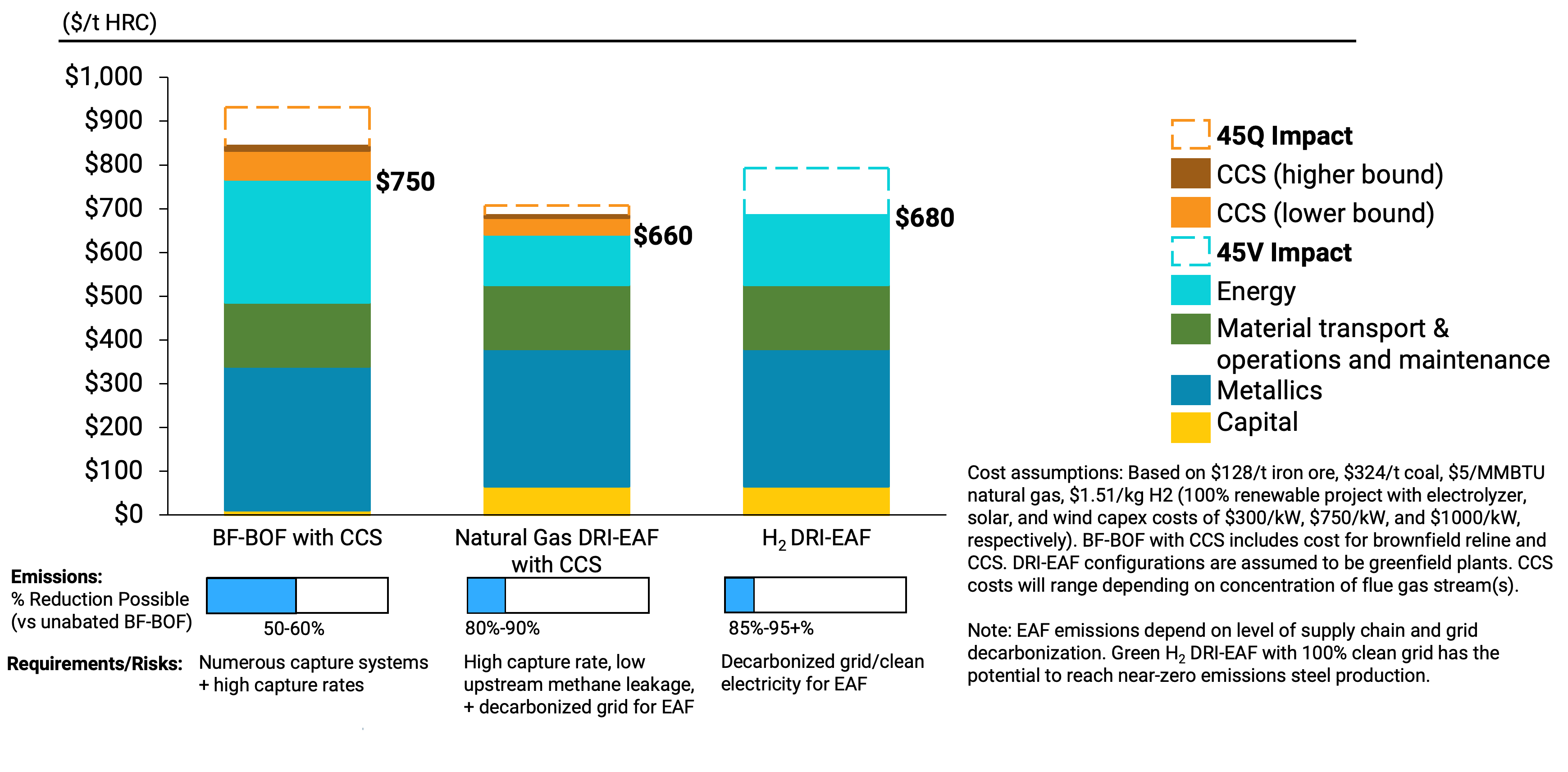

Given the existing landscape of primary steel production assets in the United States, there are three likely emissions reduction scenarios to consider. The levelized cost of steel production for each of these pathways is portrayed in Figure 8. Each pathway is competitive with traditional steel production due to reduced energy costs stemming from federal tax incentives 45Q and 45V. Although these pathways are projected as the front-runners, several hurdles remain for steel producers to navigate before investments can be made.

For the BF-BOF with carbon capture and storage (CCS) configuration, the challenge is ensuring collection of all CO2 streams and high efficiency of the carbon capture system. BF-BOF facilities have many concurrent operations on-site, several of which release large amounts of CO2 independently. Aggregating all these point sources across the plant or installing CCS systems at each individual point source would be costly and logistically challenging, with no steel producer globally trialing this pathway. Incorporating CCS at a DRI facility is considerably easier given that only a single flue gas stream requires treatment. The H2 DRI-EAF has the lowest emissions intensity and, when accounting for federal subsidies, the lowest levelized cost among these pathways, consistent with surging investment in this technology.

Figure 8: Levelized Cost of Primary Steel Production via Emissions Reduction Pathways

CCS implementation poses other challenges beyond those specific to on-site efficiency. To start, primary steel facilities, either BF-BOF or DRI (with natural gas), require capture of large volumes of CO2 (up to approximately 10 million tons per year in the United States). Transporting and storing or securing legitimate off-take for this volume of CO2 may be logistically and financially difficult, especially for steel mills operating in urban settings. Finding options that are near steel mills may pose a challenge for steel producers looking to retrofit capture technology.

Although the use of CO2 for enhanced oil recovery is somewhat commonplace in places like Texas (and brings complications in emissions accounting for the upstream product), subsurface sequestration at industrial scale remains a nascent industry in the United States and utilization of the carbon must validate emissions reduction claims at the steel facility. Only two US states have Class VI primacy, North Dakota and Wyoming, but multiple CCS research efforts and pilot projects are under way across the Great Lakes.

Additionally, many CCS systems require considerable energy of their own in the form of heat. For amine-based post-combustion systems, commonly used in commercial applications today, that heat requirement can be from 3 to 4 gigajoules per ton of captured CO2. In some cases, this heat can be provided by leveraging available waste heat, but in many situations, CCS systems increase on-site natural gas consumption. An investment in CCS locks steel producers into fossil-based reductants (coal or natural gas) and the upstream methane leakage that comes from corresponding extraction sites. If natural gas is used to generate the heat required for the system, that leakage rate will only increase.

Newer, more efficient capture technologies are coming into the market rapidly, many of which have the potential to reduce the additional energy demand on-site, and some are even capable of leveraging renewable energy for their operation. Ultimately, the viability of CCS systems relies heavily on the capture rate and true emissions abatement they can offer steel producers. Natural gas DRI with CCS is a viable near-zero-emissions production pathway if high capture rates (90% or greater) and certified low upstream methane leakage from natural gas wells can be achieved.

Renewable hydrogen-based pathways will also require steel producers or upstream energy providers to develop strategies for transporting and storing large volumes of gaseous fuel.[v] The US hydrogen industry will require considerable scaling to support new industrial off-take at this scale. Figure 9 compares the facility demand for a 2 million tons per year hydrogen DRI steel plant against the projected hydrogen production potential in the Great Lakes region by 2050. The approximately 2.25 gigawatts of renewable generation capacity required for electrolytic hydrogen production represents about 1.3% of the total generation capacity projected by the National Renewable Energy Laboratory across the Great Lakes states in 2050.

Dedicating even 1.3% of the total renewable generation capacity to a single facility may be a difficult proposition for Great Lakes utilities, disregarding any extra conditions placed on renewable electricity procurement (e.g., those expected for 45v). Considering this, steel producers should be encouraged to consider bringing additional renewable capacity online themselves if they are pursuing electrolytic hydrogen production methods.

Figure 9: Renewable Capacity Required for Green Hydrogen DRI Relative to Great Lakes Regional Capacity in 2050

In addition to the 45V and 45Q tax credits, steel producers also can apply for cost share and loan-based funding from the federal government. These programs, led by the Office of Clean Energy Demonstrations (OCED) and the Loan Programs Office (LPO), both part of the US Department of Energy (DOE), support modifications to existing facilities as well as greenfield investments and can offer support up to about $500 million per project. On a levelized basis, the cost reduction from an investment of this magnitude is about $14 per ton hot rolled coil (HRC).[vi] As Figure 8 indicates, the DRI process routes offer the most competitive production costs while also offering the greatest emissions reduction potential. Although greenfield DRI configurations require relatively high levels of capital for construction, their reduced energy costs stand to make them the better bet in the long run.

[vi] Assuming an asset life of 20 years with a production capacity of 2 million tons per year and a utilization rate of 90%.

Economic and Labor Implications

By the end of the 20th century, China had replaced the United States as the world’s largest steel manufacturer, and over the course of the early 21st century, more than half of all US steel manufacturing capacity was lost. Through this transition, the Great Lakes remained the heartland of US steelmaking. The four states with the largest employment in the industry are all in the Great Lakes, and two-thirds of the nation’s 80,000 steelworkers are in the region. Indiana is the most specialized in the industry, with 10 times the share of steelworkers in the state as the national average. Ohio and Pennsylvania have around 3.5 times the national average.

In 2017, the value added of primary metal manufacturing in the United States was concentrated in the region, with Indiana accounting for 15% of the national total; Ohio, 10%; Pennsylvania, 9%; and Michigan, 5%. In terms of production, the region accounted for 60% of US steel production in 2021: Indiana, 27%; Ohio, 11%; Pennsylvania, 5%; Illinois, 4%; and Michigan, 3%.

Figure 10: The Great Lakes Remains the Heartland of US Steelmaking

Subregions within the Great Lakes specialize in specific segments of the steelmaking industry. For example, Fort Wayne, Indiana, has 208 times the national average share of workers employed in steel wire drawing, while Pittsburgh has 19 times the share of workers in iron and steel mills. Almost one hundred percent of iron ore mining jobs are in the Duluth, Minnesota, area; a third of all steel foundries are in the Detroit-Warren-Flint area of Michigan; and 31% of iron and steel pipe and tube manufacturing is in the Cleveland-Akron-Elyria area of Ohio. Further, all the integrated steel mills in the United States are in the Great Lakes: Indiana has three; Ohio, two; Illinois, two; Michigan, one; and Pennsylvania, one. There are also numerous EAFs spread across the Great Lakes states: Ohio with nine; Illinois, five; Indiana, five; Pennsylvania, three; Minnesota, one; Wisconsin, one; and Michigan one.

Figure 11: Specializations In The Elements of the Steel Industry Vary Across The Great Lakes Region

Although the US steel industry may have shrunk in global significance, it is one of the cleanest globally given its share of EAFs and is in a strong position to capitalize on technological shifts in the industry. As previously mentioned, EAF steelmaking relying solely on scrap cannot yet fully supply domestic steel demand, which is excepted to see a nearly 40 million ton increase in the wake of the 2022 Inflation Reduction Act (IRA). Primary steel from integrated mills will continue to see demand and require investments in new low-emissions technologies. Considering the long reinvestment cycle for primary steel plants, it is crucial to transform these assets and avoid locking them in to emissions-intensive production methods for years to come.

The transition to green steel will require major changes in steelmaking technology by increasing energy efficiency, adopting low-carbon fuels such as hydrogen generated from renewable energy, and incorporating carbon capture technologies. The magnitude of investment required to transition an existing primary asset or to construct a new asset is on the order of hundreds of millions, potentially billions of dollars. Investments at that scale have the potential to generate multiple streams of revenue for states and local communities through taxable employee wages, colocation of upstream and downstream supply chain assets, corporate spending in the community, and tangential public infrastructure investments.

Figure 12: US Steel Demand Increase Driven by IRA (Million Tons)

Importantly, future steel production capacity, regardless of technology, is likely to follow existing patterns of production, given the off-take partnerships and upstream infrastructure that have been established over decades. Emissions reduction investments for primary steel assets will either be applied as upgrades to existing facilities concentrated in the Great Lakes or at greenfield sites.

Greenfield facilities, either DRI (to produce a briquette product) or EAF, have the potential to be distributed across the United States. When siting these facilities, steel producers will be targeting locations that have suitable local infrastructure and development areas, favorable logistics and transport options, an available workforce, and off-take for their products. The concentration of iron ore mines and reserves in Michigan and Minnesota make the Great Lakes a front-runner for greenfield siting, but locations across the Southeast and Texas are also attractive given their proximity to new auto manufacturing supply chains, access to energy sources (natural gas and renewable energy), and relatively cost-effective, nonunionized labor. To ensure the Great Lakes retains its status as the steel production capital of the United States, efforts must be put forth to make sure investments in low-emissions production technology are attracted locally. The steel industry has long been a source of high-quality jobs, often concentrated in large numbers at integrated facilities. The technological and operational changes required to produce low-emissions steel products will certainly affect the nature, number, and location of steel manufacturing employment.

Both the hydrogen and CCS pathways highlighted in Figure 8 project to increase direct employment throughout the steel supply chain compared with incumbent Great Lakes BF-BOF production, where employment has been in decline over recent decades.[vii] The incumbent BF-BOF supply chain for a 2-mtpa-capacity facility, from coal mining through the production of crude steel, directly employs about 1,350 individuals. An equivalently sized hydrogen DRI facility has the potential to directly employ between 1,300 and 1,700 individuals throughout the supply chain.[viii]

These jobs would include operating upstream renewable energy and hydrogen resources in addition to the employment at DRI and EAF facilities. CCS retrofits at BF-BOF locations will bring additional jobs, approximately 30 to 40 operational jobs depending on the volume of CO2 captured from the site, while also retaining the current labor force. A CCS DRI-EAF pathway projects to reduce employment throughout the steel production supply chain compared to incumbent BF-BOF production. The CCS DRI-EAF pathway will generate negligible additional employment in the natural gas distribution sector and the DRI, EAF, and CCS operations will employ roughly 1,000 individuals.

DRI pathways, hydrogen and natural gas based, do not require upstream activities to be collocated like those at integrated facilities. Renewable energy production, hydrogen production, and natural gas extraction could potentially be geographically distributed across different communities or even different states. That is not to say that these activities cannot be collocated; on-site renewable energy and hydrogen production is a reasonable option for steel producers that would help aggregate supply chain employment in one spot and potentially maintain and grow employment at existing integrated locations.

Another risk moving forward is the quality of jobs within the steel industry. Traditionally, integrated sites have been dominated by union labor, which has offered many benefits and protections for steelworkers. However, in recent decades, many steel facilities have shifted away from union employment, including US Steel, a longtime union supporter. The shift away from union employment has coincided with the shift to EAF, scrap-based production, and a geographical shift to Southern right-to-work states. Siting new facilities and investing in brownfield sites for retrofits or technology overhauls in the Great Lakes will help the steel industry retain and potentially increase its share of union employees.

[vii] The hyperlinked Ohio River Valley report indicates job decline for the Mon Valley Works locations in Western Pennsylvania, but the trend is similar across the majority of steel-producing Great Lakes states.

[viii] Estimated employment range for hydrogen DRI steelmaking is based on the share of wind and solar resources selected for use in hydrogen production.

Local Environmental Pollution

In addition to the carbon dioxide emitted from typical steelmaking operations, there are numerous local air pollutants that can affect the health of neighboring communities. These pollutants have been shown to affect cancer rates, heart health and contribute to a variety of respiratory issues as well as other health challenges. High pollution levels can also have a deleterious impact on local economic conditions, investment attractiveness, and population growth.

Figure 13 depicts the emissions of these criteria pollutants from currently operating steel facilities in Ohio. The facility data from four Cleveland-Cliffs facilities (Warren Coke Plant, Cleveland Works BF-BOF, Mansfield EAF, and Toledo DRI) was used to produce emissions totals for the BF-BOF and DRI-EAF production pathways.[ix] On a per-ton basis, the DRI-EAF production pathways significantly reduce emissions of these harmful pollutants. Implementing CCS on the DRI or switching to hydrogen-based production would result in comparable reductions to those shown in the figure. CCS implementation at BF-BOF locations may help reduce criteria pollution because many CCS technologies require scrubbing prior to capture being performed.[x]

Figure 13: Criteria Air Pollution from Steel Production Pathways in Ohio

For decades, community groups and environmental pollution–focused nonprofits have advocated for stricter air and water pollution standards for integrated facilities and related upstream activities (coke plants, mine sites, and pellet operations). This fight continues today as many of these groups are providing feedback and official comments on new National Emission Standards for Hazardous Air Pollutants being implemented by the US Environmental Protection Agency (EPA) for integrated facilities and coke ovens.[xi] Supporting the health and livelihoods of fence-line and neighboring communities is essential for ensuring the steel industry continues to grow and thrive in the Great Lakes.

[ix] The Toledo DRI operated by Cleveland-Cliffs uses reformed natural gas as its primary reductant.

[x] In many cases flues gases from integrated sites are already scrubbed for criteria pollutants. It is possible a CCS system may require additional scrubbing or provide a means of removal inherent in the capture technology. It should not be assumed that all capture technology and configurations will reduce these pollutants at BF-BOF facilities.

[xi] NESHAP (National Emissions Standards for Hazardous Air Pollutants) regulations for coke ovens: https://www.epa.gov/stationary-sources-air-pollution/coke-ovens-batteries-national-emissions-standards-hazardous-air

Path to Near-Zero-Emissions Steel Production in the Great Lakes

Transitioning the established footprint of steel in the Great Lakes to near-zero-emissions technologies will require supply chain coordination, investment attraction, and procurement strategies while leveraging policy mechanisms to ensure the longevity of the industry in the region. The passage of the IRA and the Infrastructure Investment and Jobs Act (IIJA) of 2021 represents a historic opportunity by providing funding for research, development, and deployment of new technologies, boosting domestic production, and positioning a market for near-zero-emissions steel.

State policymakers and EDOs in the Great Lakes should develop a holistic industrial and steel-specific strategy that ensures federal funding has its maximum impact on regional economic development. States can leverage investments and regulatory frameworks as catalysts to ensure the steel industry in the region is globally competitive while delivering economic benefits to local communities.

Specifically for the steel industry, a clean transition in the near term involves overcoming certain bottlenecks. The implementation speed and impact of federal funding opportunities and the ability of steel producers to transition to cleaner production methods will depend heavily on the ability of industry and political actors to address these specific challenges:

- Procuring competitive renewable energy to power EAFs

- Procuring competitive renewable energy and renewable hydrogen contracts for primary production facilities that have pricing flexibility and that would meet the yet-to-be-finalized requirements of 45V.

- Siting and permitting timelines for retrofit and greenfield steel projects along with their upstream energy sources (renewable electricity, transmissions, and storage).

- Establishing regulations, guidelines, and permitting for CO2 transmission and storage.

- Aligning with international independent standards and certifications to attract investment and demand for near-zero-emissions steel.

Policy Landscape

Without appropriate policy guidance and support, the Great Lakes runs the risk of market participants being caught flat-footed, leaving potential jobs and investment opportunities on the table. This research provides a unique policy gap analysis of selective policies focusing on the steel industry at the federal level and in the Great Lakes to better understand what regional policymakers can do to ensure investors and communities are not left behind. It uses a typology of industrial policies used globally in similar technology transitions, relying especially on a novel framework developed by the Organization for Economic Co-operation and Development.

Broadly speaking, “industrial policy” simply refers to any goal-oriented state action where the “purpose is to shape the composition of economic activity,” in this case with specific reference to iron and steel. Although there is a vast range of policy instruments that can be used to improve strategic or economically important sectors, these policies can be grouped into four primary domains: strategic coordination, production instruments, demand-pull mechanisms, and cross-sectoral interventions. Within each domain, the policy instruments are grouped based on their similarities:

- Strategic coordination: Considers any effort of policy governance such as public–private coalitions, sectoral competitiveness assessments, and technology roadmaps. Often, policymakers choose to commission industry strategy or technology roadmaps to guide and complement the other categories of industrial policy intervention. These would usually be accompanied by a vision statement and a set of objectives and targets.

- Production instruments: Affect the economics of firm-level production and investment decisions for individual firms within the target sector. This can include a range of financial incentives — such as subsidies, grants, or tax credits — to promote research, development, and demonstration (RD&D) activities or otherwise facilitate additional investment, particularly in novel technologies. Production instruments can also affect firm performance through the provision of key inputs, such as skilled labor, or through addressing supply chain gaps.

- Demand-pull mechanisms: Apply to the consumption of the product(s) produced by the industry. These can include sales taxes, mandates, public procurement, and certain product standards and definitions.

- Cross-sectoral interventions: Affect the whole industry through regulations governing the allocation of production factors, including land, capital, and labor. Interventions can also include cross-sectoral policies that affect the target industry, such as competition or trade policy, and the development of enabling technologies crucial to green steel development.

The policy gap analysis was developed for steel-specific policies and key enabling technologies like hydrogen, carbon capture, and clean electricity. Although each state has relevant climate and industry policies, they are not considered industrial strategies unless they specifically pertain to the development of a near-zero-emissions steel sector. After conducting the landscape assessment, the study identified regional gaps between federal and state policies and highlighted efforts that states should learn from and follow. Figure 14 presents the landscape assessment for federal and state policies in the Great Lakes region.

Figure 1: Near-Zero-Emissions Steel Policy Gap Analysis in the Great Lakes

Strategic Coordination

Providing a strategy with a clear vision and goals for the sector is a crucial element for the industry, considering the investment in and life cycle of these assets. Strategic coordination may include providing a steel-specific technology or industry roadmap for steelmakers to follow, aligning economic opportunities with decarbonization targets, and providing coordination among other industries that will be affected by the transition in steel, such as coal, gas, renewables, automotive, and construction.

The federal government established the goal to reduce US greenhouse gas (GHG) emissions 50% to 52% below 2005 levels by 2030 and to achieve a net-zero-emissions economy by 2050; it also aims to achieve net-zero-emissions procurement by 2050 through its Buy Clean initiative for low-carbon materials, which includes steel. The DOE’s Industrial Decarbonization Roadmap established that US steel production can reach near-zero emissions in 2050 with aggressive adoption of energy efficiency; industrial decarbonization; carbon capture, utilization, and storage (CCUS); and low-carbon fuels such as hydrogen.

Most states in the Great Lakes region have economy-wide targets for reducing GHG emissions, including for the industrial and manufacturing sectors, with Indiana and Ohio as the only states that have yet to establish targets. However, no state in the Great Lakes region has set specific GHG targets for the steel industry or a target timetable for the sector’s transition. For example Indiana’s 21st Century Energy Task Force, Michigan’s Healthy Climate Plan, and the Pennsylvania Climate Action Plan 2021, do not mention near-zero-emissions steel, with the sector receiving only token attention for industrial energy efficiency.

States should develop coordinated and regional implementation plans to transition the steel industry. The plan should bring to life DOE’s roadmap and provide specific emissions reduction targets for steelmaking facilities and related processes. For example, in ACEEE’s report, Sustainable Metals Manufacturing Opportunities in Indiana, opportunities, challenges, and paths forward are discussed for the aluminum, steel, and electric vehicle (EV) industries. This report outlines how to achieve a sustainable transition for these sectors and draw connections between the decarbonization of one to another (e.g., green steel and EV manufacturing). Similar goals and timelines should be outlined by state agencies in steel plans to ensure steady progress toward a revitalized and strengthening industry.

Production Instruments

Research, Development, and Demonstration

Scaling new technologies for low-emissions steel requires investments in research and development and pilot projects. The incumbent US steel industry has been slow to innovate or adopt new technologies, given the cost-effective reliability current assets provide. For context, the newest operating blast furnace in the United States opened in 1964 in Burns Harbor, Indiana. The iron and steel manufacturing sectors spend a smaller proportion of revenue on RD&D than other manufacturing subsectors, such as computer and electronic products or motor vehicles.

Although RD&D spending is relatively low, multiple smaller companies (such as Boston Metal and Electra) are exploring exiting direct electrolysis technologies as their primary business model. Direct electrolysis is a predominantly electrified method of primary steel production that, if proved at scale, can offer a highly efficient, near-zero-emissions steel product. Mature clean technologies such as DRI units with CCS or hydrogen production methods are in demonstration outside US borders. Enabling demonstration of these more mature clean technologies should remain a priority for implementation in the near term.

The primary funding channel for testing and demonstrating new green steel technologies comes from the federal government with $500 million through the Industrial Demonstration program. In addition, the LPO provides loan guarantees for more than $13 billion for Innovate Clean Energy projects to reduce GHG emissions from industrial applications. H2 Green Steel, one of the two companies in Sweden developing a hydrogen-based DRI steel plant, has successfully relied on public funding support in the form of debt guarantees to de-risk its first-of-kind project.

Great Lakes states should leverage the RD&D opportunities identified by the DOE and work with industry partners to develop pilot archetypes. Cleveland-Cliffs and US Steel have already shown a willingness to pursue pilot projects at some of their Great Lakes BF-BOF facilities in the form of hydrogen injection trials and CCS incorporation, but the frequency and scale could be greatly increased with support from public funding sources. Pilots and trials will be necessary for steel producers to become familiar with new processes and materials. Leveraging federal funding for pilot projects and RD&D technologies that can scale and mature over time offers a foundation for further investment and industry growth. It will be important that these states and, to the extent that they are able, private institutions make data and information from pilot projects accessible.

Figure 15: RD&D Opportunities Identified by the DOE for the US Steel Industry

The bankability of green steel projects depends on getting projects off the ground to pave the way for more significant volumes of transition financing. Investing in RD&D is a vital first step in this process. Currently, no Great Lakes states have RD&D funds set aside for innovating in green steel, although there are some programs available that indirectly affect the industry such as CCUS innovation.

Production Efficiency

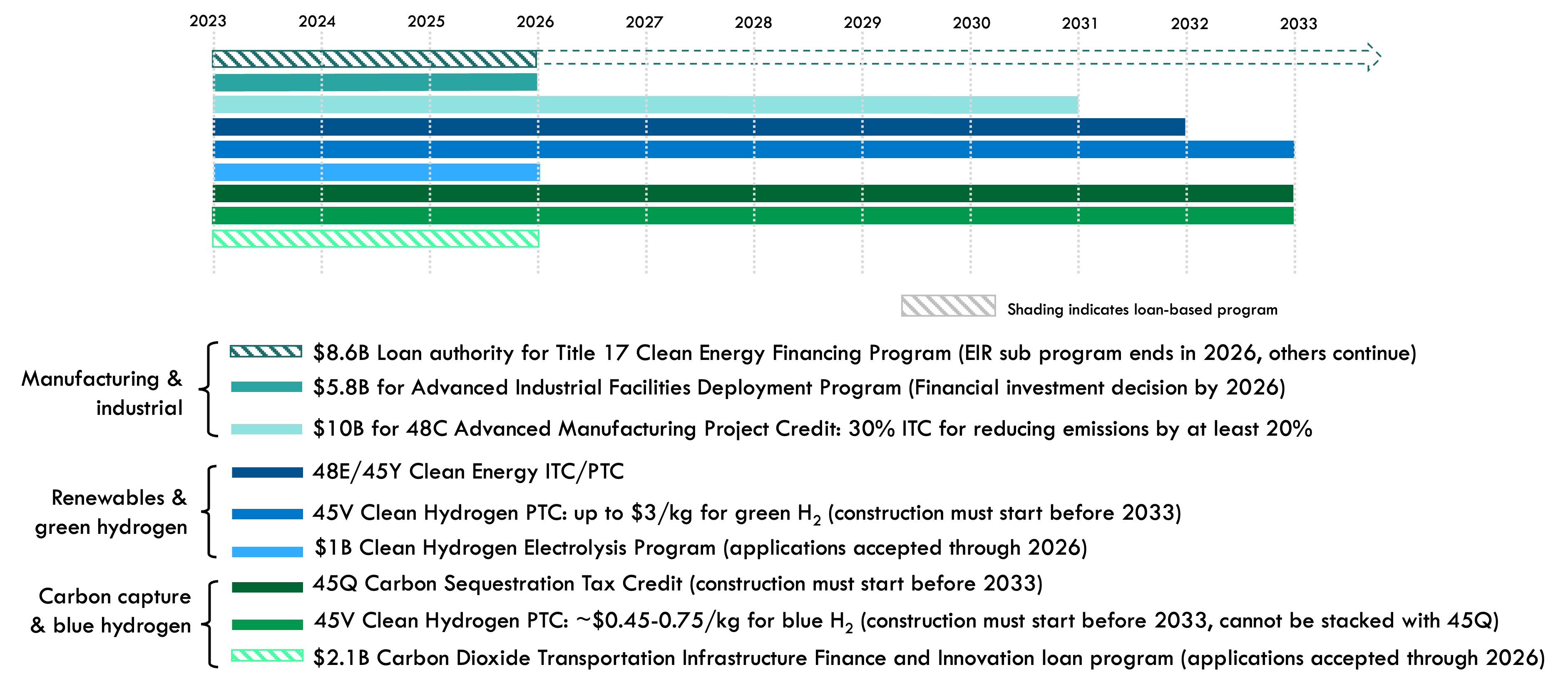

Figure 16 provides a timeline and overview of the major federal funding mechanisms applicable for low-emissions steel. The different requirements, timelines, and availability periods can represent a challenge when reviewing the stacking or “size of prize,” with the window between 2023 and 2026 representing the greatest potential for maximizing funding.

The Industrial Demonstration Program, as mentioned previously, provides RD&D funding to steel and other industrial manufacturers to implement widespread demonstration and deployment of decarbonization technologies within this sector. The Advanced Industrial Facilities Deployment Program provides financial support to energy-intensive industrial facilities to reduce GHG emissions. Finally, the Qualifying Advanced Energy Project Credit (48C) Program was created to provide tax credits for advanced energy projects in the US industrial sector. There are several other federal tax credits that indirectly affect the steel industry and are examined in the cross-sectoral section of this report.

Figure 16: Federal Incentives That Can Help Facilitate Near-Zero-Emissions Steel Production

At the state level, there is a lack of steel-specific production policy in the Great Lakes region. However, state economic development agencies can offer financing opportunities to sustainable steel companies to attract them their states. Further, the eligibility of existing lending, loan guarantees, and grant programs can be expanded to include the development and deployment of hydrogen and carbon capture technologies. States can also tailor tax policies to provide exemptions and reductions in property and sales taxes on machinery and equipment. Although state programs do not tend to reach the scale of federal incentives, the impact of these financing and grants can be meaningful.

Demand-Pull Mechanisms

Both public and private entities can leverage their purchasing power to send a clear demand signal for lower-emissions steel in the near term, thereby solidifying the investment case for the producer. These procurement strategies may be required to close the price gap between current products and cleaner alternatives where a premium could be added to the end products. Leveraging government purchasing power through mandates is fundamental to providing robust, centralized, and reliable demand over time. Although low-emissions steel production technologies are commercially available, major investments in new assets or retrofits present considerable risk for steel producers. Increasing demand helps reduce risk for first movers that can be guaranteed their new products will sell, potentially at a premium, to stable off-takes like the state and federal government.

The Federal Buy Clean Task Force, established in December 2021, seeks to promote low-carbon and made-in-America construction materials, such as steel. The domestic content requirements in some provisions from IIJA, the CHIPS and Science Act (2022), and the IRA could provide a demand certainty for the steel industry. Also, the domestic procurement from IIJA and the Build America Buy America Act (2021) could support demand for electrical steel, especially used in transformers, EVs, and EV supply equipment. Electrical steel is produced in only two facilities in the United States, one in Ohio and one in Pennsylvania.

Minnesota’s Energy and Climate Omnibus bill includes both a Buy Clean study and a Buy Clean/Buy Fair pilot program that applies to steel rebar and structural steel. The Buy Clean study requires data compilation related to emissions released by standard building materials. Furthermore, the state will prioritize the purchase of steel and rebar with low embodied carbon. Great Lakes states need to follow Minnesota’s lead and set up Buy Clean programs for green steel to ensure the market captures the momentum generated by federal funding with enough time to mature to support the development of green steel in a post-IRA landscape.

Ensuring facilities are ready to meet buyer requirements is key. For example, major automakers with strong decarbonization goals are collocated near steel facilities in the Great Lakes. Buyer aggregation platforms, which collect commitments from private corporations, are driving visibility in this space. Groups such as the First Movers Coalition and Steel Zero are working to raise this ambition among buyers globally. The focus now is turning these commitments into off-take through procurement mechanisms, such as the Sustainable Steel Buyers Platform, which RMI is currently developing for North America.

Across the market, steel producers are already looking to differentiate their products, with a variety of in-house-developed certifications (e.g., ArcelorMittal’s Xcarb, SSAB Zero), which all vary in quantification and methods. Independent, transparent, and widely adopted standards and certification schemes are gaining momentum in the market (e.g., Responsible Steel). Alignment with these types of certification schemes, which offer true emissions reduction pathways, will ensure compatibility with buyer requirements both domestically and abroad.

Enabling Environment for Green Steel

Clean Electricity

Procuring cheap, abundant renewable electricity will be vital to reducing emissions in the steel production value chain. EAFs and electrolyzers, used for hydrogen production, will demand considerable electrical energy. As a result, clear, clean electricity goals are needed on the federal and state levels. Furthermore, renewable energy generation must be facilitated to meet the needs of decarbonizing industries.

On the federal level, the White House set a target of reaching 100% carbon pollution–free electricity by 2035, focusing on generation, transmission, storage, and the use of CCUS on existing power plants. The IRA’s clean energy credits, such as 45V, 48C, 45Y, and 48E, aim to accelerate the deployment of renewable energy generation and storage capacity. The IRA also allows developers to stack certain credits to drive down costs further. For instance, if the renewable electricity generator and hydrogen facilities are separate entities, a hydrogen project procuring exclusively renewable electricity could claim investment and production tax credits for clean hydrogen and clean electricity (subject to the soon-to-be-released time-matching criteria of 45V).

In the Great Lakes, Minnesota set a goal for 100% carbon-free electricity by 2040, and Illinois and Wisconsin by 2050. Michigan uses different language, setting a goal to reach economy-wide carbon neutrality by 2050. In addition, all states in the Great Lakes except Indiana, which has renewable portfolio goals, have enacted renewable portfolio standards. Yet there is still a lack of renewable energy generation (hydro, wind, and solar) penetration in the region, with only Wisconsin (26%), Illinois (11%), and Indiana (10%) at or above 10%, mainly due to onshore wind production. There is a need for bold renewable energy and power sector decarbonization policies across the Great Lakes, considering the region’s importance for EAFs and hydrogen development.

One of the main barriers is the time it takes projects to connect to the grid. PJM and MISO, the two main electricity operators in the Great Lakes, have 3,042 and 1,734 active projects in interconnection queues, respectively. Most of these projects are solar and wind generation or battery-based storage. PJM has publicly stated that it currently has a two-year backup for its grid connection queue and had to pause review of new requests until at least 2025. Policymakers in the region need to monitor the interconnection queue issue and find ways to streamline the process and unlock clean energy capacity already in the permitting process. Given the regional nature of transmission organizations like PJM and MISO this challenge is not one that states can resolve individually Advocating for forward looking transmission planning within states and across state lines will be essential to support the development and interconnection of new renewable generation capacity. All states in the Great Lakes have a statewide interconnection policy, providing a process customers can follow and avoid arbitrary delays. However, only Illinois and Minnesota have adopted procedures that align with the Federal Energy Regulatory Commission model rules.

Steel producers also have the option to avoid grid connection delays by constructing behind-the-meter renewable power systems. Cleveland-Cliffs and US Steel have made successful and highly profitable businesses by vertically integrating their value chains from coal and iron mining through steel production and finishing. Incorporating upstream processes is nothing new for these companies, which also already operate power generation facilities at several of their BF-BOF locations. Finding methods to incentivize steel producers to pursue behind-the-meter projects could provide a way to expedite low-emissions steel production and contribute to faster regional decarbonization.

Clean Hydrogen

As explored, clean hydrogen and near-zero-emissions steel go hand in hand. To catalyze a thriving lower-emissions steel industry, clean hydrogen production must be prioritized. The federal government published the US National Clean Hydrogen Strategy and Roadmap and Pathways to Commercial Liftoff: Clean Hydrogen to provide insights on how and when hydrogen could reach full-scale commercial adoption.

For hydrogen, the IRA provides the 45V production tax credit, which could offer up to $3 per kilogram of hydrogen based on the emissions intensity of the hydrogen production pathway. All hydrogen production pathways, including fossil fuel–based hydrogen production, are eligible for the credit, with the credit value received depending on achieving the same emissions intensity thresholds.[xii] This new tax credit will make US-produced hydrogen some of the most cost competitive in the world and in doing so make hydrogen-based steel production in the United States uniquely profitable.

Hydrogen development is also being supported federally via the Regional Clean Hydrogen Hubs program facilitated by OCED. The program includes $8 billion in total funding to establish multiple hydrogen production hubs leveraging diverse production methods and off-take sectors. Multiple hydrogen hubs in the Great Lakes region have received a notice of encouragement on their concept papers and have now submitted full applications for funding; details about each are included in Figure 17.

Figure 17: Developing Great Lakes Hydrogen Hubs

At present, the United States lacks comprehensive federal regulation governing hydrogen. There are significant gaps in US hydrogen’s regulatory structure. The federal government has yet to decide the Federal Energy Regulatory Commission’s jurisdiction over interstate hydrogen pipeline, storage, import, and export facilities. Also, it needs to establish common standards for blending hydrogen in interstate natural gas pipeline systems, considering that states such as Minnesota already allow gas utilities to submit innovation plans including hydrogen-based fuels as alternatives.

Local regulations also apply for production, transportation, and use of hydrogen. In Minnesota, Executive Order 22-22 ordered agencies to evaluate the state’s regulatory preparedness for hydrogen, and the Illinois Senate passed SB 3613 to create the Hydrogen Economy Act and the Hydrogen Economy Task Force to identify barriers to the widespread development of hydrogen. States need to proactively follow Minnesota’s and Illinois’ lead to understand their specific hydrogen regulatory landscape and be ready to assess and fill gaps when federal agencies announce updates in regulations and authority oversight. This is crucial to minimize any unexpected delays or unnecessary costs and challenges to project development.

Pennsylvania passed HB 1059, which provides a tax credit of $0.81 per kilogram of hydrogen to companies that buy hydrogen made in Pennsylvania and $0.47 to companies that buy natural gas in order to make hydrogen. These incentives have no environmental safeguard nor standard that applicants must meet to receive funding, incentivizing the production of fossil-based blue hydrogen and the purchase of natural gas. With federal subsidies financially supporting the hydrogen and CCS pathways, states in the Great Lakes can look to take a stronger role in supporting the required infrastructure and coordination of these projects.

Finally, Michigan is the only state in the region with a hydrogen roadmap, created by the University of Michigan with support from the Michigan Economic Development Corporation, which identifies steelmaking as a potential candidate to use hydrogen. The roadmap provides a high-level overview of the main steel facilities assets in the states that could adopt hydrogen and estimates GHG emissions reductions as well as implementation costs. Other Great Lakes states should leverage existing EDO and university efforts to craft similar technology road maps.

Carbon Capture and Storage

The DOE’s carbon management report provides a common fact base of the path to commercial liftoff for carbon capture technologies. There are multiple reports stating that the Great Lakes region is uniquely positioned to become a global hub for carbon capture technologies, especially for primary steel production facilities in the region because production sits near viable CO2 storage sites. Michigan and Pennsylvania have ordered reports to assess the opportunities, risks, and policy recommendations to advance the development of carbon capture technologies.

Companies will require a Class VI permit from the EPA if they intend to pursue subsurface sequestration for their CCS projects, but the process is notoriously long. Thus, several states are seeking primacy over Class VI wells to have their own regulatory agencies take on permit applications. Currently, only North Dakota and Wyoming have state primacy over Class VI and Ohio is the only state in the region seeking it.

The IIJA provides $50 million in grant funding to award underground injection control grants and to support states’ efforts to develop programs leading to primacy. Separately, the law includes $25 million in funding for the EPA to permit Class VI storage projects in those states that do not yet have Class VI primacy or choose not to pursue it. In addition to Class VI primacy, states need to complementarily establish pore space ownership, permitting processes, and long-term stewardship programs for carbon capture projects deployment.

States must establish the foundations to regulate carbon capture technologies by following the example of Indiana. Michigan is starting to lay the groundwork for future projects by including CO2 as a pipeline carrier and allowing CO2 pipelines to be viable for permitting and construction from the Michigan Public Service Commission. The Minnesota Public Utilities Commission has also taken ownership of reviewing two pipelines currently in development and setting precedent for environmental review processes moving forward. Even though these efforts are in the right direction, much more work is needed. Indiana is taking the lead in the Great Lakes under HB 1209, making the state an early adopter in CCS regulation in the region. The state built up a regulatory structure to address pore space ownership, liability, permitting, monitoring, and mineral rights primacy.

On top of funding from the IIJA, the IRA increased the 45Q tax credit from $50 to $85 per ton of CO2 captured and stored and provides a direct pay option for developers. Cost estimates for CCS implementation at steel facilities range from $40 to $100 per ton of CO2, with transmission and storage potentially adding an additional $24 per ton. In this cost range, with further declines expected, 45Q has the potential to eliminate a large percentage, if not all of the investment required for CCS implementation at steel facilities.

Workforce

It is essential to ensure that the region’s primary steelmaking and coal mining workforce can transition to fossil fuel–free steelmaking. The jobs associated with hydrogen, renewables, and carbon capture technologies will require training programs and facilitated transitioning processes.

Recent federal legislation includes specific funding focused on retraining workers as well as tangential policies that can be used to support the labor transition. The IIJA contains at least $800 million specifically dedicated to workforce development. The IRA has numerous workforce development opportunities, particularly in high-demand sectors such as clean energy and construction.

In the Great Lakes, Illinois has the most comprehensive and robust clean energy workforce development framework, through the Climate and Equitable Jobs Act (2021), including programs that prioritize iron and steelworkers. Michigan, Minnesota, Pennsylvania, and Wisconsin have several generalized workforce development programs, including for former fossil fuel communities, but without steel-specific retraining programs.

On an individual project basis, steps must be taken by developers to ensure that quality jobs and community benefits are prioritized. Legally binding project labor agreements can help enforce local hire requirements and other financial and health/safety protections for employees. Training programs at local universities, community colleges, and other publicly funded educational institutions can help the Great Lakes states position themselves ahead of the curve when it comes to producing a workforce uniquely poised to support a low-emissions steel economy.

Land

Land-based policies to support economic growth can take the form of enterprise or renaissance zones for economic, workforce, and community development, where businesses receive incentives to locate operations in these specific zones.

On the federal level, the Lawrence Livermore National Lab administers the High Performance Computing for Energy Innovation (HPC4EI) Program, which funds domestic manufacturers innovating in the energy space while encouraging them to collaborate with nonprofits and universities in opportunity zones. In 2021, one of the project recipients was steel producer ArcelorMittal, which received the award for research on creating energy-efficient steelmaking. Furthermore, the Biden administration’s Buy American program incentivizes domestic manufacturing, which encourages the placement of manufacturing sites on land in the United States.

All states in the Great Lakes region have an enterprise zone program that could benefit steelmakers. Although there are examples of steel distributors or producers of steel products taking advantage of these zones, there are no specific incentives or standards tied to steel that could encourage facilities, especially mini mills, to be in one of the zones.

The redevelopment of abandoned, underutilized, or closed steel mills also represents an opportunity to help boost a regional solar industry by installing solar panels in these brownfield sites.

The federal government offers a range of grant and loan programs designed to support brownfields redevelopment and reuse. For over two decades, the EPA has managed a range of federal brownfields grants, and most of these received historic increased funding from the IIJA. The IRA has three new grants programs that can supplement “brightfield” development. The DOE’s Energy Infrastructure Reinvestment Program offers $5 billion for low-cost loans to retool, repurpose, or replace energy infrastructure, and the EPA’s Environmental and Climate Justice Block Grants program gives $3 billion to invest in community-led projects in disadvantaged communities.

All states in the Great Lakes have funding opportunities for brownfield remediation, including for former coal mines, mostly dedicated to on-site renewable energy projects.

The installation of a 133,000-square-foot solar array on a former Pittsburgh steel mill, developed by Pennsylvania’s Regional Industrial Development Corporation, is a good example of how to leverage existing unused infrastructure to support economic growth and provide benefits to local communities.

[xii] The Treasury Department guidance to determine the emissions intensity of electrolytic hydrogen is to be released in the coming months.

Conclusion

Steel production and industrial manufacturing has been ingrained in the cultural fabric of the Great Lakes region for decades. It has been a means of economic prosperity and stability that has supported community growth, infrastructural ingenuity, and a regional identity that persists even in the face of decline. The continuation of Great Lakes steel production hinges on continued investment in steel production assets in the region, in particular investments that will facilitate the production of financially competitive and in-demand near-zero-emissions primary steel.

Continued reinvestment in existing fossil-based production technologies will put US steel producers at risk of becoming noncompetitive in a market with increasing demand for lower-emissions products. Investments in near-zero-emissions steel technology will not occur if the legislative and regulatory environment remains status quo. The build-out of upstream and downstream infrastructure requires political and financial support from individual states and collaborative efforts across the region. The potential for the Great Lakes to continue to lose its steel production share to other regions in the country and overseas is very real and should be top of mind for policymakers and EDOs in these states.

States must develop regional and comprehensive implementation plans for the steel industry to align steelmakers’ efforts to maximize federal funding uptake, tailor financial mechanisms to scale and complement federal support, and set up Buy Clean programs to provide reliable and strong demand over time. For enabling technologies, states should understand their specific regulatory landscape to establish the foundations of hydrogen and carbon capture development. Hydrogen will need to be produced and utilized in the Great Lakes at a scale not seen today. This will require significant growth throughout the hydrogen supply chain from equipment manufacturers to storage specialists.

Local investments targeting the hydrogen industry will help make the Great Lakes a leader in the industrial decarbonization space, but production methods must be reviewed in depth when determining the emissions reduction potential. CCS systems will also require regional infrastructural support and supply chain investment. The transmission and storage of captured carbon will need to be regulated and monitored closely. Capture systems must achieve high capture rates, and their contributions to upstream methane leakage must be minimal to help produce the low-emissions steel products buyers are seeking and standards makers are prioritizing. Renewable energy will also play an important role. States must establish bold targets and streamline the permitting process to unlock clean capacity already waiting to get connected to the grid in addition to the continuation of new asset construction.

Caring for the workforce and individual communities that have long supported the steel industry will be essential to ensuring steel production remains prevalent in the region. A transition to DRI steelmaking offers a reprieve from harmful air pollution by reducing the industry’s reliance on coal and coke. CCS and hydrogen-based production pathways project to retain steel production employment levels and offer an opportunity to expand if upstream and downstream activities are collocated with steel production. To facilitate the transition, there is a need for funding to support workforce development and educational programs related to the CCS and hydrogen industries.

The time is now. The federal subsidies available to support CCS and hydrogen infrastructure and those specifically designed for reducing emissions from steel production facilities have come with a clock, and it is ticking fast. The demand for low-emissions products is increasing quickly and is already at a point that justifies the construction of full-scale near-zero-emissions production assets. With the federal government doing its part to incentivize emissions reduction in the steel industry, it is now up to state policymakers and EDO offices to ensure that timely investments are made in the Great Lakes region.

Authors

Lachlan Carey

Manager

Aaron Brickman

Senior Principal

Nick Yavorsky

Senior Associate

Joaquin Rosas

Manager

Chathurika Gamage

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.