Learn how we are working to transform how we use and produce energy.

Financing Electric Two- and Three-Wheelers in India

Two ways that concessional capital providers can catalyze the Indian electric two-/three-wheeler financing market.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Access to affordable financing is one of the best ways to accelerate the adoption of electric two-and three-wheelers (e-2/3Ws) in India. E-2/3Ws now match conventional fossil fuel vehicles on a total cost of ownership basis, and future adoption trends suggest rapid adoption mirroring an S-curve — a trajectory of growth that shows that the adoption rate of innovations is non-linear — slow at first, then rapidly rising before flattening out again as it reaches market saturation.

A major catalyst driving this growth is the active participation of numerous non-banking financial companies (NBFCs) nationwide. These NBFCs have emerged as primary providers of organized credit to borrowers in the e-2/3W segment. They play a pivotal role in extending loans to low-income individuals new to credit and with limited collateral. Many of these borrowers are actively engaged in the gig economy, offering delivery services, last-mile logistics, and passenger transportation.

However, systemic barriers contribute to the perceived high risks associated with EV lending, resulting in e-2/3W loan terms being 5–14 percent costlier than their gasoline- and diesel-powered counterparts. While NBFCs are committed to expanding financing in the e-2/3W market, which is projected to reach approximately INR3.7 lakh crore (US$44 billion) by 2030, the primary challenge is to make financing more affordable. Below, we describe two ways that concessional capital providers such as multilateral development banks, philanthropists, corporate social responsibility capital and foundations can play a pivotal role in addressing this challenge.

Challenges faced by NBFCs lending to the e-2/3W market

RMI recently collaborated with the Electric Mobility Financiers Association of India, a consortium comprising India’s top 35 NBFCs, to pinpoint their specific hurdles. The foremost challenge highlighted by the group is the steep cost of borrowing faced by NBFCs. Unrated and small NBFCs incur an average cost of capital that is 600–800 basis points higher than banks and investment-grade NBFCs, resulting in elevated interest rates for e-2/3W borrowers.

In addition to the high cost of borrowing, NBFCs must also overcome and manage prevalent EV market risks pertaining to the asset. For one, the lack of an e-2/3W secondary market translates to a virtually non-existent residual value. The product quality and range performance of e-2/3Ws are other concerns. Lastly, as the e-2/3W market is becoming more crowded with many start-ups vying for market share, NBFCs are wary of market failures stemming from defaults by new and unprofitable OEMs, leading to extreme losses for NBFCs.

Furthermore, NBFCs noted a significant gap in borrowers’ understanding of EV products and maintenance, and digital payments exasperating customer risk. While NBFCs have expertise lending to new-to-credit customers and observe that most low-income borrowers do not intentionally default, EVs have a higher default rate due to customers’ lack of familiarity with products and digital payment systems.

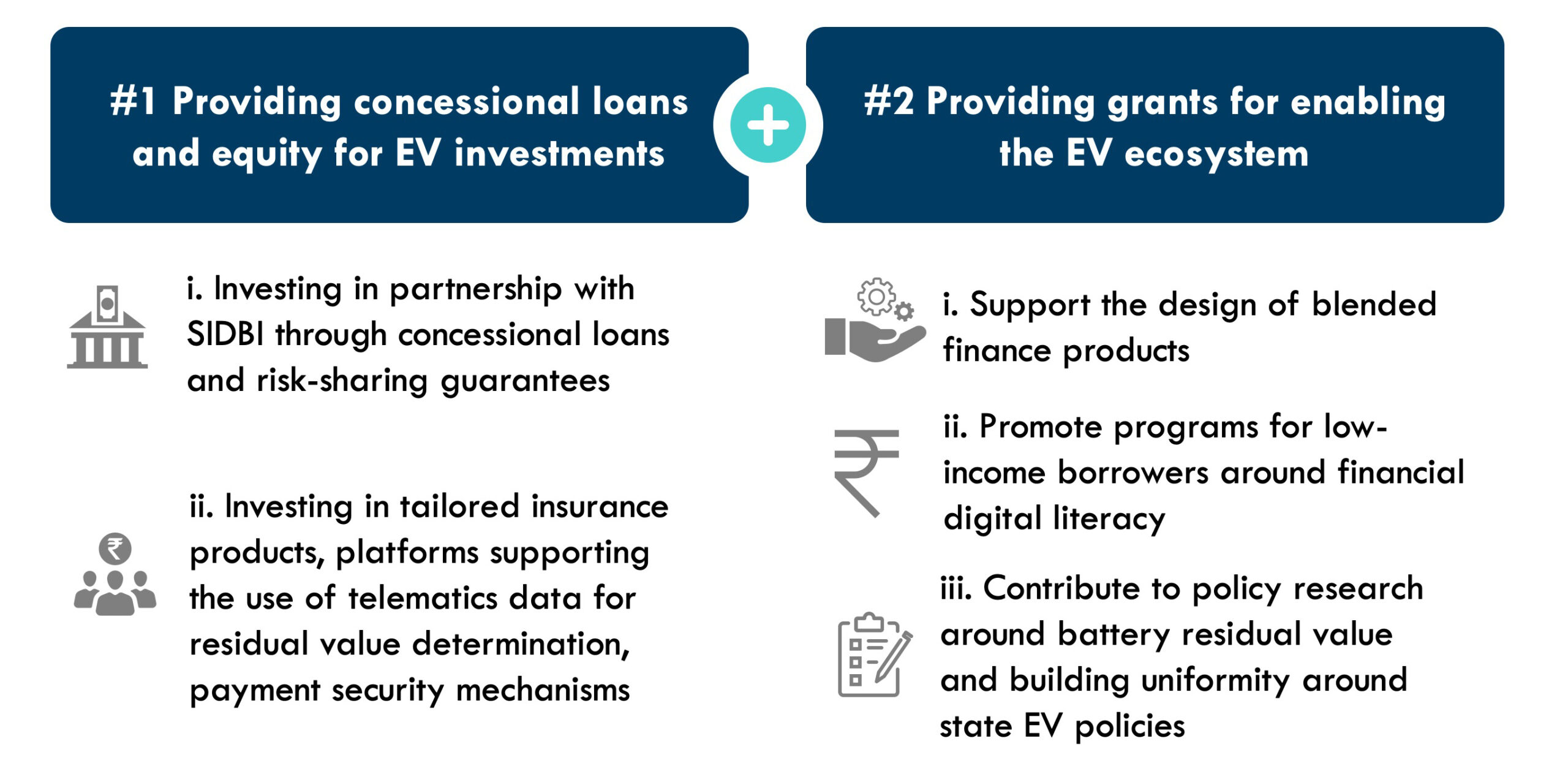

Two ways concessional capital providers can support affordable EV financing

Concessional capital providers play a vital role in fostering affordable lending to e-2/3Ws in the Indian market. Here is how they can contribute:

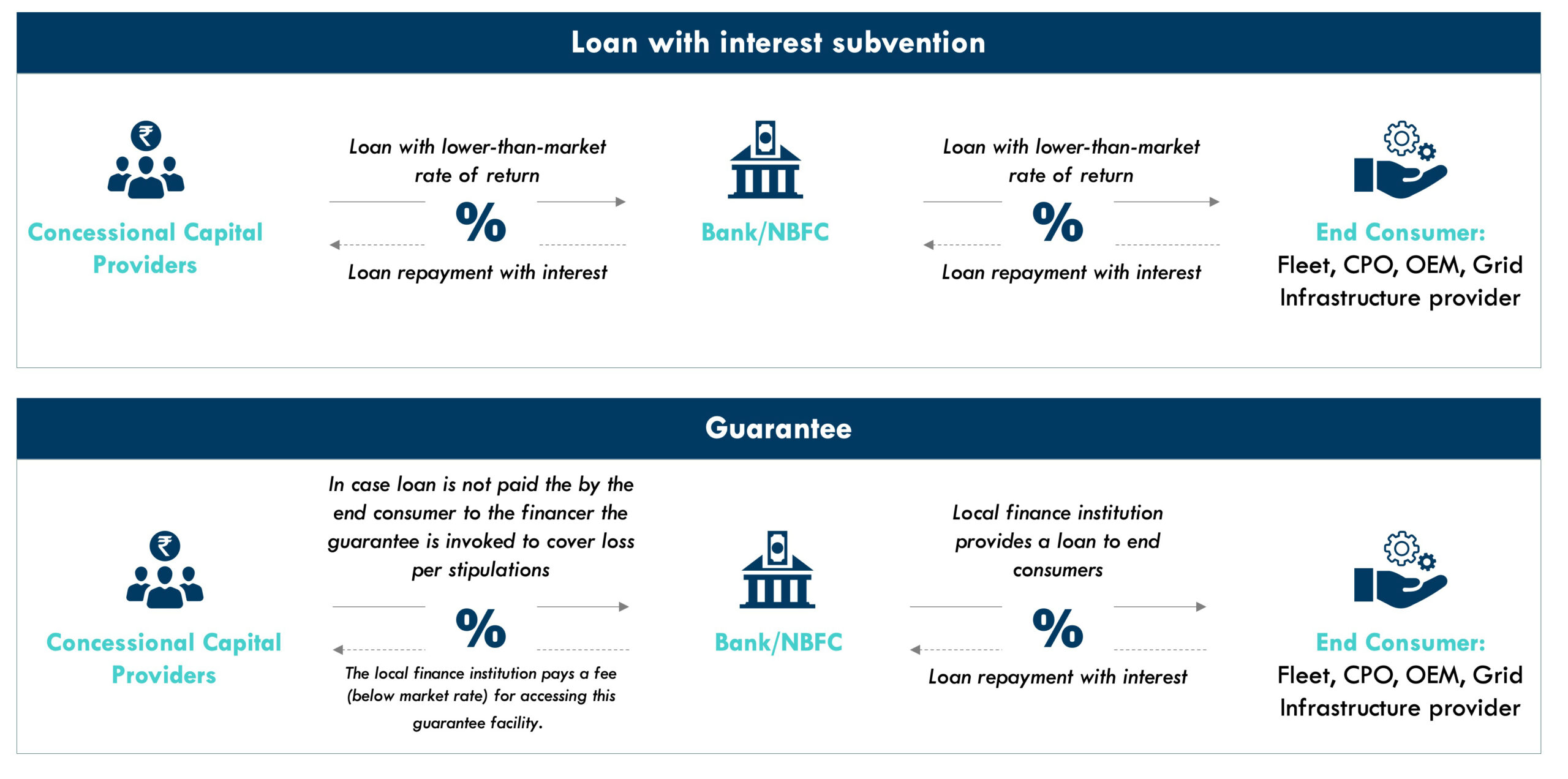

1. Providing concessional capital (i.e., concessional loans and partial risk-sharing guarantees) for blended finance instruments

Concessional capital providers can explore capital directly through concessional loans and partial risk-sharing guarantees to the ecosystem. Concessional loans to NBFCs can reduce the cost of capital and support more affordable lending terms for end consumers. Similarly, partial risk-sharing guarantees can help mitigate the extreme losses financiers face while lending to e-2/3W customers.

In the Indian market, philanthropists can engage directly with institutions such as the Small Industries Development Bank (SIDBI), which offers such instruments to a range of EV financiers and EV ecosystem players, including fleet operators and charge point operators. The Shell Foundation collaborated with SIDBI via a US$6 million risk-sharing facility offering coverage on secondary losses faced by NBFCs. While financial institutions are adept at underwriting the initial loss due to their direct client interactions, governments are often reluctant to assume responsibility for secondary losses. Therefore, philanthropic capital can act as a buffer and be strategically deployed to maximize its impact.

Given the flourishing EV start-up ecosystem in the country, concessional capital providers can also offer concessional equity or debt to start-ups developing open data platforms to build more transparency around battery data. In addition, they can invest via other innovative financial products such as insurance and payment security mechanisms specifically designed for the e-2/3W sector. The implementation of this would include assessing the nature of the underlying asset and its associated risks, particularly its income-generating potential, evaluating the product’s quality and its implications for financial risk, identifying conditions necessary for commercial banks to enter e-2/3W financing, and ensuring compliance with stringent quality standards for financed products.

2. Providing grants for EV ecosystem-enabling activities

If concessional capital providers cannot explore investments in blended finance products and prefer to use grant capital, they can support various ecosystem-building initiatives to create a conducive environment for EVs. The activities supported by grant capital would be different from investments by concessional capital providers, as the intention of the capital is not to seek a return. This can be more flexibly used to mitigate risks associated with lending to e-2/3W customers.

First, organizations can allocate grants to facilitate the design and launch of blended finance products. This involves supporting conceptualization, convening relevant stakeholders to establish a framework, and reaching a consensus on key aspects. Such infusion can help initiate blended finance products in the near term and serve as a blueprint for how they can scale when or if a larger sum of concessional capital from multilateral development banks becomes available.

Second, by offering grants, organizations can assist in developing educational programs aimed at enhancing financial literacy. This includes providing training on the usage of digital finance platforms and promoting understanding of EV products among low-income borrowers. Utilizing corporate social responsibility capital for such initiatives would be catalytic, as it would help achieve green goals and enhance social impact as mandated by law.

Third, concessional capital providers can support policy research focused on developing regulatory guidance for battery life and usage strategies to enhance residual value. Additionally, they can assist state governments in developing uniform EV policies, including the dissemination of incentives. This collaborative effort would enable financiers to deploy their financing schemes more rapidly.

Overall, concessional capital providers’ contributions to shifting the S-curve even by two to three years could have significant societal benefits. Through close collaboration with financiers to address risks associated with EV assets and broader challenges within the EV ecosystem, concessional capital providers can facilitate the realization of short-term benefits of e-mobility. These benefits include enhanced air quality, diminished oil dependency, bolstered energy security, and cost saving for users. Ultimately, this would accelerate India’s transition to decarbonization in the transport sector.

Related Insights

Planning Ahead for EV-Ready Grids Without Leaving Ratepayers Behind

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.