Bangui Wind Farm is a wind farm in Bangui, Ilocos Norte, Philippines.

From Theory to Reality: Building Credible Transition Credit Projects

Insights from RMI’s early-stage engagement in coal-to-clean transition credit projects

To connect with our team concerning transition credits, please fill out this form.

Introduction

Power sector stakeholders around the world are exploring options to improve the affordability and reliability of their electricity systems while increasing energy security and promoting economic development and benefits to vulnerable communities. They are finding that transitioning from coal generation to cleaner alternatives is frequently a cost-effective solution that can provide all those benefits while reducing emissions.

Increasingly, corporations and governments are seeking to purchase carbon credits attached to emissions reductions. As such, power sector stakeholders are assessing the role of high integrity carbon credits for coal transition — called transition credits — which can be offered to buyers through existing and planned carbon market channels. Transition credits are intended to generate financial value by monetizing the emissions reductions realized through early retirement and replacement of coal assets with clean energy sources.

In addition to buyer interest in new sources of high integrity carbon credits, the transition credits approach is driven by existing gaps in deploying finance for coal phaseout projects. These projects are often supported in part by concessional finance provided through international initiatives and multilateral development banks. However, this concessional capital is limited, and additional sources of finance are needed to grow the market.

In many emerging markets and developing economies, coal assets are young, profitable, and financed with low-cost debt. This creates a challenge for employing traditional cost of capital levers for coal transition. Under the right circumstances, transition credits can offset the costs associated with retiring a coal asset early while also mobilizing financing for clean energy investments and providing support for communities and workers impacted by coal plant closures.

Despite growing interest in this relatively new form of coal transition finance, early transition credit projects must be tested and rolled out carefully to ensure their high integrity and added value. Careful assessment of pilot projects can be a way to refine existing guardrails that aim to reduce moral hazard (ensuring credits do not inadvertently incentivize minimal action) and establish project additionality (through rigorous baseline setting and granular measurement of actual net emissions reductions and mitigation of leakage emissions — emissions that increase from other sources as a result of increased plant operation from other plants on the grid) while also providing insights into potential replicability and scaling.

Early-stage due diligence and feasibility testing should include: 1) testing the integrity and applicability of transition credits for the pilot project; 2) understanding the need for transition credits while considering other available coal transition mechanisms (CTMs); and 3) assessing the feasibility of transition credits to cover financing gaps associated with coal transition (e.g., early retirement, replacement with clean energy, just transition for communities).

The transition credit pilot currently underway at the South Luzon Thermal Energy Corporation (SLTEC) plant in the Philippines illustrates these steps and has drawn further attention to the opportunity for credits to accelerate the pace of capital mobilization for coal transition.

The SLTEC transition credit pilot, if successfully structured and implemented, could set a powerful precedent for the wider ecosystem. The pilot has the potential to demonstrate practical insights from the transition credit project development life cycle. It can also increase the global dialogue on comprehensive and intentional approaches to just transition planning.

In the spring of 2024, RMI supported the early-stage engagement and pre-feasibility assessment for SLTEC’s transition credit pilot. Using SLTEC as an example, we break down the critical considerations for asset owners interested in moving a transition credit pilot from origination to concept development.

SLTEC: A real-world test case

The SLTEC plant is a 246 MW coal-fired power plant located in Calaca, Batangas, Philippines. The facility comprises two units, with one beginning operations in 2015, and the second in 2016. The Philippines has significant coal-fired capacity on its grid (approximately 60% of its generation comes from coal), and has forecasted a 5.2% annual growth rate in peak electricity demand until 2050.

In November 2022, energy company ACEN completed the world’s first market-based Energy Transition Mechanism (ETM) transaction for the SLTEC coal plant. The deal was driven by ACEN’s ambition to lead in the clean energy transition, as well as investor pressure to prevent ongoing operation of the plant post-divestment. The ETM deal utilized a project sale of the plant into a special purpose vehicle, which facilitated the early retirement of SLTEC to 2040, reducing the plant operating life by 25 years.

To explore the viability of pulling forward retirement 10 years earlier, to 2030, ACEN and the Coal to Clean Credit Initiative (CCCI) announced at COP28 a collaborative effort to explore a transition credit pilot project. For a 2030 closure to be financially viable, three broad buckets of additional costs would need to be assessed against a 2040 baseline:

- Foregone cash flows from the SLTEC plant and other early retirement costs (e.g., decommissioning, contract termination, etc.)

- Additional costs associated with building clean energy replacement required to maintain system reliability on an earlier timeline

- Just transition for impacted plant workers and local communities

From origination to concept

The early-stage assessment of SLTEC and other pilot plants highlights the importance of identifying and addressing project risks up front. Surfacing these risks early is critical not only for the success of individual transactions, but also for building broader market confidence in transition credit mechanisms and their practical use cases.

Early assessment of the opportunity for transition credits can be broken down into four distinct phases (Exhibit 1), structured over a three-to-six-month period. This stepwise approach also helps to provide a replicable framework for evaluating future projects.

Exhibit 1

Phase 1: Project Screening provides a gating assessment of whether the plant has potential for a high-integrity transition credit project. This includes screening against a project-based crediting methodology and understanding the market and owner commitments to coal phaseout. When engaging the asset owner, it is also important to identify project constraints such as the plant’s contractual obligations, utilization dynamics, clean replacement potential, process for engaging the system operator, and applicable carbon market regulations.

If the project appears compatible with the methodology, it moves to Phase 2: Defining Evaluation Scope to understand the potential role for transition credit revenues in supporting early retirement, as well as the clean replacement options that could support the project. The former is done by identifying the categories of costs that would result from the plant’s early retirement. The latter is done by understanding the technical potential of different clean resources, collecting data from existing capacity and interconnection studies, and assessing the maturity of the clean energy market in the country. The output of this phase is a set of scenarios that should be run to quantitatively assess crediting potential, as well as determining any additional studies that might be needed to move forward (e.g., technical studies to identify needed replacement resources, just transition engagements and costing).

Phase 3: Conducting a Pre-Feasibility Analysis focuses on a quantitative assessment of the scenarios identified in Phase 2. The outputs of this assessment will vary on a project-by-project basis, but generally include:

- Baseline retirement date — the counterfactual scenario, or the assumed date that the coal asset would have been retired without the application of transition credits. This is the date against which sales of transition credits can be measured.

- Estimated replacement portfolio timing, size, and costs in an early plant retirement scenario.

- Emissions reduction potential of the project.

- Required revenues and pricing from the sale of transition credits to make the deal financially viable.

A sensitivity analysis of the project’s underlying assumptions is critical in determining how changes in these assumptions might impact the project’s outcome. Examples of sensitivities to run in Phase 3 include:

- Varying coal utilization assumptions

- Different replacement portfolios

- Replacement capital and financing costs

The outputs of this assessment then lead to the Phase 4, where project stakeholders decide whether they would like to proceed to the next stages of project development, including drafting project design documents, engaging buyers, and financial structuring of the transaction.

RMI’s assessment of SLTEC

Using the phases defined above, RMI conducted a pre-feasibility assessment for SLTEC to examine several critical elements of early-stage project validation: eligibility assessment, conservative baseline setting, and quantifying transition credit revenue potential. The outputs of this approach are summarized in Exhibit 2.

Exhibit 2

Phase 1: Project Screening

In the first phase, we conducted a qualitative assessment of SLTEC’s candidacy for transition credits against the CCCI methodology. Our assessment surfaced that SLTEC could be eligible for crediting, as the plant has positive fair value and high existing utilization, and as a relatively young plant, could generate high emissions reductions with its early retirement and replacement with clean energy. The electricity offtaker, ACEN, also has a clear public commitment to decarbonization, a no new coal plant commitment, and commitment to a strong just transition plan.

Phase 2: Defining Evaluation Scope

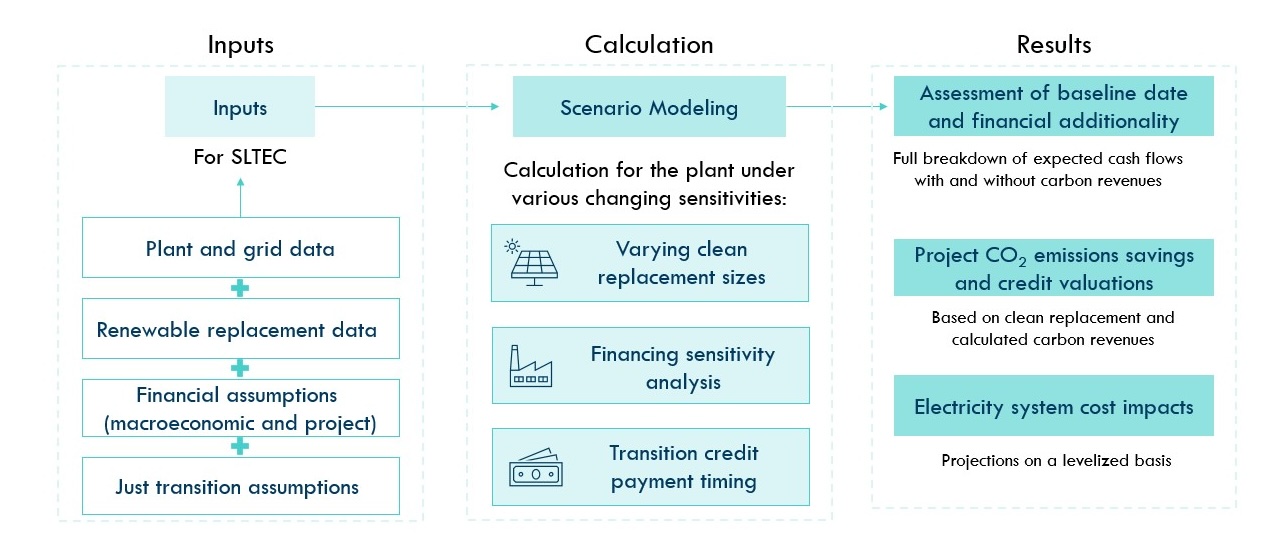

Based on our initial screening, in Phase 2 RMI designed our analysis to consider the role that credits could play under several scenarios, using the below analytical approach:

Exhibit 3

Analytical approach used for RMI’s assessment

RMI Graphic

For any financial shortfall, transition credit revenues were assumed to cover the write-off of any remaining plant value, any financial shortfalls associated with clean energy replacement, and decommissioning and just transition costs for early termination. Over the course of the project, we iterated with ACEN and other partners to define assumptions and sensitivities, including:

- A base case assumption that ACEN would work toward a replacement portfolio of 1,000 MW of solar, 250 MW of wind, and up to 4,800 MWh of battery storage to replace 100% of SLTEC’s business-as-usual output.

- For the remainder of SLTEC’s operating life, ACEN would continue to make full production payments to the SLTEC plant under the existing PPA.

- The replacement portfolio would come online at PPA prices competitive with current auction-based prices in the Philippines, forecasted to 2030 based on expected price decreases.

Using the above assumptions, we would then assess the opportunity for transition credits against a determined baseline date for each project year as early as 2030. This would include the required transition credit revenues and potential emissions impacts, given the assumed clean energy replacement portfolio.

For any financial shortfall, credit revenues were assumed to cover the write-off of any remaining plant value, any financial shortfalls associated with investment in a clean energy replacement, and decommissioning and just transition costs for early termination.

Phase 3: Conducting a Pre-Feasibility Analysis

Our scoping revealed key questions to be clarified through the Phase 3 pre-feasibility analysis, including:

- What would be the most appropriate baseline or counterfactual year to measure transition credit revenues against?

- Given that SLTEC is a relatively young asset, how might undepreciated value and outstanding debt affect the feasibility of earlier retirement?

- What additional termination costs would need to be accounted for in assessing the financial viability of earlier retirement?

- How would different combinations of replacement resources affect SLTEC’s required volume of transition credit revenues and emissions impacts?

Our analysis yielded the following results:

- The current ETM retirement date could be the baseline against which transition credit potential could be assessed. However, this is contingent on the assumed replacement size, financing assumptions, and forward-looking performance of the asset.

- Based on the anticipated timeline for methodology revisions, project design, and commercial implementation, SLTEC could be retired with transition credits as early as 2030.

- The base case renewable energy build could reduce system-wide emissions by up to 19 million metric tons of CO2.

- Based on the above emissions reduction assumptions, breakeven transition credit prices would be in line with market expectations.

- Outcomes proved sensitive to assumed counterfactual utilization of the plant, as well as capital cost, size, and timing assumptions for solar, wind, and battery storage resources.

Phase 4: Recommendations and Next Steps

At the conclusion of the pre-feasibility assessment, RMI presented its findings on behalf of CCCI to ACEN.

RMI recommended three key areas for further stress testing.

- Validation of the 2040 baseline determination via stress testing of key methodological components. The 2040 baseline is highly contingent on cost and sizing assumptions for building a large battery storage asset. The CCCI methodology currently stipulates that the project scenario considers replacement generation from renewable energy only. The case of SLTEC, and the current situation in the Philippines, has indicated that there will be scenarios in which battery storage or other grid reliability measures may need to be incorporated. As a result, additional methodological work may be needed to refine how additionality assessments are performed for battery storage or other flexible technologies, to minimize required credit revenues while still meeting grid reliability needs. The SLTEC project will need to take these uncertainties into account as and when the baseline is assessed after methodology approval by Verra — the standards body that is registering the CCCI methodology.

- Continued assessment of the likelihood of leakage from the clean replacement portfolio. The assumed replacement portfolio for SLTEC is highly ambitious, and will require additional detailed studies on land availability, resource potential, and local and/or regional grid constraints. The base case assumptions assume that the replacement portfolio avoids any project scenario leakage. If this changes in implementation, any subsequent grid emissions leakage would decrease the amount of emissions reductions that can be claimed for transition crediting and thus increase the amount of credit revenues required for deal feasibility.

- Thorough financial analyses to review credit valuation, to consider against market willingness to pay. As a first mover project for transition credits, there is little precedent for how transition credits can be structured to meet project needs while ensuring integrity and ability to be monitored, reported, and verified over the course of the project lifetime. This will require additional thinking on how credit revenues can most effectively be issued into a project’s cash flow, the contractual structure of credit offtake agreements, and mitigation of performance risk via insurance, buffer pools, and other tools.

During the session, the group also discussed various support actors that could continue to work with SLTEC on its transition credit pilot journey.

Looking ahead: Next steps for SLTEC — and the broader market

The CCCI methodology utilized for the SLTEC pilot is undergoing final approval with Verra — a process that includes methodology revisions, audit of the methodology by an independent audit body, and final review before Verra officially registers the methodology. Simultaneously, the ecosystem of actors supporting the SLTEC pilot are completing a project design document (PDD), which describes the transition credit project in greater detail and explains how it meets each of the requirements of the methodology.

ACEN and project partners are also continuing to navigate opportunities to secure offtake from potential buyers. Efforts are moving in parallel to ensure the necessary monetization framework is in place, such as the negotiation of a memorandum of understanding (MOU) in August 2024 between the Philippines and Singapore — a potential offtaker of the project’s credits. This MOU, under Article 6 of the Paris Agreement, would allow for international carbon trading.

Simultaneously, ACEN is engaging with other governments to be a part of the offtake mix, in addition to assessing the potential demand in the voluntary carbon market for corporate buyers to come to the table. The goal is to secure letters of intent from potential buyers in the near term, which will provide the security needed to launch the PDD and move the project toward transaction close. ACEN has also signed an MOU with GenZero and Keppel to jointly explore how transition credits can most effectively be utilized to facilitate project implementation.

Meanwhile, ACEN will continue to focus on coal-to-clean project implementation efforts — including continued refinement of just transition planning. Accelerating SLTEC’s retirement from 2040 to 2030 heightens the importance of ensuring that worker consultations, and any required reskilling efforts, set a positive precedent for other project proponents seeking to ensure that affected communities lie at the heart of coal-to-clean transition planning.

Core lessons for those exploring transition credit projects

Our SLTEC analysis underscores several important considerations for others looking to engage in early opportunity assessments for transition credits.

Commitment to coal phaseout: Credible transition credit projects must demonstrate clear, publicly verifiable commitments from the asset owner. This helps demonstrate that asset owners are serious about coal phaseout and won’t be inclined to continue to build new plants while crediting existing ones. ACEN’s ambitious decarbonization goals and commitment to no new coal have made it a template case for how to help alleviate some of the perverse incentives that carbon markets could face.

Understanding the role of transition credits within a suite of CTMs to instill confidence in the baseline and the project’s additionality: Establishing confidence in the counterfactual scenario (how a coal asset would have operated in the absence of credits) is one of the most challenging aspects of a carbon credit project. One way to address this challenge is for asset owners to consider the suite of other CTMs available to retire coal assets first and see how early retirement can be pulled forward using those mechanisms. In the case of ACEN, the use of the ETM mechanism to bring forward retirement to 2040 helped set a precedent for what was possible in the absence of transition credits — on top of which transition credits could now be layered to incentivize even earlier retirement.

Assessing the feasibility of replacement portfolios against market realities: Achieving commensurate replacement of coal with clean energy at scale is influenced significantly by a variety of factors. Limited land availability can restrict the deployment and potentially limit the amount of energy production potential. Resource potential, dictated by geographic and climatic factors, further influences the feasibility of renewable energy alternatives. Additionally, grid constraints such as insufficient transmission infrastructure or capacity bottlenecks can hinder integration timelines.

Collectively, these factors can limit the speed and extent of commercial implementation, thereby influencing the actual net emissions impacts achieved at the grid level. Addressing these physical and infrastructural challenges is critical to maximizing the emissions reduction potential — and financial viability — of transition credit projects.

SLTEC’s journey exemplifies both the complexity and the potential of creating high integrity transition credit projects. For asset owners and market participants globally, the lessons from SLTEC’s early-stage experience sheds light on what it takes to bridge theory and practice — offering insights the market can use to navigate the complexities in moving from transition credit origination to impactful execution.

If you are interested in learning more about transition credits and their potential applications, please fill out this form.