Learn how we are working to transform how we use and produce energy.

Reality Check: COVID, Not Clean Energy, Drove Rise in Electricity Burden

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Despite claims that the growth of clean energy has caused more burdensome electric bills, a new look at utility data suggests that COVID-related factors, not the changing energy mix, drove 2020 increases in electricity burden for US customers. In fact, customers of the utilities that increased their clean energy generation the most in recent years have consistently benefited from lower-than-average electricity burden.

These insights are among the key trends we’ve identified by analyzing new data in RMI’s Utility Transition Hub on the finances, operations, and emissions of vertically integrated investor-owned utilities, or “regulated utilities.” The data, which covers all of 2020, became fully available in fall 2021 and provides a look at how the regulated utility sector is changing—and there are signs that utilities are progressing toward energy transition.

This blog examines three trends with big implications for how regulated utilities move forward with decarbonization:

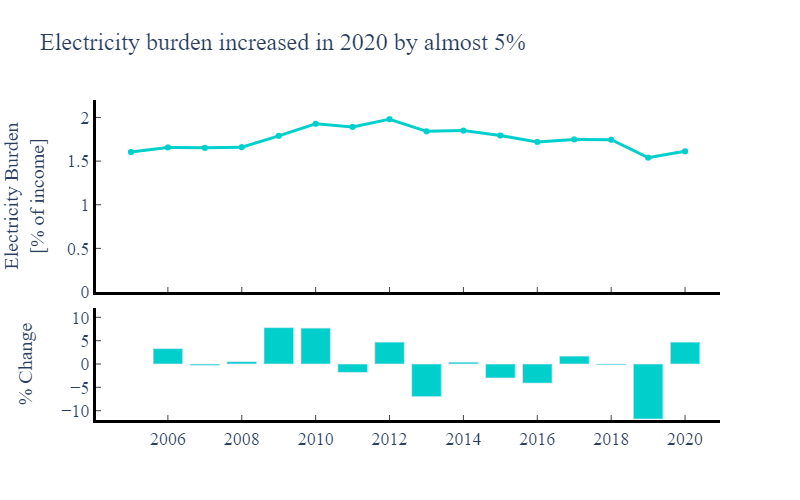

- As a result of income and demand effects of the COVID-19 pandemic, regulated utility customers faced a 5 percent increase in energy burden from electricity costs, the largest increase since 2012.

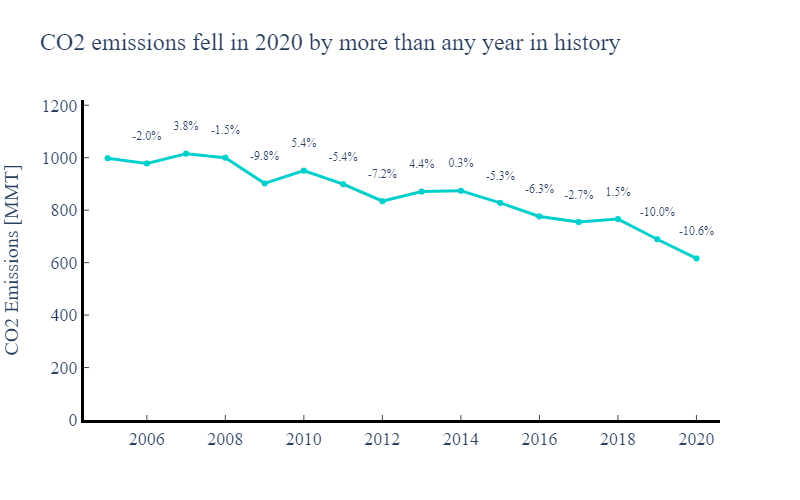

- CO2 emissions dropped by nearly 11 percent, a record decline across the regulated utility sector, due primarily to a decrease in generation from coal-fired power plants—but this dramatic decline was due in part to reduced demand for electricity during COVID-19 lockdowns and may not be persistent.

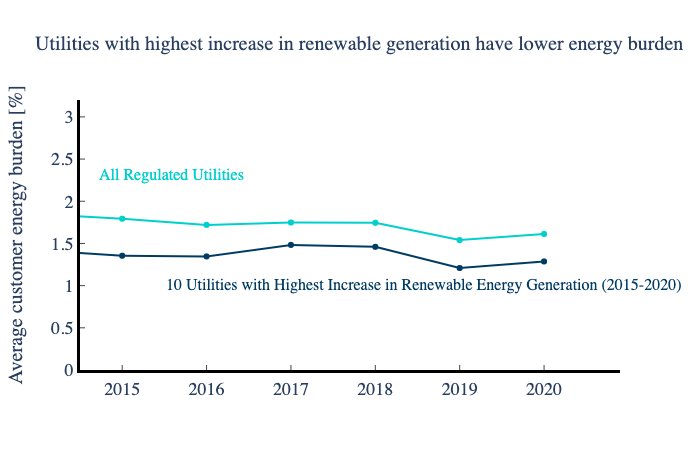

- Regulated utilities invested a record $7.8 billion in wind and solar, and clean investments outpaced fossil investments for the first time. Customers of the utilities that increased their renewable energy generation the most enjoyed lower-than-average electricity burden.

In this blog, RMI’s Utility Transition Hub team dives into the data to understand these trends and assess how new policies might change the way that trends play out in the future.

COVID Causes Biggest Electricity Burden Increase in Eight years

The COVID-19 pandemic significantly impacted electric utilities and their customers in 2020. In some countries, electricity demand fell by as much as 20–30 percent in a month during periods of full pandemic lockdown. In the United States, overall electricity consumption decreased by 4 percent from 2019 to 2020. However, residential electricity consumption grew by 2 percent as lockdown restrictions kept people at home during the day.

COVID-19 also had a negative impact on household income. The median household income dropped by 2.9 percent in 2020—the first statistically significant decline observed since 2011. The combination of increased residential electricity use and lower median household income was felt by regulated utility customers. Electricity burden—the percentage of household income that goes toward electricity costs—increased by 4.7 percent for residential customers. Customers in the lowest income bracket were hardest hit, experiencing a 7 percent increase in electricity burden.

Source: Utility Transition Hub

2020 was also a record year for wind and solar investment for regulated utilities, as outlined below. While energy burden increased for the average household, increased renewable energy investments did not drive this negative customer impact. In fact, residential customers of most of the utilities that have had the largest increase in renewable energy generation over the past five years have had lower electricity burden than the sector average. We expect increased renewable energy use to help moderate household energy burden over time, as utility bills become less impacted by volatile fuel prices.

Note: The 10 utilities with the largest increase in renewable energy generation from 2015 to 2020 are the following, which excludes utilities that had very low (below the 50th percentile) renewable energy generation in 2015: Florida Power & Light, Interstate, Northern State Power (MN), MidAmerican, Consumers, DTE Electric, PacifiCorp, Puget Sound Energy, Portland General Electric, and Minnesota Power.

Source: Utility Transition Hub

Record Drop in Emissions

Regulated utilities have a central role to play in meeting the United States’ national decarbonization goals. However, regulated utilities, along with other electric utilities in the United States, have been slower to adopt low-carbon technologies when compared with independent power producers (private, non-utility entities that sell electricity into the grid). In 2020, regulated utilities generated 33 percent of the electricity produced in the United States, but they were responsible for 42 percent of US power sector emissions.

The global power sector experienced a record drop in CO2 emissions in 2020, and regulated US utilities were no exception. Emissions from regulated US utilities dropped nearly 11 percent from 2019 to 2020, which was the largest year-on-year decline since at least 2005. Some of these reductions were caused by reduced demand for electricity, as generation from utility power plants dropped 3.5 percent.

Source: Utility Transition Hub

But reduced demand is not the biggest part of the story. In 2020, utilities reduced generation from coal by a whopping 18 percent compared with 2019. This drove the sector’s emissions intensity down nearly 8 percent, from 0.51 metric tons of CO2 per megawatt-hour (MWh) to 0.47 metric tons per MWh.

Coal’s dramatic decline was interrupted in 2021. Using preliminary data, the US Energy Information Administration (EIA) recently predicted that coal-fired power generation in the United States would increase by 22 percent in 2021 in response to rebounding electricity demand and high natural gas prices. As a result, CO2 emissions will likely increase too. However, EIA predicts that electricity generation from coal will resume its decline in 2022 as gas prices stabilize and coal plant retirements continue. 2021 may end up as a one-off spike for coal generation and CO2 emissions in an otherwise persistent sector-wide decline.

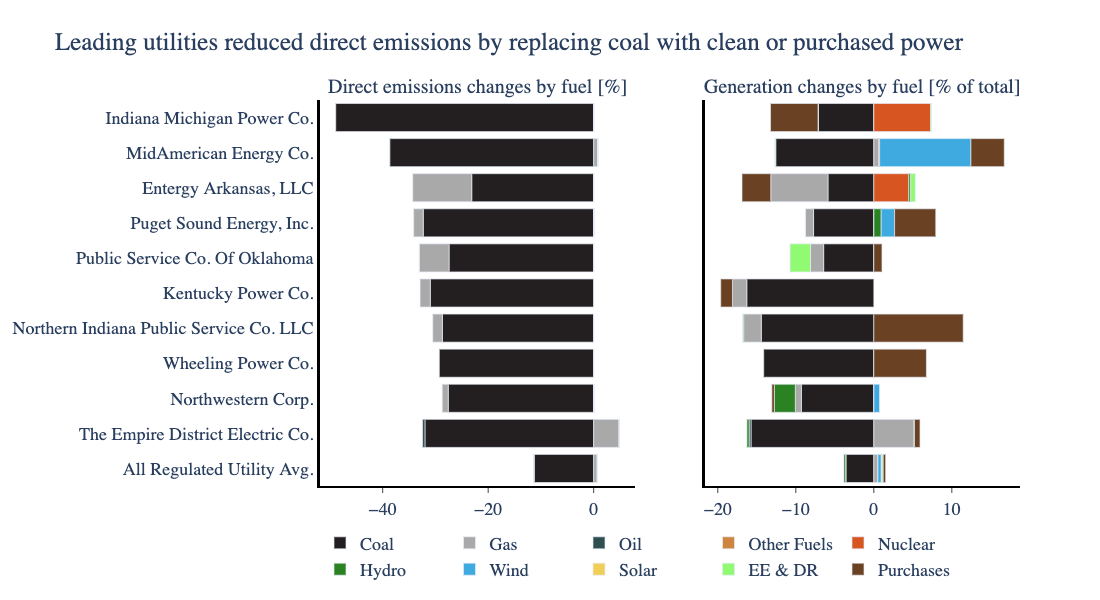

In 2020, utilities replaced their coal generation with a combination of natural gas, nuclear, and wind. Electricity from gas-fired power plants increased from 39 percent to 42 percent, and gas continued to make up the largest share of the sector’s generation. Utilities also replaced their coal generation with purchased power. The sources contributing to purchased power include a mix of fossil and clean generation. Some utilities purchase power from wind or solar plants to decrease the overall emissions associated with the electricity they provide to customers, but this is not always the case—and it is possible for a utility to reduce its direct emissions while maintaining or increasing its overall emissions with CO2-intensive purchased power. RMI’s Utility Transition Hub team is analyzing the emissions associated with utility purchased power, but this work is not yet complete.

From a direct emissions-reduction perspective, MidAmerican Energy stood out as an exceptional case. In 2020, the company’s generation from coal dropped by 5 terawatt-hours (TWh) (a 40 percent decrease), and generation from wind increased by 5.5 TWh (a 37 percent increase). As a result, direct CO2 emissions dropped 38 percent, or 4.6 million metric tons.

Source: Utility Transition Hub

Utilities Invest Big in Renewables

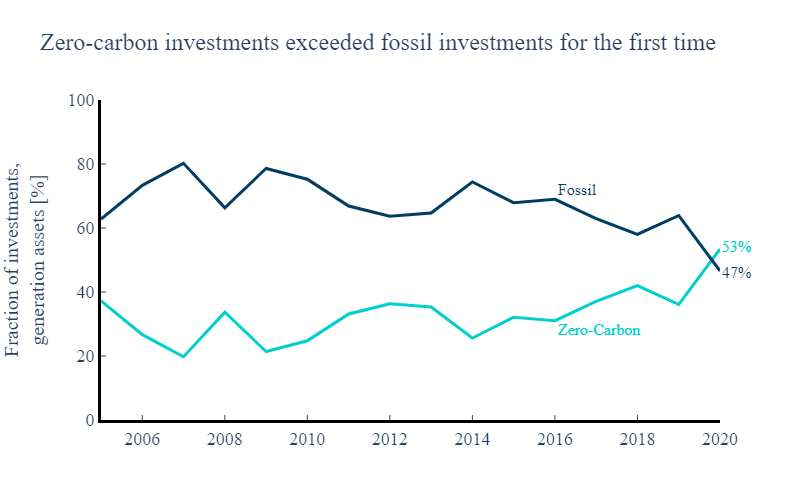

2020 was a huge year for utility investment in renewable energy. For the first time since at least 2005, investment by regulated utilities in zero-carbon technologies exceeded investment in fossil assets (53 percent versus 47 percent). Of the $10.9 billion invested in zero-carbon resources, regulated utilities invested $7.8 billion in 4.5 GW of wind and 1.8 GW of solar, bringing the total wind and solar owned by regulated utilities to 25 GW (an increase of 30 percent for wind and 61 percent for solar).

Source: Utility Transition Hub

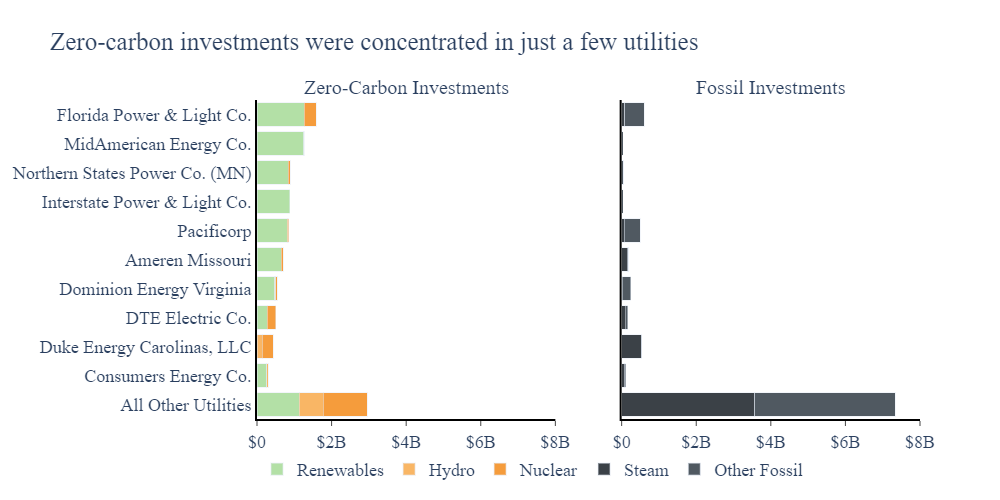

Notably, seven utilities made about 79 percent of the wind and solar investments in the sector. These utilities were already sector leaders that had together made around 64 percent of wind and solar investments in 2019. This concentration of renewable energy investment in the utility sector suggests that, while increased investment is encouraging, we are not yet seeing a sector-wide transition.

Source: Utility Transition Hub

The difference between wind and solar capacity additions (4.5 GW for wind versus 1.8 GW for solar) highlights the continued negative impact on solar deployment of tax normalization rules and the unavailability of the Production Tax Credit (PTC) for solar. Several policy reforms included in the Build Back Better Act, notably direct pay tax credits and the option for solar to claim the PTC, would incentivize wind and solar investments for regulated utilities as well as municipal and rural cooperative utilities. If the Build Back Better Act becomes law, we expect to see a much larger increase in renewables investment going forward.

Despite the growth in renewables, the regulated utility investment story in 2020 was not completely positive from a climate perspective. Though these utilities made record investments in renewable energy, they also invested $9.5 billion invested in fossil assets. Half of this went toward “other fossil” assets, which mostly represents investment in 6.86 GW of new natural gas power plants. The other half went toward “steam” assets—primarily coal power plants—though new investment in these plants was more than offset by depreciation and retirements. The value of steam assets, accounting for depreciation, declined by $2.3 billion, and utilities retired 3.85 GW in coal capacity.

Federal Policy Can Encourage Positive Trends

Regulated utilities in the United States need to accelerate their transition to clean energy for the power sector to meet its climate goals. Federal policy can help. The Build Back Better Act and Infrastructure Investment and Jobs Act both include programs that would help utilities quickly make investments in clean technologies, thereby reducing both their customers’ exposure to fossil fuel price volatility and their overall electricity bills. If Build Back Better passes, over the next decade we expect to see massive utility investment in clean energy, reductions in emissions, and reductions in energy burden.

2020 was a disruptive year for the power sector, and we expect to see even more change going forward. Amid this change, utility stakeholders need granular metrics to distinguish one-off variations from persistent trends. RMI’s Utility Transition Hub, which provides data and analyses about utility finances, operations, and emissions, can help utility stakeholders understand trends in the sector and develop solutions that have lasting positive impacts on the energy transition.

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.