Learn how we are working to transform how we use and produce energy.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

The design and rules of wholesale, retail, and local electricity markets impact which, when, and how resources are purchased, sold, and utilized by system operators. Markets can generate efficient pricing for energy, capacity, and other ancillary grid services. Today, expanding and maturing markets are supporting investment in generation and grid infrastructure, putting new stress on the economics of coal, and improving the economics of renewables. In response, market parameters are evolving to support electricity reliability and affordability as systems accommodate higher levels of variable and distributed energy resources.

Through research and interviews with experts around the globe, RMI has compiled examples and data to describe how power sector leaders are leveraging market structures to make progress on energy transition priorities. Specifically, this report:

- Highlights why innovation in markets is critical to the energy transition

- Explains emerging global trends and associated challenges and opportunities

- Describes how market structures can advance the seven key outcomes for successful global energy transformation

- Articulates the edge of innovation for different countries and where attention is needed most

- Spotlights case studies to better illustrate what is being attempted across the industry and to share the experiences of practitioners

This report is part of RMI’s Global Energy Transformation Guide.

Related Insights

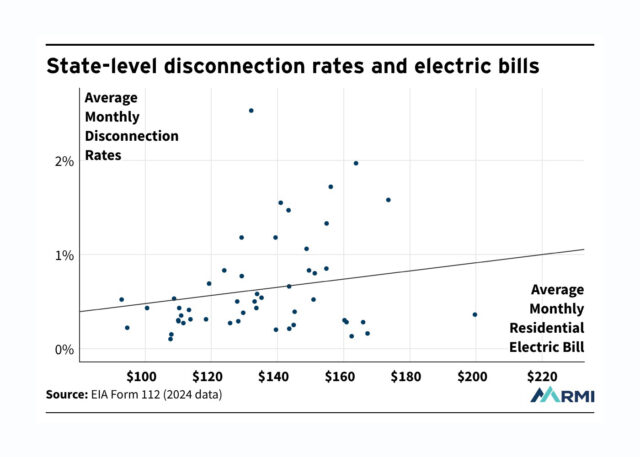

Disconnection Data Is Finally Available. What Does It Tell Us?

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.