Learn how we are working to transform how we use and produce energy.

Oil: Revenge Of The Negabarrels

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

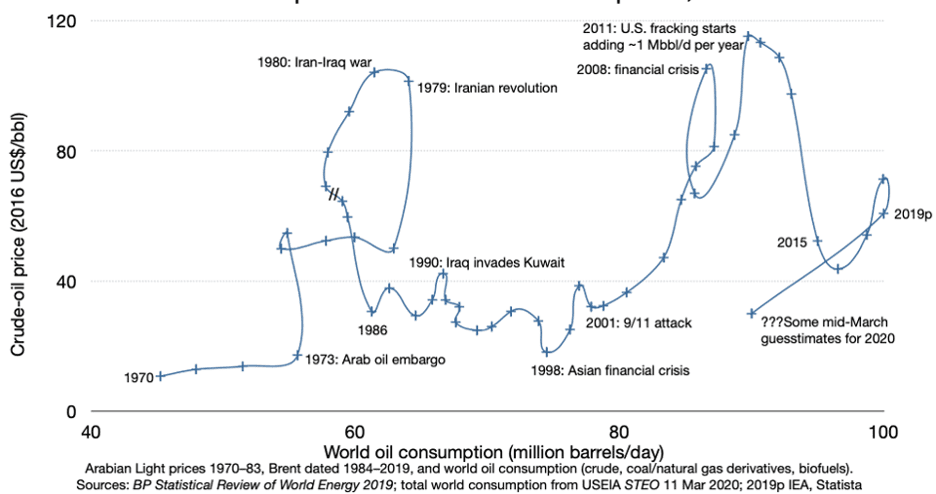

Never before, say shell-shocked oil traders, has the world price of crude oil fallen so far.

Well, not since the early 1980s, anyway. Or was it 2008? Or 2014? Look at the 50-year history:

Starting at the lower left, this roller-coaster ride of real price vs. use went wild in 1973–74 with a 217% price rise. Ever since, like other commodities, it’s done repeated loop-the-loops: price rises, use dwindles, price crashes, repeat. Yeehaw! Fasten your shoulder harness! Grab your barf bag! The only relief from this volatility is to climb off—to stop buying oil and buy cheaper, cleaner, constant-price efficiency and renewables instead. Now we can do that: oil is no longer, as a bailout advocate claims, a “must-have commodity…[with] no scaleable substitute.”

The pandemic-sped oil price drop is the fastest, but maybe not the deepest. Benchmark Brent crude oil’s annually averaged real price fell in 2008 by 36%, in 2014 by 47%, but in 1980–86, in an inexorable six-year skid, by 71%. From its January 2020 high to its April low, its daily price just fell 72% to below $20. Traders expect a rebound with eventual economic recovery, but $20 oil would put the entire US industry underwater despite the subsidies that most of its output already requires to yield a profit. A year of $20 oil would bankrupt many smaller suppliers and some nations. Saudi Arabia needs $80 oil to pay its bills, US frackers $40–50, Russia $40.

As big oil importers, Americans used to plead for cheaper oil. Now we beg our Saudi and Russian buddies for higher oil prices to protect economic zombies called frackers, who produce oil but not profits. Worse, with demand suddenly squashed, they’re nearly out of storage space: spare capacity in the Strategic Petroleum Reserve would hold only two days of world oil use, and the whole world will run out of spare storage in another month or so. The White House’s remedy —bailing out producers and investors rather than laid-off rig workers—would enlarge overproduction, prolong and intensify pain and risk, reward greedy blunders, socialize investors’ losses to our grandkids, and send oil and stock prices lower for longer. Surely they wouldn’t do that.

In the early 1980s, oil users responded to 1973 and 1979 oil price shocks and the delayed effects of smart Ford-Carter policies with a gusher of energy efficiency. President Reagan meanwhile boosted energy supplies far above demand. The resulting train wreck devastated suppliers and depressed oil prices for 17 years. Now we’re re-running that experiment just to make sure. US energy policy is expanding oil extraction by every possible means while failing to reverse potent efficiency trends. In 2019, the global economy grew 2.9% but world oil demand and price shrank, helping stabilize carbon emissions for the third year in five. This year, the same US mismanagement that had crashed the coal sector and embrittled the oil and gas sectors also enlarged the pandemic, dropping oil demand by at least one-third in two months. Now oil producers face the same fate, for the same reason, that bankrupted them in the 1980s: more supply than demand. Stupidity springs eternal; only the names and details have changed. So what does history teach?

The most important cause, led by Washington and made in Detroit, was 7.6-mpg-more-efficient domestic cars. The average new model drove 1% fewer miles but burned 20% fewer gallons—with 96% of its savings coming from smarter design, only 4% from smaller size. During 1975–84, the entire automotive fleet got 62% more miles per gallon, yet was safer, much cleaner, and no less peppy. By 1985–86, this had helped trigger a crash in the world oil price.

For the next quarter-century, policymakers hit the snooze button, ignoring President Gerald Ford’s 1975 legal mandate to continue cost-effective efficiency gains as technology kept improving. From 1981 to 2003, the average new US auto gained 24% in weight, 93% in horsepower, 29% in acceleration, but 1% in fuel efficiency. Holding acceleration constant would have boosted mpg by 33% and more than eliminated imports from the Persian Gulf by 2000. Today, protecting access to that oil remains our nation’s biggest military cost, risk, and burden. A Princeton study found in 2007 alone it cost about a half-trillion dollars, or three-fourths of the total national defense burden, or ten years’ worth of typical costs of buying oil from the Gulf. Our Pentagon-cosponsored study Winning the Oil Endgame estimated that in 2004, America’s $2-billion-a-day oil bill was only half the hidden costs thereby incurred for price volatility, monopoly pricing, and the readiness costs of US forces meant for Persian Gulf interventions.

So now fast-forward to 2020. American automakers, scheduled and poised to raise new autos’ mpg by 5% per year with uncompromised value and attributes, were just derailed by scuttled federal standards in two-thirds of the US—while high efficiency standards prevail in the other one-third and in all major foreign markets. Sundered markets and litigated standards just added years of uncertainty to risks imposed by the same Administration’s metal tariffs, disrupted trans-border supply chains, tariff threats inviting retaliation against US auto exports, and botched pandemic response that crashed auto sales. The White House’s own analysis admits its rollback of auto efficiency standards would cost jobs, health, and many billions of customer dollars.

Even before that friendly fire, automakers were struggling with falling sales, radical reforms to catch up on electric cars, weakening credit quality and investor confidence, and six years’ sectoral underperformance. By early February, the Big Three combined were worth less than Tesla—which Moody’s said was the only US automaker, and one of just six of the world’s top 20, well positioned for the clean-air, low-carbon automotive transition already underway.

Automobile sales peaked in 1990 in Japan, 2000 in Europe, 2016 in the United States, 2017 in the world. Before the pandemic, auto sales were slumping in China and India. The two million electric cars sold worldwide last year further sped the decline of oil-fueled car sales. World gasoline sales were thus forecast to stall by 2025 before the pandemic, which then halved them. US gasoline sales peaked in 2005. This month, they’re down by another 50–60+%. With coal in free fall too, the world’s total fossil-fuel use may turn out to have peaked in 2019.

The few major oil companies bravely trying to turn their supertankers—most recently Shell with its 16 April pledge of net-zero operational carbon emissions and 65% less from its products by 2050—will be hard pressed to evade a swarm of demand-side icebergs. Autos face not only renewable-electric competition but also a new car-free generation who prefer ridehailing and carsharing, bike and scooter services, rejuvenated public transport, virtual mobility, and cities redesigned around feet, not wheels. And not only autos can save oil. Mobility fuel’s #2 users, heavy trucks, offer doubled efficiency proven on the road, at least tripled on paper. The #3 users, airplanes, offer 3–5-fold efficiency gains. Both can advantageously switch to electricity, advanced biofuels, or renewable hydrogen (promising for transoceanic flights). The #4 users, marine shipping, can at least double efficiency and switch to renewable ammonia fuel, hydrogen, or advanced biofuels. Together, all these profitable shifts are ushering oil toward the exit, at least a decade sooner than expected. Natural gas, under severe competitive threat in every use and (like oil) threatened by its continued dangerous methane emissions, won’t be far behind.

For decades, I’ve been saying that oil is becoming uncompetitive even at low prices before it becomes unavailable even at high prices. Now that future has arrived. Saving oil costs less than buying it, let alone burning it, so oil owners are even more at risk from market competition than from climate regulation. More of their oil is unsellable than unburnable. The competing negabarrels—saved barrels—are safe, benign, all-American, and inexhaustible. So in an oil market that sputters at $60 a barrel, faints at $40, and vanishes at $20, what do negabarrels cost to produce? In 2004, Winning the Oil Endgame detailed how negabarrels costing $17 in today’s dollars could save half of US oil. In 2011, our Reinventing Fire synthesis updated how saving all US oil by 2050, with far greater mobility, could cost $20 per barrel saved in US transport or $14 just in autos. Today’s efficient autos can save a barrel for less than $7. That will fall below zero in a few more years as superior electric cars match or beat gasoline cars on sticker price alone.

As we ponder post-pandemic life, should America steer the energy transition so it strengthens or weakens national health, security, and prosperity? Should we further hobble US automakers by urging them to make obsolescent products that will raise mobility costs, harm health, and waste more oil—or harness innovations amassed over the past four decades to create a greater leapfrog than Detroit last exploited in the 1980s when its saved oil broke OPEC’s sword?

Combining electrification with lightweighting and streamlining can help put US automakers back in the global game. My quadrupled-efficiency German electric car pays for its ultralight and ultra-safe carbon-fiber body by cutting manufacturing costs and needing fewer batteries, which then recharge faster. The brilliant engineering and software in my wife’s American electric car make it the world leader. Both models sell briskly and profitably. US fossil-fuel dominance was always a self-destructive illusion despite rig workers’ skill, sweat, and grit. But strengthening American innovation in cars, trucks, and planes could return their makers and workers, including retrained rig hands, to durable health and global leadership. Why wait?

The sharp temporary crash in oil use can gradually be made permanent and complete. As negabarrels outcompete and replace barrels, solar and windpower have taken two-thirds and will soon take the last third of the world market for making electricity to replace fossil fuels in autos, buildings, and factories. Investment is shifting from the fading oil market to its bright successor, from volatility to stability, from crony capitalism to vibrant competition. This tragic pandemic, if turned to advantage, could help speed, focus, and perfect that market-led transformation.

This article was originally published on Forbes.

Authors

Amory Lovins

Cofounder and Chairman EmeritusRelated Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.