Learn how we are working to transform how we use and produce energy.

Harnessing Carbon Removal Opportunities in Biomass Residue Building Products

How building with renewable, bio-based materials has the potential to scale carbon removal and storage.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Commercial and climate imperatives for integrating carbon removal activities into existing industrial processes and value chains are becoming ever more apparent. Opportunities to integrate carbon removal can help businesses grow and diversify, increase operational efficiencies, and adhere to evolving regulations. Simultaneously, climate stabilization demands rapid, large-scale carbon removal, positioning industries as vital contributors. Forward-thinking industry leaders are beginning to strategically invest in a variety of carbon removal methods that align with their operational capabilities.

This series explores the economic and environmental incentives for integrating carbon removal into the wider industrial landscape. Focusing on specific industries, the reports identify synergies with existing processes, along with the challenges, potential scale, and critical needs to advance opportunities. This report assesses the use of building products produced from residue biomass for carbon removal.

This article is part of a series. To learn more, please see our other articles in this series:

Construction and renovation of buildings account for 34–46 gigatons (Gt) per year (or as much as 75%) of global material flow. [1] Over the past decade, this vast quantity of materials has been identified as a leading contributor to climate change, with the “embodied carbon” emissions associated with harvesting and manufacturing of building products directly responsible for 14% to 21% of global greenhouse gas emissions.[2] Global efforts to measure and reduce these embodied carbon emissions using life-cycle assessment (LCA) have led to mitigation strategies which are now being adopted by municipal, state and federal governments as well as corporations.[3]

As LCA disclosures provide measurement of bio-based carbon flows into products and buildings, they have also led to insights into the potential for carbon storage in building products. Bio-based products from a variety of feedstocks, such as straw, corn stover, perennial grasses, husks and hulls, bamboo, and small diameter wood waste, can be used as both novel and drop-in replacements for building products. These bio-based materials can be used throughout a building, including structural components, insulation, exterior cladding, ceilings, floors, interior walls and partitions, millwork, and finishes (see Exhibit 1).

Exhibit 1: Examples of biomass-based materials that can be used throughout building construction and finishing

In 2023, the United Nations Environment Program recognized that “renewable, bio-based building materials have a unique capacity to drive reductions in atmospheric carbon, if they are sustainably sourced and managed.”[4] In particular, the UNEP report identifies existing residue biomass, such as agriculture and forestry residues, as the most promising source of globally significant, bio-based carbon dioxide removal (CDR) for buildings.

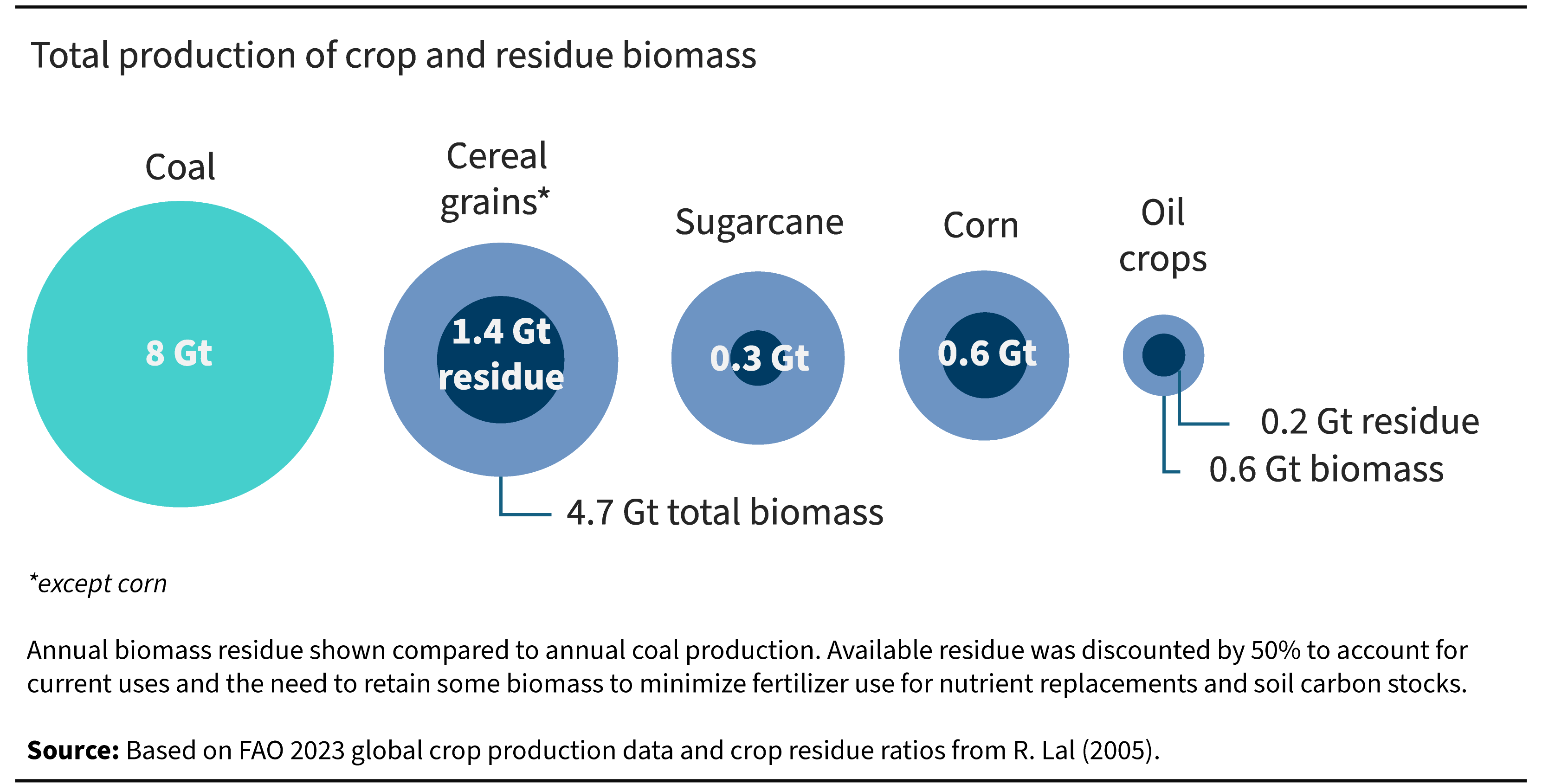

Globally, 3.34 Gt of residues accumulate annually from cereal crops alone, 50% of which is currently burned or rotted.[5] The analysis performed for this report focuses on those feedstocks and products that can be made from regional variations of these materials along with waste stream fibers such as from cellulose insulation, wood fiber insulation, and biochar. The feedstocks for building products are many and varied, as are the product types that can be made from each. Individually, few biomass feedstocks or product types could be a major source of carbon removal but together they represent a massive opportunity, shown in Exhibit 2 as compared to coal production for scale.[6]

Exhibit 2: Annual biomass residue production

Typically overlooked as a pathway for carbon removal, there are many reasons why this option may be an outstanding candidate to achieve affordable and significant quantities of carbon removal in a short amount of time, given its many synergies between agriculture, forestry, and the buildings industry:

- Carbon removal in bio-based building products could rank among the least expensive options to remove and store carbon because it includes inputs into a product (i.e. the building) that is already in high demand— investments in new buildings and retrofits reached approximately $9.7 trillion in 2022. [7],[8]

- Existing quantities of feedstocks for the products considered in this analysis are already produced globally. Productive use of many of these feedstocks carries additional benefits beyond carbon removal, including increased revenues for farmers and the establishment of small- and medium-sized manufacturing opportunities (especially in rural areas).

- Using residue biomass also avoids damaging practices such as burning crop stubble and forestry slash, leaving residue to decompose (which requires significant amounts of water and produces methane), or other environmentally damaging waste management practices. However, this must be balanced with the total removal of nutrients from the soil when waste biomass is taken away from the fields or forests where it was produced.

- No new land conversion is required for sourcing building materials.

- The technological know-how to manufacture carbon-based building products at scale already exists, and investments required for additional capacity are for proven processes that are already practiced.

- Buildings are a highly regulated industry, and existing permitting and insurance tracking enables the monitoring of carbon storage entering and leaving the built environment with little additional administrative burden.

- Buildings are valuable long-lived assets, with most building types estimated to have service lives of 60 years. In practice, many buildings last far longer than this, because of the value they represent to society. This makes building materials a good candidate for secure, long-term terrestrial carbon storage.

Potential scale of carbon removal and storage in buildings

Our estimates of carbon removal potential in buildings are based on models of five different building types, including low- and mid-rise residential, high-rise residential, low-rise commercial, mid-rise commercial, and high-rise commercial.[9] They were created in a life cycle assessment software called BEAM, chosen for its inclusion of biogenic, or biomass-based, building products.[10]

A baseline model was created using typical building products to establish a baseline result, and then products made from biomass residues were substituted into the model to match the performance specifications of the baseline, ensuring like-to-like comparisons. The total net carbon storage value, which consists of the physical biogenic carbon present in the material with all harvesting and processing emissions subtracted, of all bio-based products was divided by the floor area of the model to arrive at a carbon storage intensity. The average intensity of all the building types was applied to projected floor area growth based on estimates from the International Energy Agency (IEA) and multiplied by adoption rates based on historical rates for successful new building products.[11]

The average potential storage intensity is 60.4 kg CO2/m2. When multiplied by assumed adoption rates, the cumulative projected global carbon removal capacity is 3.6 Gt CO2 by 2050, with annual carbon removal rates of 0.26 GtCO2 per year by 2050, shown in Exhibit 3. [12]

Exhibit 3: Carbon dioxide removal in new construction

Avoided emissions

These results do not include any potential emissions reductions achieved by substituting carbon-storing products for more conventional carbon-intensive options. To provide a comparison, BEAM models were adjusted to include embodied carbon results for a typical range of conventional products that would be used in a business-as-usual scenario without the use of any carbon-storing options. The models showed avoided emissions of 144.8 kg CO2e/m2 for low- and mid-rise buildings, 75.9 kg CO2e/m2 for high-rise, with an average averted emissions of 103.46 kg CO2e/m2. [13] The total of 16.5 Gt CO2 of averted emissions by 2050 (0.64 G t CO2 per year in 2050) is nearly 2.5 times as large as the net carbon removal impact. This volume of avoided emissions is an appreciable co-benefit of building related carbon removal efforts.

Limitations of results

These results for carbon removal in buildings using non-timber biomass materials are likely to significantly underestimate the total carbon removal potential in the building sector. The models created for this study only include currently available products that have at least one available Environmental Product Declaration (EPD) per product type and for which there is enough feedstock to supply the assumed demand. [14] Limiting the study to today’s products with standardized EPDs dismisses a sizable variety of additional feedstocks and product types, including:[15]

- Products that don’t currently have EPD data but are made from widely available feedstocks (such as rice hulls, corn stover, and sugar cane bagasse) could feasibly provide double or more the carbon removal potential calculated in this analysis. (For relative biomass volumes, see Exhibit 2.)

- Additional carbon-storing products are being developed using new or emerging feedstocks, including algae, mycelium, microbial excretions and food wastes.

- Mass timber and bamboo products were not included due to uncertainty regarding methodologies for estimating the net carbon storage benefits of wood construction (see Stabilizing Forest Carbon with Wood Construction, below).

- Carbon-storing cement and concrete products were not included because no EPD data is currently available for the limited number of products on the market.

Stabilizing Forest Carbon with Wood Construction

Forests store about 860 gigatons of carbon, making them the largest land-based biological carbon pool. 42% of this carbon is stored in living biomass, 8% in dead wood, 5% in litter, and 44% in soils. Forests absorb a net 7.6 Gt CO2 annually.[16] Wood is roughly 50% atmospheric carbon by mass, sequestered over the lifetime of a tree via photosynthesis. This carbon is securely retained in dead wood as long as it doesn’t burn or decay. Long-lived products made using wood continue to store this carbon, and an industry which grows trees and processes these into long-lived wood products could conceivably be a net carbon sink. Indeed, some estimation methodologies suggest that harvested wood products may already be responsible for net storage of 335 million metric tons of CO2 per year.[17]

Structural elements make up the majority of the total mass of buildings, likely representing the largest opportunity for carbon storage in buildings.[18] In most buildings globally, apart from residential buildings in North America, this structure is built primarily using steel, concrete, or masonry. Replacing steel and concrete in 90% of new large buildings with cross-laminated timber and other high-performance engineered wood products (collectively referred to as “mass timber”) could result in cumulative storage of as much as 20 Gt of carbon by 2050, a fivefold increase in the carbon storage estimated in this report [19].

It would also save about 2.5 Gt of carbon emissions from new construction, as mass timber structures produce about 50% to 75% less emissions to manufacture and erect than steel or concrete.[20] However, the total climate impacts of wood products supply chains are complex. Some authors argue that the wood harvests for all products between 2010 and 2050 will result in net 3.5 – 4.2 Gt CO2e emissions per year.[21] Their analysis includes estimates of forgone sequestration potential in harvested forests.

Pictured: Miller Gulch Forest after wildfire mitigation thinning. Courtesy of Denver Water. Denver Water's "From Forest to Faucets" program restores forests in the watersheds that supply water to Denver Water’s 1.5 million customer to reduce the risk of severe wildfires. Restoring forests to their historic structure and composition stabilizes these forests' ability to sequester and store carbon in the long-term, in addition to protecting watersheds and reducing wildfire hazards to nearby communities. Using the wood harvested in such thinning projects in long-lived wood building products can maximize the carbon benefits of this type of active forest management.

Although experts disagree on the net climate impacts of conventionally procured wood products at an increased scale globally, there is established agreement on the opportunity for active forest management, including harvest, to play an important role in stabilizing forest health (and carbon) into the future. [22] Climate change increases the risk of “natural” disturbances such as wildfire, pests, and disease in forests.[23] Climate change has already increased the rate of wildfires, which are now responsible for 27% of all forest cover loss globally.[24] Climate change also affects the natural ranges of trees and other forest species, sometimes faster than forests can adapt.[25]

Science-based active forest management, which can include various types of ecologically-motivated selective harvests, planting, and introduction of fuel breaks and other landscape interventions, can improve long-term carbon storage in forests and provide numerous co-benefits.[26] In other words, in a changing climate, forests are not best “left alone.”

Processing wood harvested from resilience-oriented forest management into long-lived building products can improve the health of forests and preserve the ability of forests to continue to provide ecosystem services, especially carbon sequestration and storage. Construction, which moves the most material of any global industry, could be enlisted to selectively remove so-called “liability biomass” from forests (including urban forests) to stabilize the 860 Gt of forest carbon which increasingly faces existential climate threats.[27] Initiatives such as the Climate Smart Wood Group and Climate Smart Forest Economy Program aim to provide methodological clarity to forest managers and those procuring wood products regarding how to maximize the climate benefits of wood construction. [28] Cambium Carbon and other private sector actors aim to create marketplaces to connect liability biomass supply with product demand.[29]

Aside from their role in the global climate, forests provide irreplaceable ecosystem services, such as water, shelter, food, fuel, timber, and livelihoods to billions of people and host 80% of land-based biodiversity.[30] Any industrial strategy utilizing forest biomass for climate benefit must respond to the highly differentiated local conditions of forests and the communities which depend on them. Based on the above estimates, the climate impact of increased use of long-lived wood products in buildings could produce cumulative net storage or emissions potentially on the order of tens of gigatons by 2050. The most significant factor affecting these flows is likely to be how effectively harvests can be used to improve the resilience and health of forests in a changing climate.

Risks and constraints to implementation

The potential scale of carbon removal and storage in building materials provides a tremendous opportunity for the construction industry, but is dependent on overcoming key challenges:

- Carbon tracking and accounting: Carbon accounting along the value chain is a major challenge. Defining the system boundaries may not be straightforward in all cases but is important in attributing climate benefits. Third party standards should be used to ascribe what counts as removals and what counts as lowered emissions, as well as who is entitled to claim such benefits. The use of residue biomass could provide carbon removal credits for agricultural producers or forestry managers, or those credits could be ascribed to the material manufacturers or building project developers, as long as the removals are credited and claimed only once.

- Awareness: The potential opportunity of carbon removal and storage in building materials is often overlooked as a viable solution, but increased awareness in the industry and from consumers can drive demand for suitable products and shape the market.

- Durability: While buildings can be stable, durable sites for carbon storage, the lifespan of products within a building can range from 5–100 years (or more). The fate of stored carbon at a product’s end of life, along with the time between biological capture and possible carbon release, will determine the climate impact of the carbon removal achieved.[31] Existing permitting processes in much of the world can capture critical data about quantities of carbon stored in products, and renovation and demolition permits can enable tracking of carbon leaving a building. As valued assets, buildings affected by unexpected disasters (fires, floods, earthquakes, etc.) are also tracked and quantified. Robust carbon tracking could fit well within existing building policies with minimal additional burden to owners and regulators. The value and assessment of carbon removal in buildings is currently a topic of debate in the EU, and the development of standards will be critical to acceptance and successful deployment.[32]

- End-of-life management: When a building reaches its operational end of life, the materials remain after demolition or destruction. Bio-based materials will decompose under suitable conditions, but options like conversion to biochar and deep burial (also called direct biomass storage) are currently being developed to extend the carbon storage of building products for much longer periods of time.

- Standards and codes: All products considered in this study have met the building code requirements in the jurisdictions where they have been deployed, however new bio-based building products are often met with valid concerns about building code compliance, fire performance, and material durability. All building products must meet stringent testing requirements, regardless of the feedstock source. The array of incumbent bio-based building products (including some forms of timber, cellulose insulation, and linoleum flooring) have demonstrated that appropriate performance requirements can be met, although a broader array of suitable products is highly desirable to enable increased use in architecture and design. Typically, this requires adequate investment in testing and proper training for designers and installers. These are already requirements for any new building products, although many smaller manufacturers may have difficulty with the costs required for testing and EPDs.

- Product costs: The cost of bio-based building products is a leading concern for designers and builders today. Many of the incumbent bio-based building products are cost competitive, with many new entries only fractionally more expensive. Building products can offer very low-cost carbon removal as new products are established and the only additional investment required becomes the fractional green premium.

- Production logistics: Logistics, including storing feedstock residues that are produced seasonally for annual production or using small batch production, are a challenge for early-stage products. [33] It is typical that economies of scale transform new building products into cost-competitive options and can improve logistical efficiency.

- Competing demand for biomass: There are numerous applications for biomass, even waste, to be used for biofuels, electricity, and heat that will compete for the available supply.[34] The analysis of carbon removal potential for agricultural residues and waste stream biogenic feedstocks has often focused on bioenergy with carbon capture and sequestration (BECCS). [35] This entails burning the biomass as a replacement for fossil fuels, then capturing and storing the resulting emissions. Process efficiency requires very homogenous feedstock, reducing risk of competition for suitable biomass.

- Land use: Using building products made with biomass residues from current crop production does not require any changes in land use. This substantially reduces technical, political, and market barriers to using these feedstocks compared to solutions which require conversions of land from one use to another.

What’s needed next

As our analysis demonstrates, a cumulative four Gt of carbon could be removed and stored in buildings globally by 2050. This figure excludes the potential carbon removal derived from many feedstocks and products that do not yet have sufficient data to include in the analysis, nor does it represent another potential 16 Gt of avoided emissions. Updating policy, codes, and standards to appropriately consider bio-based building products is a critical next step to enable this potential.

The development of policy and tools to specifically address the use of bio-based building products is starting to emerge, and includes:

- Two national policies (France RE2020 and Denmark BR18) that incentivize and/or require the use of bio-based building products as part of life cycle assessment requirements.[36]

- Municipal incentive programs in Canada (including Vancouver and Toronto) that recognize carbon storage from residue and waste-stream biomass in LCA calculations used for programs to reduce embodied carbon in buildings.[37]

- BEAM and MCE2, two leading tools for measuring embodied carbon in new homes in North America, that include biogenic carbon storage in their calculations and reporting.[38]

- The forthcoming LEED v5, which has a new suite of credits to encourage and recognize the value of carbon-storing products in new and renovated buildings.[39]

- New standards for measuring embodied carbon from ASHRAE (240p) and RESNET (c1550), which explicitly include biogenic carbon measurement and reporting.[40]

- Recent investment by the US government in the development of carbon-storing building products through recent EPA grants and the ARPA-E Hestia program.[41]

While currently a patchwork of codes, standards, and incentives, these existing policies demonstrate the suite of approaches required to encourage building owners, designers, builders, product manufacturers, and regulators to include robust measurement of carbon stored in building products as a key part of broader decarbonization efforts.

The EU is currently establishing a Union certification framework for permanent carbon removals, carbon farming, and carbon storage in products (the Carbon Removals and Carbon Farming Regulation) and is developing technical advice for certifying long-term biogenic carbon storage in buildings.[42] A draft of the “Technical assessment of certification methodologies for long-term biogenic carbon storage in buildings” was released in 2024 to help establish the means of implementation, including the adoption of EU certification methodologies, third-party verification rules, EU recognition of certification schemes and set-up of EU-wide registry.[43] This effort is seen as an important first step in creating a market for short-term, building-related carbon removal and will provide an important economic incentive for greater use of CDR building products.

Advancing the ongoing policy and economic incentives is essential to realizing the opportunities for carbon removal through biomass-based building materials. Key next steps include:

- Update life cycle assessment standards to align with EN 15804, which requires all biogenic carbon flows and land use and land use change (LULUC) emissions to be included separately in all building product EPDs. This will enable consistent reporting across all products and product categories.[44]

- Ensure that reporting of biogenic carbon flows is included in new policies and requirements for life cycle assessments of buildings and establish guidelines for the inclusion of biogenic carbon storage.

- Ensure new policies requiring embodied carbon reduction allow for stored biogenic carbon to be used to meet required thresholds.

- Work toward standardized methods for valuing carbon storage in building products to enable consistent application of storage time value for crediting removals.

- Support development of innovative products and testing (for thermal, fire, structural, moisture and durability performance, as required by building codes), and create training and incentives for designers and developers.[45]

- Create an international case study library of buildings using significant quantities of biogenic materials.[46]

- Support resilience-oriented forest management and harvest practices to maximize the climate benefits of wood construction.

Appendix: Detailed analysis of carbon dioxide removal and storage capacity

Building Emissions Accounting for Materials (BEAM) software was used to determine carbon dioxide removal and storage capacity in this analysis. BEAM estimates the material quantities required for each product type and applies the Global Warming Potential (GWP) from the Environmental Product Declaration (EPD) of each product to provide a quantity of both emissions and carbon storage in kilograms of carbon dioxide equivalent (kg CO2e) in accordance with ISO Standard 21930 and/or EN Standard 15804.[47] The software tallies all the product-level results to provide an overall result for the building.

In this analysis, products were only considered if the manufacturer’s expected lifespan for the product was between 20 and 75 years (where 75 years is the typical maximum lifespan ascribed in LCA practice, although many buildings have a longer lifespan), as this is a range where the various methods for valuing short term carbon storage ascribe meaningful climate impact.[48]

For this analysis, a representative version of each building type (low- and mid-rise residential, high-rise residential, low-rise commercial, mid-rise commercial, and high-rise commercial) was modeled in the BEAM software.[49] A whole building model was created for low-rise buildings, and a single representative floor of the building was modeled for mid- and high-rise buildings. For each product category represented in the tool, the BEAM model included equal areas of all relevant building products (for example, if five carbon-storing flooring options exist in the tool, each was attributed 20% of the total floor area).

The total net carbon storage value (physical biogenic carbon present in the product minus harvesting and processing emissions) of all bio-based products was divided by the floor area of the model to arrive at an intensity value expressed in kilograms of carbon dioxide storage per square meter (kg CO2/m2).

An adoption rate for bio-based products was chosen based on historical adoption rates for a successful new building product in five-year increments to 2050 of 5, 20, 40, 50, and 70% adoption in all new buildings.[50]

The average intensity of all the building types was applied to projected floor area growth based on estimates from the International Energy Agency (IEA) and multiplied by the adoption rates.[51]

Exhibit A1: Carbon storage capacity of non-timber biomass building materials

The results for carbon removal in buildings using non-timber biomass materials are likely to significantly underestimate the total carbon removal potential in the building sector. The models created for this study only include products available in today’s market that have at least one available Environmental Product Declaration (EPD) per product type and for which there is enough feedstock currently available to supply the assumed demand.[52] Limiting the study to today’s products with standardized EPDs dismisses a sizable variety of additional feedstocks and product types, including:

- Existing products made from available feedstocks that do not currently have EPD data: This includes numerous commercial and emerging products made from abundant feedstocks such as rice hulls, corn cob and stover, sugar cane bagasse, coconut shell, and fiber, and sunflower stalks, each of which is among the highest grossing global crop residues. For each of these feedstocks, a variety of products exist at varying levels of production, and the inclusion of such products could feasibly provide double or more the carbon removal potential calculated in this analysis.

- Carbon-storing products using new or emerging feedstocks, including algae, mycelium, microbial excretions, and food wastes: For each of these feedstocks, new products are emerging and beginning to enter the market, including products that may be able to replace or supplement common structural materials such as concrete and steel. The inclusion of such products could potentially double the carbon removal potential calculated in this analysis.

- Mass timber products: Due to uncertainty regarding methodologies for estimating the net carbon storage benefits of wood construction (see sidebar), mass timber and bamboo were excluded from this analysis. By some estimates, widespread adoption of mass timber could increase carbon storage benefits by as much as five times the carbon removal potential included in this report.

- Low-carbon cement and concrete products: No EPD data is currently available for the limited number of products on the market. However, the potential for carbon removal in buildings increases significantly if emerging developments in carbonated aggregates, new carbon-storing cement formulations, and CO2 injection in concrete can scale and provide verifiable net carbon storage. The quantities of aggregate and cement used in buildings could, if net carbon storage is achieved, eclipse the carbon storage potential of the biomass products in this study, with a potential 14 Gt of CO2 storage per year.[53] This value does not consider the accounting nuances to ascribe credit for removals, but does indicate the potential scale the buildings and construction sectors could contribute to carbon management.

Acknowledgements

RMI would like to thank the following for the contributions to this report:

Simeon Max, Climate-KIC

Naomi Sakamoto, Gensler

Cambium Carbon

Top photo credit: EcoCocon

RMI would also like to acknowledge and express gratitude for funding support from the Grantham Foundation for the Protection of the Environment.

Endnotes

[1] Barbara Plank, et al., “From Resource Extraction to Manufacturing and Construction: Flows of Stock-Building Materials in 177 Countries from 1900 to 2016,” Resources, Conservation and Recycling 179 (April 2022): 106122. https://doi.org/10.1016/j.resconrec.2021.106122; Fridolin Krausmann, et al, 2018a. From resource extraction to outflows of wastes and emissions: The socioeconomic metabolism of the global economy, 1900–2015. Global Environmental Change 52, 131–140. https://doi.org/ 10.1016/j.gloenvcha.2018.07.003.

[2] “Why the Built Environment?” Arch. 2030, January 2025, https://www.architecture2030.org/why-the-built-environment/; and “The Embodied Carbon Challenge,” Carbon Leadership Forum, accessed January 2025, https://carbonleadershipforum.org/carbon-challenge/.

[3] “Policy Tracking Map, Embodied Carbon Policy Toolkit,” Carbon Leadership Forum, accessed February 2025, https://carbonleadershipforum.org/clf-policy-toolkit/.

[4] Biomass residue estimates were determined by applying residue rates from “World crop residues production and implications of its use as a biofuel” to the FAO 2023 global crop production data.

[5] Building Materials and the Climate: Constructing a New Future. United Nations Environment Programme, 2023.

[6] Smerald, A., Rahimi, J. & Scheer, C. “A global dataset for the production and usage of cereal residues in the period 1997–2021”. Sci Data 10, 685 (2023), https://doi.org/10.1038/s41597-023-02587-0

[7] Depending on the definition of system boundaries, carbon removal or storage through building products may not produce saleable CDR credits, but can still provide a mechanism for moving carbon dioxide out of the short carbon cycle. For additional detail on this definition, please see the Seizing the Industrial Carbon Removal Opportunity report or “What is CDR?” by CarbonPlan.

[8] “Global Construction Futures,” Oxford Economics, accessed February 2025, https://www.oxfordeconomics.com/resource/global-construction-futures/.

[9] Low-rise < 3 stories; Mid-rise < 10 stories; High-rise >= 10 stories. The analysis includes the core and shell, the interior partition, and the floor, wall, and ceiling finishes for which bio-based substitutions were calculated and does not include those elements that did not have a bio-based substitute proposed (e.g., wall structure materials).

[10] Building Emissions Accounting for Materials (BEAM) is a free LCA software provided by Builders for Climate Action in Canada and is the only LCA software that applies a consistent evaluation of biogenic carbon in building products, https://www.buildersforclimateaction.org/beam-estimator.html.

[11] For more detail on the analysis and assumptions, please see the Appendix.

[12] “Global buildings sector CO2 emissions and floor area in the Net Zero Scenario 2020-2050,” IEA, updated 1 September 2022, https://www.iea.org/data-and-statistics/charts/global-buildings-sector-co2-emissions-and-floor-area-in-the-net-zero-scenario-2020-2050.

[13] Carbon dioxide equivalent (CO2e) is the number of metric tons of CO2 that are equivalent to the amount of carbon stored in a non-CO2 form within biomass.

[14] Analysis was carried out using UN agricultural statistics from https://dataexplorer.fao.org/ to ensure global feedstocks are sufficient to meet the modeled demand, but analysis was not carried out regionally to match anticipated building floor area growth with available feedstocks.

[15] Additional details on the limitations of the analysis of CDR potential are included in the appendix.

[16] Nancy Harris and David Gibbs, “Forests Absorb Twice as Much Carbon as They Emit Each Year,” World Resources Institute, January 21, 2021, https://www.wri.org/insights/forests-absorb-twice-much-carbon-they-emit-each-year.

[17] C.M.T. Johnston, V.C. Radeloff, “Global mitigation potential of carbon stored in harvested wood products,” Proc. Natl. Acad. Sci. U.S.A. 116 (29) 14526-14531, https://doi.org/10.1073/pnas.1904231116 (2019).

[18] Churkina, G., Organschi, A., Reyer, C.P.O. et al. “Buildings as a global carbon sink.” Nat Sustain 3, 269–276 (2020). https://doi.org/10.1038/s41893-019-0462-4

[19] Churkina, G., Organschi, A., Reyer, C.P.O. et al. “Buildings as a global carbon sink.” Nat Sustain 3, 269–276 (2020). https://doi.org/10.1038/s41893-019-0462-4

[20] “Platte Fifteen Life Cycle Assessment – WoodWorks | Wood Products Council.” 2023. WoodWorks | Wood Products Council. May 17, 2023. https://www.woodworks.org/resources/platte-fifteen-life-cycle-assessment/.

[21] Peng, L., Searchinger, T.D., Zionts, J. et al. “The carbon costs of global wood harvests.” Nature 620, 110–115 (2023). https://doi.org/10.1038/s41586-023-06187-1.

[22] “Forest Europe Workshop Report: Pro-active management of forests to combat climate change driven risks,” Forest Europe, 3-4 September 2019, https://foresteurope.org/wp-content/uploads/2016/08/WS_report_CC_Adaptation.pdf; Todd A Ontl, et al., “Forest Management for Carbon Sequestration and Climate Adaptation,” Journal of Forestry, Volume 118, Issue 1, January 2020, Pages 86–101, https://doi.org/10.1093/jofore/fvz062; Satyam Maharaj and Aurimas Bukauskas, “Fighting Wildfires with Low-Carbon Buildings,” RMI, 2024, https://rmi.org/app/uploads/dlm_uploads/2024/10/fighting_wildfires_with_low_carbon_buildings_brief.pdf .

[23] Seidl R, et al., “Forest disturbances under climate change,” Nat Clim Chang. 2017 Jun;7:395-402. doi: 10.1038/nclimate3303. Epub 2017 May 31. PMID: 28861124; PMCID: PMC5572641.

[24] MacCarthy, J., Richter, J., et al. “The Latest Data Confirms: Forest Fires Are Getting Worse, World Resources Institute,” 2024, https://www.wri.org/insights/global-trends-forest-fires

[25] Messaoud, Yassine, 2024, “Tree Growth in Relation to Climate Change: Understanding the Impact on Species Worldwide.” Forests 15 (9): 1601. https://doi.org/10.3390/f15091601.

[26] Ontl, Todd A, Maria K Janowiak, Christopher W Swanston, Jad Daley, Stephen Handler, Meredith Cornett, Steve Hagenbuch, Cathy Handrick, Liza Mccarthy, and Nancy Patch, “Forest Management for Carbon Sequestration and Climate Adaptation.” Journal of Forestry 118 (1): 86–101, 2019, https://doi.org/10.1093/jofore/fvz062.

[27] “Western US cities combine to combat ‘liability biomass’,” Bioenergy Insight, 2024. https://www.bioenergy-news.com/news/western-us-cities-combine-to-combat-liability-biomass/; Climate Smart Wood Group, https://www.climatesmartwood.net/

[28] Climate Smart Wood Group, https://www.climatesmartwood.net/.

[29] Cambium Carbon, https://cambiumcarbon.com/.

[30] “Forests – a lifeline for people and planet,” United Nations Department of Economic and Social Affairs, accessed February 2025, https://www.un.org/en/desa/forests-%E2%80%93-lifeline-people-and-planet.

[31] In this analysis, products were only considered if the manufacturer’s expected lifespan for the product was between 20-75 years (the typical maximum lifespan ascribed in LCA practice), in the range where the various methods for valuing short term carbon storage ascribe meaningful climate impact.

[32] “Technical assessment of certification methodologies for long-term biogenic carbon storage in buildings,” Carbon Removals Expert Group Technical Assistance, accessed February 2025, https://climate.ec.europa.eu/document/download/cae4eabb-34af-421b-b8ed-42543bf38a1d_en?filename=policy_carbon_expert_tap_buildings_en.pdf.

[33] Wanda Lau, “CalPlant Launches Green MDF Made from Local Agro-Waste,” Architect Magazine, August 7, 2019, https://www.architectmagazine.com/technology/products/calplant-launches-green-mdf-made-from-local-agro-waste_o; and “Calfibre hopes to restart rice-straw MDF plant,” Building Products Digest, June 1, 2024, https://www.building-products.com/calfibre-hopes-to-restart-rice-straw-mdf-plant/.

[34] Kahsar, R., Pike, D., et al., The Applied Innovation Roadmap, RMI, 2023 https://rmi.org/insight/the-applied-innovation-roadmap-for-cdr/.

[35] Chum, H., A. Faaij, et al., 2011: Bioenergy. In IPCC Special Report on Renewable Energy Sources and Climate Change Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA.

[36] The Bio-based Materials Collective is currently working to develop access to regionally produced biomass-based materials, including developing education and regulations.

[37] Product libraries such as 2050 Materials, revalu, and the Carbon Smart Materials Palette provide information on specific products, include bio-based options, but do not specifically provide case studies of deployed materials.

[38] “Réglementation environnementale RE2020,” Ministère de la Transition Ècologique, de la Biodiversité, de la Forêt, de la Mer et de la Pêche, update 10 June 2024, https://www.ecologie.gouv.fr/politiques-publiques/reglementation-environnementale-re2020; “Building Regulations,” The Social and Housing Authority, accessed February 2025, https://www.bygningsreglementet.dk/.

[39] “Embodied Emissions, Stream 2: An applied research project for low-rise homes that minimize embodied emissions,” Near Zero, accessed February 2025, https://nearzero.ca/home/stream-2/; and “Buildings Energy & Emissions,” City of Toronto, accessed January 2025, https://www.toronto.ca/city-government/planning-development/official-plan-guidelines/toronto-green-standard/toronto-green-standard-version-4/low-rise-residential-version-4/buildings-energy-emissions/.

[40] “Introducing the BEAM Estimator,” Builders for Climate Action, accessed January 2025, https://www.buildersforclimateaction.org/beam-estimator.html; “Material Carbon Emissions Estimator (MCE2),” Government of Canada, accessed February 2025, https://natural-resources.canada.ca/maps-tools-and-publications/tools/modelling-tools/material-carbon-emissions-estimator/24452.

[41] “LEED V5,” USGBC, accessed February 2025, https://www.usgbc.org/leed/v5.

[42] “ASHRAE, The International Code Council Completes Draft Carbon Emissions Evaluation Standard,” ASHRAE, published 2 February 2024, https://www.ashrae.org/about/news/2024/ashrae-the-international-code-council-completes-draft-carbon-emissions-evaluation-standard; and “Draft PDS-01 RESNET 1550, Embodied Carbon,” RESNET, accessed January 2025, https://www.resnet.us/about/standards/minhers/draft-pds-01-resnet-1550-embodied-carbon/.

[43] “Summaries of the FY 23-24 IRA 60112 Grant Selections: Reducing Embodied Greenhouse Gas Emissions for Construction Materials and Products,” Environmental Protection Agency, 2024, https://www.epa.gov/system/files/documents/2024-10/2024-epd-grant-summaries-ira-60112-updated-10.25.24snw.pdf; and “HESTIA,” Advanced Research Projects Agency – Energy, 2024, https://www.arpa-e.energy.gov/technologies/programs/hestia.

[44] “Regulation (EU) 2024/3012 of the European Parliament and of the Council of 27 November 2024 establishing a Union certification framework for permanent carbon removals, carbon farming and carbon storage in products,” EUR-Lex, accessed March 2025, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ:L_202403012.

[45] “Technical assessment of certification methodologies for long-term temporary biogenic carbon storage in buildings,” Partners for Innovation & Wageningen University and Research, March 2024, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ:L_202403012.

[46] “Sustainability of construction works – Environmental product declarations – Core rules for the product category of construction products,” CEN (European Committee for Standardization), accessed March 2025, https://standards.cencenelec.eu/dyn/www/f?p=CEN:110:0::::FSP_PROJECT,FSP_ORG_ID:70014,481830&cs=1B6FE860255B200E33E1E2E4B4A540088.

[47] EPDs are governed by ISO Standard 21930:2017, https://www.iso.org/standard/61694.html.

[48] Chilton, K.; Arehart, J.; Hinkle, H. “Evaluating Fast-Growing Fibers for Building Decarbonization with Dynamic LCA,” Sustainability 2025, 17, 401, https://doi.org/10.3390/su1702040.

[49] Building Emissions Accounting for Materials (BEAM) is a free LCA software provided by Builders for Climate Action in Canada and is the only LCA software that applies a consistent evaluation of biogenic carbon in building products. Details at https://www.buildersforclimateaction.org/beam-estimator.html.

[50] Adoption rate is based on Rock Wool mineral insulation, https://www.rockwool.com/group/about-us/history/. They grew their market by 90x from 1960 to 1990 to reach a sizeable market share. From 1990 to 2020, they grew 6x, with the product becoming ubiquitous and new competitors emerging. In this analysis, this was mapped to a 14x growth rate from the initial 5% adoption rate.

[51] Floor area growth rates are taken from IEA scenarios at https://www.iea.org/data-and-statistics/charts/global-buildings-sector-co2-emissions-and-floor-area-in-the-net-zero-scenario-2020-2050.

[52] Analysis was carried out using UN agricultural statistics https://dataexplorer.fao.org/ to ensure global feedstocks are sufficient to meet the modeled demand, but analysis was not carried out regionally to match anticipated building floor area growth with available feedstocks.

[53] Van Roijen, Elisabeth, Sabbie A. Miller, and Steven J. Davis. “Building Materials Could Store More than 16 Billion Tonnes of CO2 Annually.” Science 387, no. 6730 (January 10, 2025): 176–82, https://doi.org/10.1126/science.adq8594.

Recommended Reading

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.