Energy storage power station in the morning

Batteries: The Workhorse of an Affordable, Reliable Grid

Batteries can support grid affordability and reliability — if only grid planners would let them.

This spring, a massive, hours-long power outage across Spain and Portugal disrupted businesses and transit systems and left tens of millions of people without power. In June, Spain’s government released a report that added to the ongoing search for answers post-blackout. The blackout was a complex event, with multiple technical failures, but a key contributor was unreliable voltage regulation of conventional generators cited in both the government’s report and in and assessment by the North American Electric Reliability Corporation (NERC).

Fortunately, solutions are becoming clearer. Both NERC and the Spanish government highlighted an opportunity for more renewable and battery energy storage to provide the types of voltage regulation that could have helped stabilize the grid.

If US grid planners wish to learn from the Iberian Peninsula’s story, there is one resource that has proven it can compete to provide grid stability and affordability at the same time: batteries. Two US markets, California and Texas, offer blueprints for how to do that.

Enhanced stability at lower costs

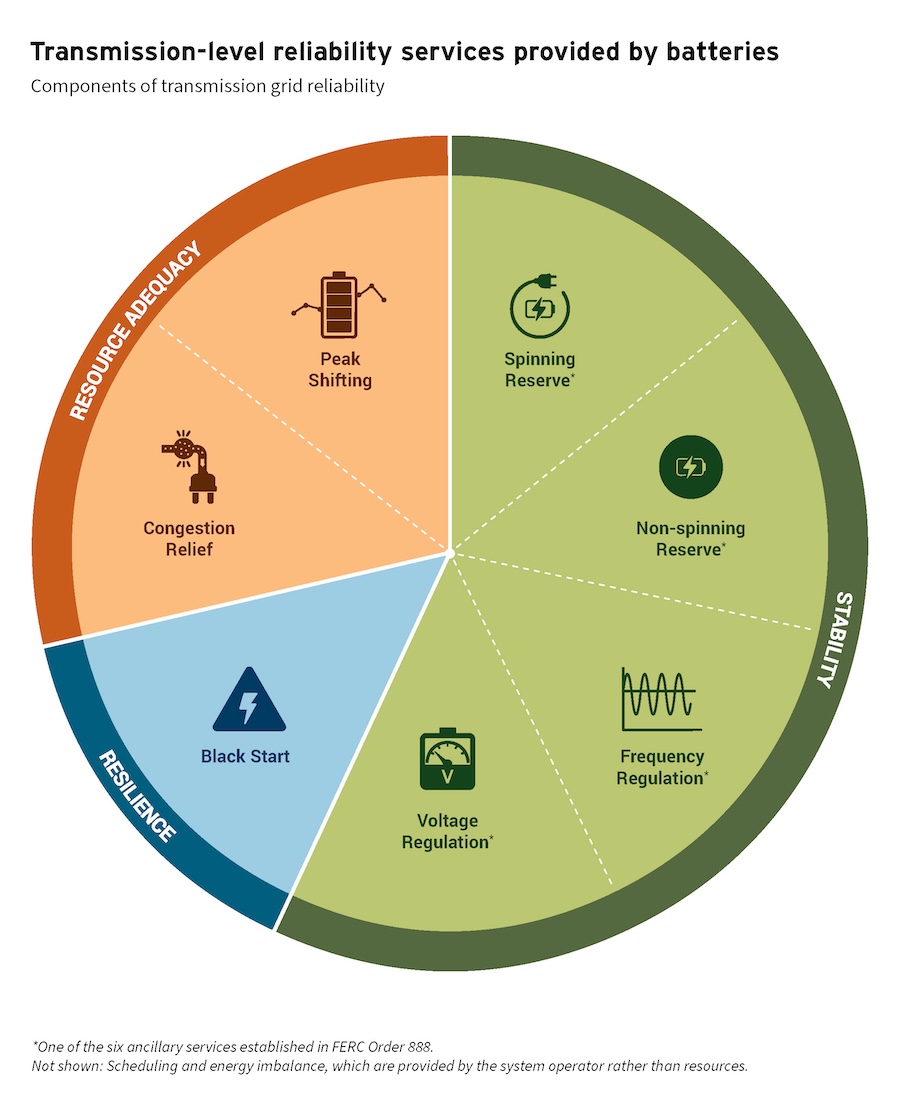

Thanks to research, development, and deployment, battery prices have declined by 90 percent since 2010, one of the fastest of any energy technology. Batteries can support all three main components of grid reliability: resource adequacy — the long-term ability to meet demand on peak; stability (also known as operational reliability) — critical short-term services like frequency and voltage regulation that stabilize the grid; and resilience — the ability of the grid to quickly recover from or support critical systems during an outage.

Historically, grid stability has been provided by large fossil fuel generators. As these generators retire batteries have already begun to fill the gaps.

Exhibit 1

Stability is typically provided in energy markets through “ancillary services” that support proper operation of the grid by keeping voltage, frequency, and power load in check. The Federal Energy Regulatory Commission’s (FERC’s) Order 888 established the types of ancillary services that utilities must offer, and variations on these have been adopted in regional ancillary service markets across the world.

The Electric Reliability Council of Texas (ERCOT) is a renowned leader in defining and refining ancillary service market products to ensure system reliability at low cost, which creates new ways for companies to earn revenue and encourages more participants to join the market. Batteries have successfully competed for these services, and as they have been added to the grid, they have grown to provide the majority of several ancillary services — with more competition resulting in lower costs than when fossil fuel resources were providing them alone (Exhibits 2 and 3).

This has resulted in both enhanced reliability and savings. During freezing conditions in Texas in January 2024, for example, battery energy storage systems contributed to $750 million in market savings while providing essential ancillary services that kept the lights on. And in California, the Valley to Colorado River transmission line enabled 2,400 MW of battery storage and 525 MW of gas resources to be developed in the Colorado River area. This serves the Los Angeles basin, and in 2022 saved customers $23.2 million in resource adequacy costs.

In contrast, in regions like PJM (a thirteen-state region including Pennsylvania, New Jersey, Maryland, and others), storage has not yet come online at scale, for reasons discussed below.

Exhibit 2

Exhibit 3

Reducing uplift costs

In order for batteries to provide the reliability and affordability benefits they’ve demonstrated in California and Texas, ancillary services must be well-defined and competitively compensated. Under specific conditions, like extreme weather, generators may be called upon to run even if energy and ancillary service market prices wouldn’t otherwise be economically sufficient. In those cases, consumers make additional payments to those generators (uplift payments) to wholly compensate for their costs to operate.

Exhibit 4

These out-of-market uplift payments ensure generators that provided reliability are made whole for their operating costs. However, payments can undermine the market’s ability to send actionable price signals, and also increase over time due to the lack of downward pressure from competition. On the other hand, ancillary services are in-market products, subject to competition, which means that when they are designed correctly, they are better equipped to meet reliability needs without driving up costs.

In PJM, almost a billion dollars in uplift costs have already been incurred in the first quarter of 2025 — 10 times more than any other regional transmission organization (RTO) in the United States, and more than 3 times the cost of PJM’s entire ancillary service market during the same period. This represents an opportunity to revisit whether more ancillary market products can be defined and made competitive so that batteries can compete against traditional generators to provide additional stability services. PJM is considering two of a number of useful market fixes, including a product that captures flexibility needs due to forecast uncertainty and a tracking metric to better account for following dispatch signals, but it’s unclear whether and how they may be implemented.

Stacking value

Storage can provide affordable stability, and in markets already deploying storage, batteries are also providing resource adequacy value (Exhibit 5). Battery storage resources can be enabled to participate in “value stacking” — being compensated to provide multiple reliability services when one single value stream is insufficient to justify new-build costs. The main categories of battery value stacking include participation in multiple market products across stability and resource adequacy: capacity market revenues, energy market arbitrage (storing energy when it is free or low-cost due to available, renewable resources, and then discharging or selling that energy when costs are higher due to higher demand and less supply availability), and ancillary service markets. Batteries may also stack in-market revenues in some cases with out-of-market revenues like corporate or utility offtake agreements.

In both California and Texas where robust battery markets have emerged, batteries are successfully competing to provide resource adequacy services, including energy arbitrage, in addition to ancillary services. Energy arbitrage helps ensure resource adequacy during risky peak-demand hours and enables batteries to maximize their reliability value to the grid. Energy arbitrage can also lead to lower costs — as batteries help the grid use more low-cost wind and solar at the most needed times.

As ERCOT’s ancillary service market has saturated and prices have gone down, batteries there are now pivoting toward arbitrage opportunities — enabled by renewable energy deployment. Their increasing share of earnings from arbitraging abundant solar energy have now also helped bolster resource adequacy on ERCOT’s system. Predictable intra-day price volatility is key to harnessing these reliability and affordability benefits. Regions with laggard renewable energy uptake won’t be able to capitalize on the advantages of battery energy arbitrage until increasing their clean energy generation.

Exhibit 5

Firm capacity during peak shifting is the other main resource adequacy service that storage can provide and stack along with critical stability services. Capacity is similar to insurance: in exchange for revenue, resources make a future commitment to be available with power at the times the grid most needs it.

In California, CAISO’s rules and reforms, which shift resource adequacy requirements from monthly aggregate to hourly assessments, have increased competitiveness and incentivized a surge of flexible and longer-duration battery storage deployment. In ERCOT, there is no capacity market or associated revenues; even so, the combination of ancillary services and energy were sufficient to incentivize significant battery energy storage deployment. In PJM, capacity prices jumped dramatically, with a record high of a $329.17/MW-day clearing price for the recent auction of the 2026/2027 delivery year. However, new batteries struggle to access this market since FERC approved PJM’s multi-year queue closure and transition proposal in 2022, and PJM’s continued noncompliance with Order 2023, which modernizes the interconnection process for new generation facilities. Furthermore, while this price surge promises higher potential capacity revenue, battery storage is also facing decreasing marginal value in PJM’s capacity accreditation framework, discounting how much of a battery’s capacity qualifies for payment.

Using smart planning and interconnection to harness the benefits of batteries

It’s clear that there is both a reliability and an economic case to encourage battery deployment, which is already happening in some regions. Those regions are successful due to two primary reasons: well-planned and stackable market products, and clear interconnection rules.

In many regions, battery deployment is still being held back not by market products, but by interconnection practices that need to evolve. FERC Order 2023 attempts to address this, but the impacts of this order are still yet to be seen. The PJM region, in particular, is struggling to connect new resources, including batteries, fast enough to prevent a resource adequacy crisis. Yet, just this year, FERC approved changes to PJM’s tariff that would allow batteries to participate in surplus interconnection service, a cost-effective way to bring new capacity online quickly.

Planners occasionally cite battery modeling difficulties due to uncertainty in terms of how those resources will operate; but the behavior of batteries in operation is, in part, driven by market products defined in planning. This chicken-and-egg cycle between planning and operations must be broken for market rules to fully unleash the reliability and affordability potential of battery storage. In regions with slower battery growth, regulators and planners should:

- Collaborate with regional grid operators to ensure batteries can competitively provide ancillary services, including considering new products that address either stability services the market currently lacks or those already provided and paid for out-of-market via uplift, which could be delivered by batteries faster and at a lower cost. ERCOT has comprehensively quantified and incentivized the flexibility attributes it needs to keep the lights on, services that have historically been met by fossil fuel generators. If other RTOs create products for their needed flexibility attributes, batteries can compete to meet reliability needs at lower cost than legacy generators.

- Ensure that in addition to stability, batteries’ resource adequacy services are accounted for and valued, addressing needs by providing low-cost capacity and energy. Given that state regulators have jurisdiction over resource adequacy, they should work with their utilities to ensure that batteries are being analyzed as resource adequacy assets and their capacity values are being properly accounted for. This will help quickly support resource adequacy, reduce capacity market prices, and when paired with low-cost renewable resources, reduce energy costs.

- Improve generator interconnection and associated planning processes, including for battery energy storage, by complying with and going beyond FERC Order 2023. Ensuring that battery modeling assumptions are not overly restrictive or unrealistic is one important component of Order 2023. Batteries are diverse and will not necessarily dispatch as a monolithic resource type since they can provide a range of benefits to the grid. Developers anticipating certain behavior should make the grid operator aware of the appropriate modeling assumptions so that planners can estimate the impact on the system accordingly. This will help planners capture the value that batteries provide, and additional reforms such as utilizing third-party automation software and fast-tracks like surplus service, energy-only service, and generator replacement will enable efficient market entry of these new, cost-effective resources.

US grid planners should take action to unleash the reliability and affordability benefits of batteries. Better planning practices and market products that enable batteries to fairly compete for their value streams are essential to ensuring more batteries come online in regions with laggard deployment. Appropriate modeling assumptions, ancillary service products, and competition also enable long-term price declines, saving people money while keeping the lights on.