Learn how we are working to transform how we use and produce energy.

The Five Dimensions of Hydrogen

The who, what, why, where, and when of RMI’s work on clean hydrogen to date.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

In the last year, we’ve seen a flurry of activity in the emerging hydrogen industry, from the establishment of the world’s largest clean hydrogen incentive to the first final investment decisions being made on multi-billion-dollar green hydrogen, green ammonia, and green steel projects. Amid the excitement of the past year, it’s important to remember that hydrogen isn’t just a fad. RMI has been analyzing the alternate energy carrier as a low-carbon energy solution since 2003, building upon the work of RMI Founder, Amory Lovins, to demonstrate why hydrogen will play a critical and substantial role in the decarbonized global energy system.

At RMI, we understand the importance of not leaving any sector behind in the energy transition. To address these needs, we have established a hydrogen initiative in our Climate-Aligned Industries program to promote systems thinking around finding solutions for industrial and heavy-transport sectors. We collaborate closely with our colleagues across RMI to deliver holistic, integrated insights in our analyses and to our partners. Experts from our electricity, transportation, buildings, and finance teams, as well as our Global South, China, India, and US Programs regularly contribute to and review RMI’s hydrogen work, and their perspectives have been vital in developing our broader analyses on the developing global hydrogen industry.

The following breaks down the why, what, who, where, and when of our work on clean hydrogen to date. Through our informed opinion that hydrogen can play a calibrated role in a successful energy transition, we’re turning cutting-edge analytical research into action.

What “Clean Hydrogen” Means

For hydrogen to effectively reduce emissions in heavy industry and heavy-duty transport sectors, its carbon footprint needs to be near zero. We’ve worked to understand the emissions intensity of all types of potential hydrogen production. Because hydrogen produced from natural gas with carbon capture can never be truly net zero, we focus primarily on electrolytic hydrogen production and pathways to scale carbon-free hydrogen markets. We primarily refer to hydrogen as “low carbon” in this piece, to acknowledge that while markets scale, not all hydrogen coming online will be net zero — electrolytic hydrogen produced with grid power, for example, can remain carbon intensive until the grid is fully decarbonized. But ultimately, we’re working to ensure heavy industries and heavy-duty transport can rely exclusively on zero-carbon hydrogen to mitigate their emissions.

To achieve this, we are advocating within leading markets in the EU, the United States, and China, as well as major emerging markets like India, for governments to set stricter standards for defining which fuels count as truly “carbon free.” In the United States, for example, we’ve advocated that electrolytic (or “green”) hydrogen be produced with new, additional renewable energy resources, to ensure expanded hydrogen production will not deplete existing green power resources that are needed to enable direct electrification. We’ve also advocated for robust, detailed monitoring and verification of emissions intensity for hydrogen produced with natural gas via steam methane reforming (“blue” hydrogen), which should account for upstream methane leakage of the gas it uses for feedstock.

We analyze all possible hydrogen production pathways to develop a comprehensive, up-to-date view on expected emissions intensities and costs of different products, and evaluate alternative decarbonization pathways that contrast with hydrogen. In China, we are working closely with the National Standardization Research Institute as well as steel and chemicals industry associations to support policy makers on setting up national standards for hydrogen carbon accounting and promote standards and certification systems for hydrogen produced with renewable energy.

Alongside our analysis of hydrogen’s decarbonization benefits, our research and work with industry also addresses the risks that could accompany wide-scale hydrogen deployment. Scientists are raising concerns about hydrogen’s potential to exacerbate warming by leaking into the atmosphere during production, storage, or transport. We’re taking these concerns seriously by advocating for expanded monitoring of existing hydrogen leakage, as well as for optimal infrastructural planning and robust hydrogen pipeline development that ultimately minimizes leakage.

Some community-based organizations and environmental groups in the United States have expressed concerns about the potential equity, safety, public health, air quality, water sourcing, and environmental impacts of some types of hydrogen projects (e.g., fossil-fuel derived hydrogen and subsurface carbon dioxide sequestration), transportation, storage and other enabling infrastructure (e.g., CO2 pipelines), as well as specific end uses proposed in certain regions (e.g., NOx emissions from hydrogen combustion for power generation).

We take such concerns seriously and push for intentional sourcing, project siting, and efficient water use in our work with project developers to ensure we keep our communities safe and value their health alongside the health of our planet. Based on our experience advising multiple finalists for the $7 billion US Department of Energy’s Regional Clean Hydrogen Hubs Program, we shared best practices and learnings for meaningful, inclusive, and accessible two-way engagement between project developers and local communities to ensure transparency, foster ongoing dialogue, and establish iterative feedback loops to support the development of responsive Community Benefit Plans (CBPs) that center equity and community perspectives across the full lifecycle of clean hydrogen projects to ensure a just, clean energy transition.

Our work on hydrogen comes with an immense amount of responsibility. We aim to ensure that it is scaled effectively and only where needed, demonstrating tangible emissions reduction impacts from day one.

Who Should Use Hydrogen

Most sectors can and should rely on increased energy efficiency and direct electrification to fully decarbonize. Energy and materials efficiency is a strong starting point to reduce demand, and subsequently, emissions. Renewable electricity and batteries can decarbonize our power generation, most of road transport, and residential and commercial heating (together with heat pumps). Further, as battery technologies continue to advance, they could enable the direct electrification of rail transport, trucking, and industrial heating. The research is clear: electrification and improved efficiency will drive the vast majority of global decarbonization.

But there remain some sectors that cannot be easily decarbonized through the above methods, and their associated carbon emissions must be addressed to achieve deep decarbonization. Energy-intensive heavy industry and some long-haul transport sectors like steel, fertilizer, shipping, and aviation rely on high energy density fuels or hydrogen feedstock to maintain their operations. In these cases, green hydrogen, produced via electrolysis with renewable power, is a critical fuel source to enable decarbonization, as corroborated in models published and regularly updated by BNEF, IRENA, the IEA, and the ETC.

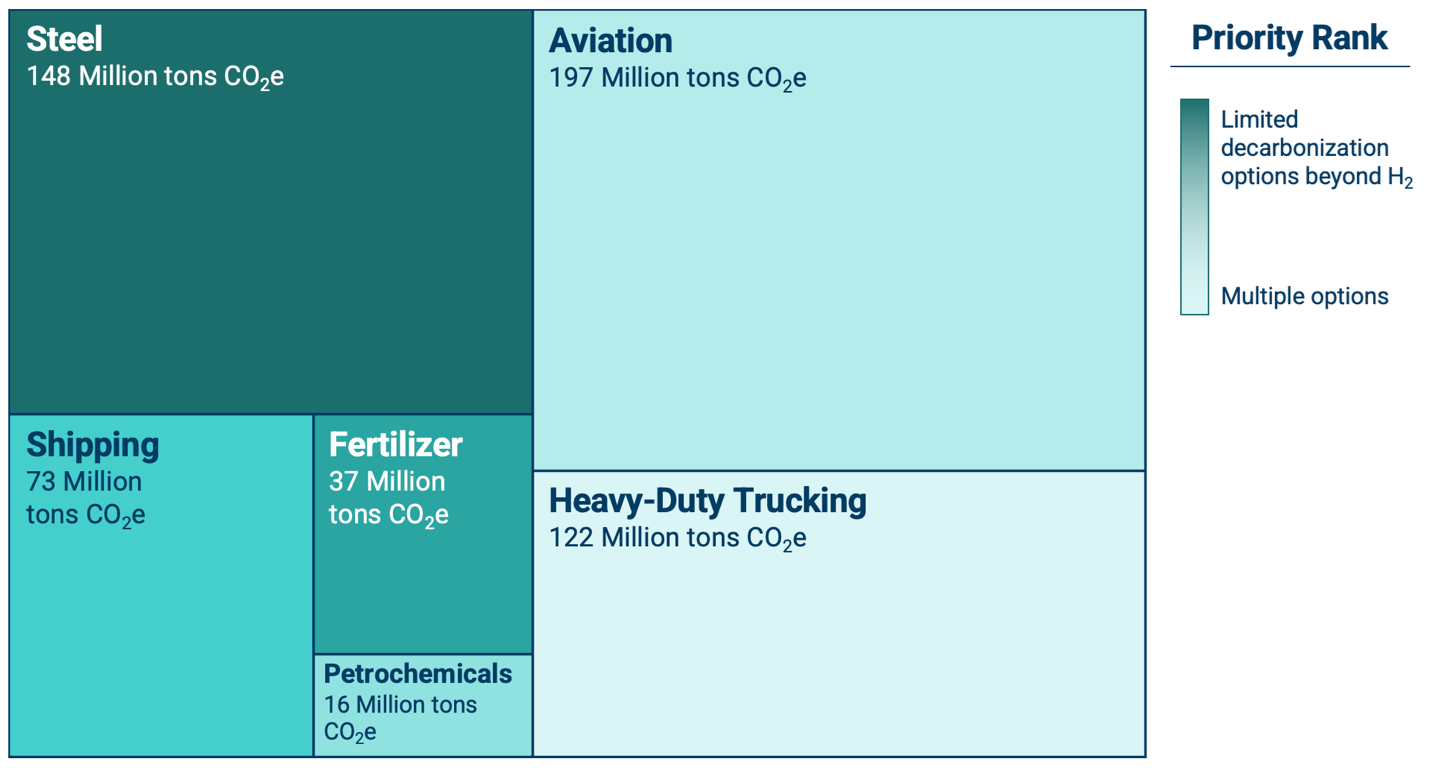

From our research and work with industry, we anticipate that hydrogen-enabled fuel switching will result in the highest emissions abatement in the aviation and steel production sectors, followed closely by shipping, and fertilizer production. There may be a role for hydrogen to play in more challenging market segments of the heavy-duty trucking sector, but this role will be determined by how battery electric infrastructure and technologies develop. Exhibit 1 depicts the scale of expected emissions within the United States and emphasizes which of these sectors have limited alternative decarbonization options beyond hydrogen deployment. By accounting for both abatement potential and availability of decarbonization solutions, we determine which sectors are best suited for wide-scale hydrogen use.

Exhibit 1 – Hydrogen-enabled abatement potential by sector, categorized by availability of alternative decarbonization options (USA example)

Steel

Steel manufacturers can use hydrogen to replace fossil fuels and produce high-quality iron. Green iron and green steel will help reduce embedded emissions in steel-consuming industries like construction, automotive manufacturing, and renewable energy infrastructure. Already, leaps and bounds are being made in the steel sector. At the start of this year, H2 Green Steel, a Swedish startup, raised $6.5 billion to fund the world’s first large-scale green steel plant. Another method of steel decarbonization in the near term involves the use of carbon capture and sequestration, but this is not a zero-emission solution. To realize true steel decarbonization, the future of steelmaking lies with green hydrogen.

We are working with the frontrunners in the steel industry to enable hydrogen-based primary steelmaking. In 2023, the Sustainable Steel Buyers Platform established by RMI and WEF initiated a competitive procurement process open to all steelmakers to deliver sustainable steel to North America. The platform membership aims to have this process result in a collective request for up to 2 million tons of near-zero emissions steel. Leading corporations, including Microsoft, Nextracker, and Trammell Crow Company have joined forces to advance the purchase of inaugural volumes of near-zero emissions steel in North America.

In China, more than $7 billion has been invested into hydrogen-based steel making, with He Steel (a 1.2 million tons DRI pilot), Baowu Steel, Jinnan Steel, and several others implementing successful pilots. RMI China is collaborating with these leading steel making companies and China Metallurgical Industry Planning and Research Institute to identify suitable production lines for using green hydrogen as a pilot. In emerging geographies like India, we have begun the process of charting the course of steel decarbonization through the development of a supply side roadmap and establishing pathways for creating demand through demand-side initiatives like green public procurement.

Chemicals and Fertilizer

Nitrogen-based fertilizers are widespread globally and emit significant amounts of carbon dioxide. To make nitrogenous fertilizers, ammonia needs to be produced, which requires hydrogen. Green hydrogen has the potential to remove carbon emissions from this system. At the same time, because green hydrogen is made via renewable energy, resource-constrained regions that are rich in renewables such as the Global South, can produce their own hydrogen and, in, turn their own fertilizers, improving local food security and reducing reliance on costly imports. This is known as decentralized fertilizer production.

We are working with project developers, local governments, civil society, academia, technology providers, and electric and agricultural cooperatives to enable decentralized models of green fertilizer production in the United States and countries of the Global South. Scaling up this model would allow farmers to move away from the harmful and volatile fossil-based fertilizers supply chain and switch to more resilient and decentralized green fertilizers. Given that many chemical corporations in China have started to pilot green hydrogen utilization, we are also working with China Petrochemical and Chemicals Federation and leading companies on locating possible green hydrogen-based chemical hubs and potential solutions for increasing green hydrogen usage and cost reduction.

Shipping

While inland navigation and shipping across short distances can be electrified, deep-sea shipping — the glue that holds together supply chains and the global economy — is heavily reliant on the dirtiest of all fuels: heavy fuel oil. To balance cost and emissions considerations, shipping companies are starting to procure biomass-blended fuels. Several studies have found, however, that due to limited feedstock and heavy competition with other sectors, biomass-based fuels are likely to play a relatively modest role in decarbonizing the shipping industry.

For the maritime sector to reach net zero, shipping companies need to transition to hydrogen-derived fuel alternatives such as ammonia and methanol. Ammonia produces no carbon emissions and methanol is a net-zero fuel source when sustainably produced. The shipping industry is demonstrating clear interest in ammonia and methanol; there are more than 200 methanol-fueled ships on order and 2023 became the first year of ammonia vessel procurement. This pattern of growth is expected to continue, solidifying hydrogen-derived fuels as the dominant vector for clean shipping.

Over the past couple of years, in close collaboration with Global Maritime Forum and Mærsk Mc-Kinney Møller Center for Zero Carbon Shipping, we have been working on the establishment of several green shipping corridors centered around the use of these hydrogen-based fuels. We have also been collaborating with 20 ports from all over the world under the umbrella of the Shipping Mission Innovation to advise these ports on zero-emission fuel supply strategies.

We are also developing China’s shipping zero carbon transition roadmap by modeling and comprehensive analysis of various shipping decarbonization options, feasibility, and cost-effectiveness. Specifically on green methanol, RMI China is modeling the integration of renewable power generators, hydrogen electrolyzers, and manufacturers to spot optimized points for producing green methanol with minimized costs.

Aviation

Airlines, especially long-haul flight operators, will need clean fuel — Sustainable Aviation Fuels (SAFs) — to replace the fossil fuels they critically rely on. Biofuel-based SAF produced today requires approximately 0.15 kg of hydrogen per gallon of SAF; for e-SAF, which is anticipated to account for nearly 20 percent of aviation GHG reduction by 2050, approximately 2 kg of hydrogen is needed per gallon of SAF production. Therefore, significant quantities of clean hydrogen will need to be produced for SAF alone.

RMI is engaging stakeholders across the aviation sector, including in hydrogen hubs like ARCHES in California, to develop the infrastructure for sustainable fuels and aid in the decarbonization of aviation for years to come. Already, the sector is starting to see big success: this past year, Virgin Atlantic flew the world’s first 100 percent SAF flight from London Heathrow to New York JFK, demonstrating the capability of SAF as a safe replacement for fossil-derived jet fuel. We are also conducting supply and demand mapping to inform SAF consumption and production target setting in China, partnering with manufacturers to establish second-generation SAF pilots, and exploring power-to-liquid SAF possibilities.

Beyond these four sectors, we’re also supporting cross-sector initiatives working to accelerate the deployment of clean hydrogen. Our work with Third Derivative engages hundreds of cutting-edge start-ups, including hydrogen start-ups, in unearthing industrial decarbonization technology and solutions. Leveraging insights from the Sector Transition Strategy reports jointly developed with Mission Possible Partnership, we develop tailored theories of change for engaging with steel, fertilizer, shipping, and aviation players on hydrogen and other solutions, accounting for the varying needs of each sector. Further, as part of our goal to promote decarbonization within hard-to-abate sectors, we work with the United Nations to co-convene and actively support the Green Hydrogen Catapult, a coalition of ambitious project developers determined to scale up renewable fuel deployment globally.

Where Hydrogen Can Be Leveraged

Renewable energy, as a resource, is naturally concentrated in different areas of the world. Regions with limited near-term ability to site, interconnect, and deliver solar and wind should prioritize the use of renewables to decarbonize power production. These regions still need hydrogen to decarbonize industry, illuminating the need for global hydrogen trade. ACWA Power is leading this development, having recently raised $8.5 billion and began the construction of a 2.2 GW project in the desert of Saudi Arabia, with plans to export the green ammonia to renewables-constrained Europe.

Hydrogen-based products’ seaborne trade provides an opportunity for countries with abundant renewables to trade their locally produced green hydrogen with countries that require green ammonia to produce fertilizers or green iron to produce steel. Pure hydrogen trade will also take place, but mostly among countries connected by pipeline infrastructure. Many developing nations can capitalize on this opportunity — giving their economies a path towards reindustrialization and green industrialization through the development of their renewable markets — while providing energy security and decarbonization abroad.

This strategy is already recognized by major economies. Japan and South Korea have identified hydrogen and its derivatives as critical components of their decarbonization strategy, with an emphasis on imports. The European Union has set a green hydrogen import goal of 10 million tons per year by 2030, with individual EU countries signing bilateral agreements with nations across the globe including those within the Global South to collaborate on hydrogen and its derivatives trade. By importing hydrogen, the EU will be able to decarbonize industry without jeopardizing its ambitious direct electrification targets, while providing value to economies positioned to grow rapidly within the renewable landscape.

RMI has taken a forefront role in the development of hydrogen derivatives trade as a partner of the United Nations High-Level Champions in the establishment of the Green Hydrogen Catapult. The convening of this coalition of first movers sets the groundwork for an expansion of trade into other economies by demonstrating that hydrogen trade is a reality and will be a powerful tool for deep decarbonization and providing greater energy security for regions in need.

When We Need Hydrogen

We need hydrogen now, and we need it clean and at scale. We’re at a stage in the global energy transition where it’s crucial for steel makers, fertilizer producers, shipping companies, and airlines to transition away from fossil fuels and reduce their emissions. Many will need clean hydrogen to do so, and luckily, hydrogen project developers are scaling their ambitions to meet this need. A few years ago, the largest hydrogen facility under construction was 20 MW in capacity. Today, several 100-250 MW projects are under development, and visionary first-mover developers including ACWA Power and H2 Green Steel have taken final investment decisions on GW-level renewable hydrogen production facilities.

While supply grows, demand for clean hydrogen also needs to visibly increase. In the last year, RMI has focused on growing supply and demand in tandem; we launched the Sustainable Steel Buyers Platform, which connects committed companies around the US who need low-emissions steel with sustainable steelmakers, piloted a Maritime Book & Claim System, stimulating the uptake of clean shipping fuels, and initiated the sustainable aviation fuel certificate (SAFc) registry through the Sustainable Aviation Buyers Alliance (SABA), enabling the decarbonization of aviation.

Our work is focused on creating enabling environments in which these critical new projects can succeed. As the transition advances — and as renewable power expands and battery technologies scale — we’ll continue to calibrate our analyses and engagements on hydrogen in sectors such as heavy-duty trucking and use cases such as dispatchable power to ensure that clean fuel can strengthen resiliency in industries that electrification and power storage can’t meet alone.

Growing a clean hydrogen market is hard and complicated. But clean hydrogen is also an integral part of RMI’s mission: to transform the global energy system. Our work on scaling this zero-carbon molecule builds on an RMI legacy of not shying away from a challenge, but instead heading straight toward the decarbonization solutions that we need to deploy at the speed required to protect our planet from climate change.

Authors

Oleksiy Tatarenko

Senior Principal

Aparajit Pandey

Principal

Patrick Molloy

Andrew Chen

Principal

Quailan Homann

Senior Associate

Mark Dyson

Managing Director

Zhe Wang

Principal

Hadia Sheerazi

Natalie Janzow

Charlotte Emerson

Jagabanta Ningthoujam

Dave Mullaney

Related Insights

Advance Market Commitments Today Can Build a Low-Carbon Tomorrow

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.