Learn how we are working to transform how we use and produce energy.

Hydrogen Policy Assumes Natural Gas Prices Are Stable. They’re Not

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Natural gas markets have been acting up lately. Consumers and businesses are in uproar, governments are bailing out users, and analysts are scrambling to explain the supply shortage and consequent price increases. In some markets, regulations and market structures have been overridden to protect consumers from the impact of higher energy prices.

The impact of natural gas price variability in a decarbonized economy should be better incorporated in energy policy, specifically as it has major implications for the emerging hydrogen markets.

No “Business as Usual”

In a broad context, the global natural gas markets are reaching record high volumes, and prices are at record lows. In the last decade, global natural gas consumption has grown by 33 percent, while prices, accounting for inflation, have dropped by half. These changes have largely been driven by the broad adoption of shale extraction technologies (fracking) and a global policy push away from coal.

But despite these trends, there is no business as usual. The declining price regime held true only until early this year. Natural gas prices have been on a steady rise for the past six months, disregarding some winter spikes that were driven by a combination of an Asian cold snap and reduced liquefied natural gas (LNG) terminal capacity. And prices are expected to stay high for at least another quarter. In most markets, these prices are passed on to consumers via their electricity bills, with dramatic implications.

Yet, in most assessments of the cost of the energy transition, the price of conventional fuels reference “business as usual” scenarios, often assuming a single, fixed price point relating to historical levels. There are several reasons why this assumption leads to inaccurate conclusions:

- Over the past 25 years, the coefficient of variation for natural gas prices is close to 60 percent, which is an abstract statistical metric that can be translated to the practical implication that there’s about a 50 percent chance of being 50 percent wrong (up or down) by using the historical average.

- Given current record-low price levels, there are many more potential outcomes with increased prices for natural gas than there are with lowered prices.

- Prices vary substantially across regions, and the variations are not correlated with the cost of renewable power.

Price Hikes Drive Multibillion-Dollar Cost to Consumers

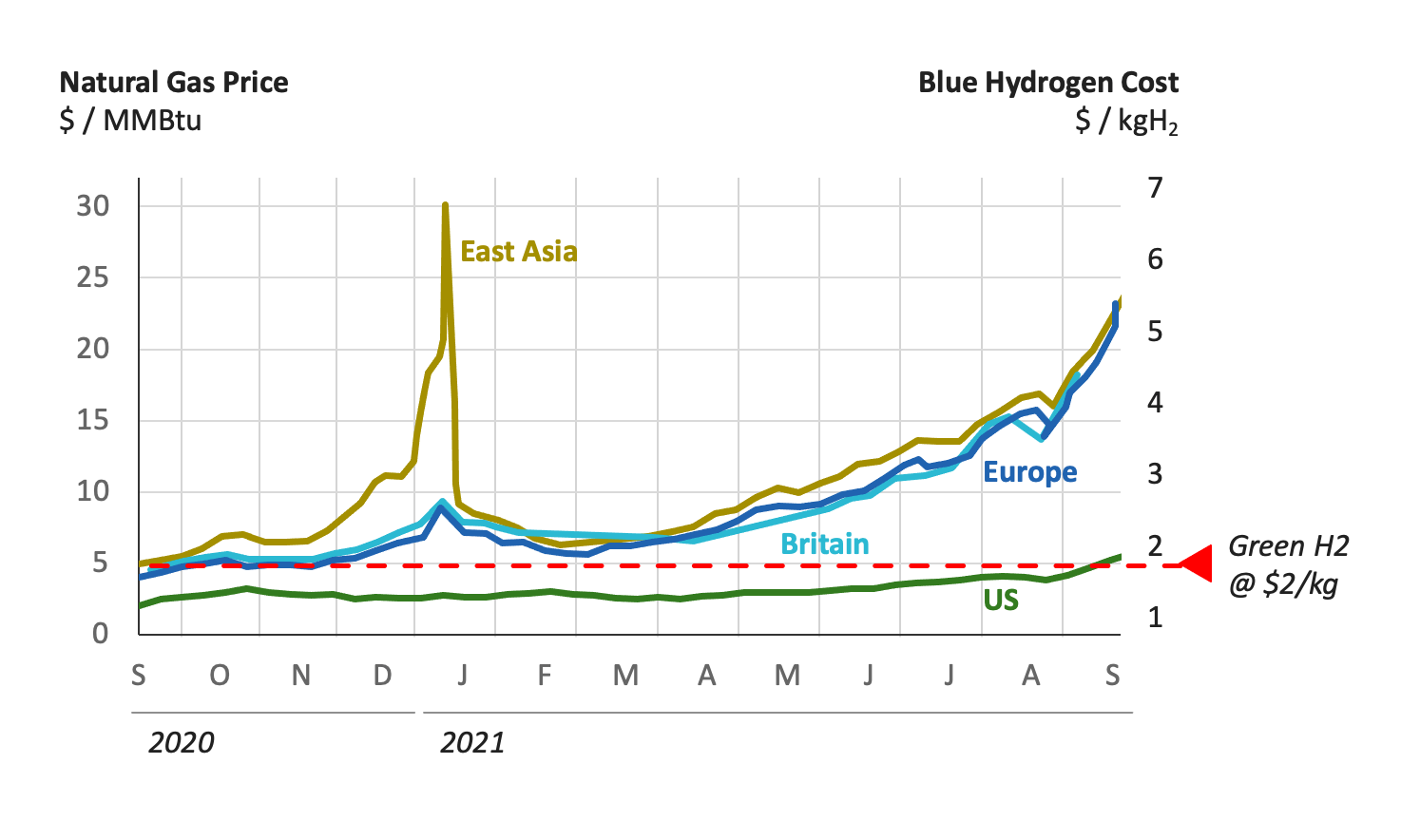

These assumptions are used for assessing the competitiveness of alternative pathways for decarbonization, so these assessments consequently undervalue the nonfossil options. For instance, consider the case of comparing “green” and “blue” hydrogen. Green hydrogen is made from renewable power with electrolyzers, whereas blue hydrogen is made from natural gas with carbon capture. A traditional benchmark assumes natural gas prices of around $5 per million British thermal units (MMBtu). This is representative of the last few years in Europe and Asia, but prices have recently climbed to a whopping $25/MMBtu.

This elevated price for natural gas translates to a price of about $6 per kilogram of blue hydrogen. Green hydrogen, in contrast, has the potential to absorb the variability of renewable power generation by ramping production up and down and can be locked to fixed-price power purchase agreements (PPAs). With the current projects in development, we can expect green hydrogen not exceeding $2/kg by the mid to late 2020s. With the natural gas prices of today, it would cost European consumers up to $20 billion more to rely on blue hydrogen as compared to green in 2030.

There Is No Market Like the Average Market

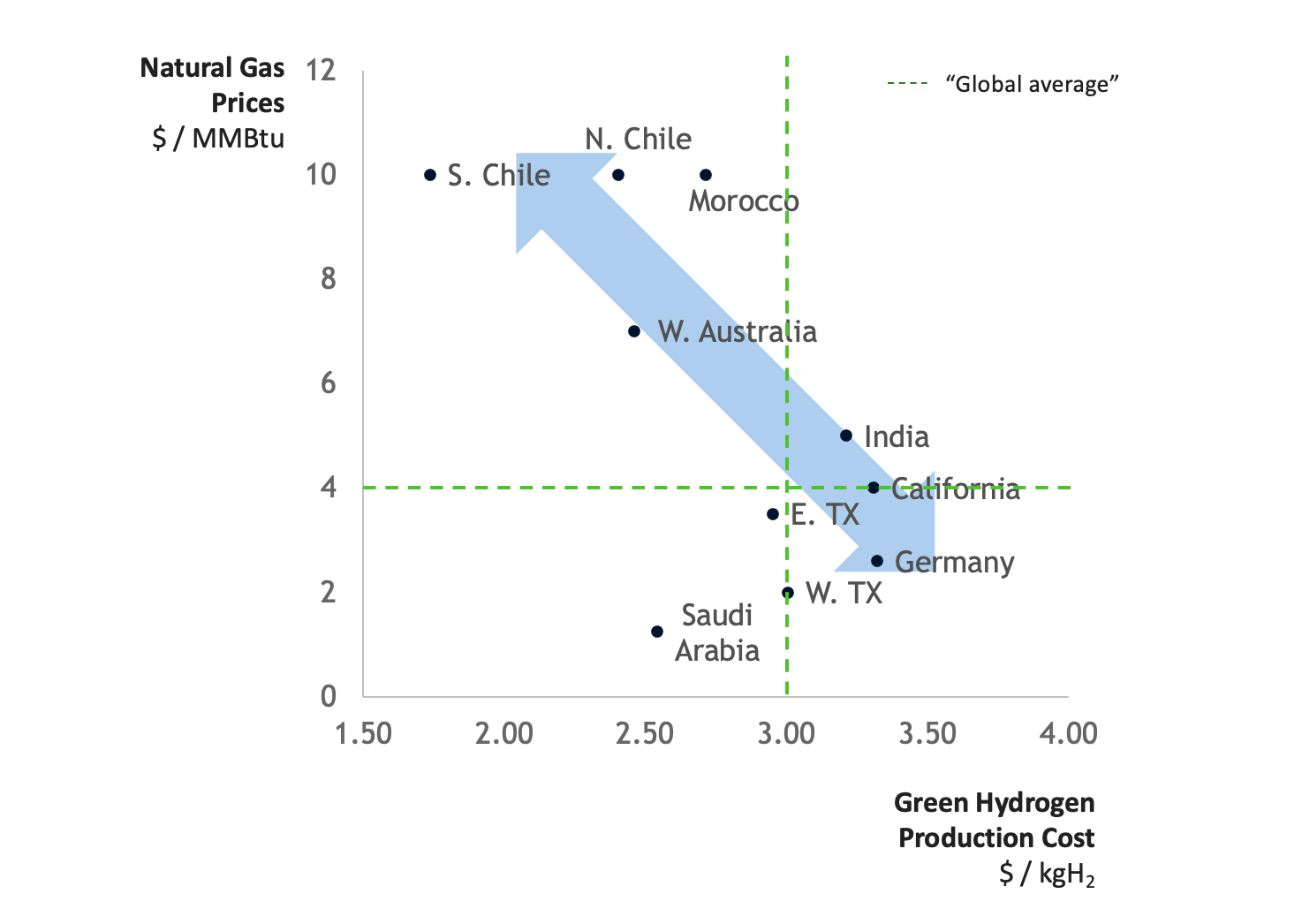

The fact that prices vary significantly across regions is lost in synthesis when making single-point assumptions for reference fuels. In reality, both natural gas prices and electricity prices are not homogenous across markets. More intriguingly, these prices are not correlated but rather anticorrelated (Exhibit 2).

These simplifications can lead to strategic misguidance. For example, the hydrogen-producing technologies are fairly comparable in terms of cost across regions, whether using electrolyzers that split water into hydrogen and oxygen, or steam-methane reforming (SMR) facilities with carbon capture (which react methane gas with steam to produce hydrogen). This means that the installation cost (capex) for hydrogen production evolves at the same pace globally. Across several technology pathway assessments, the electrolyzer capex is expected to drop from the current $700/kW to $200/kW no later than 2030.

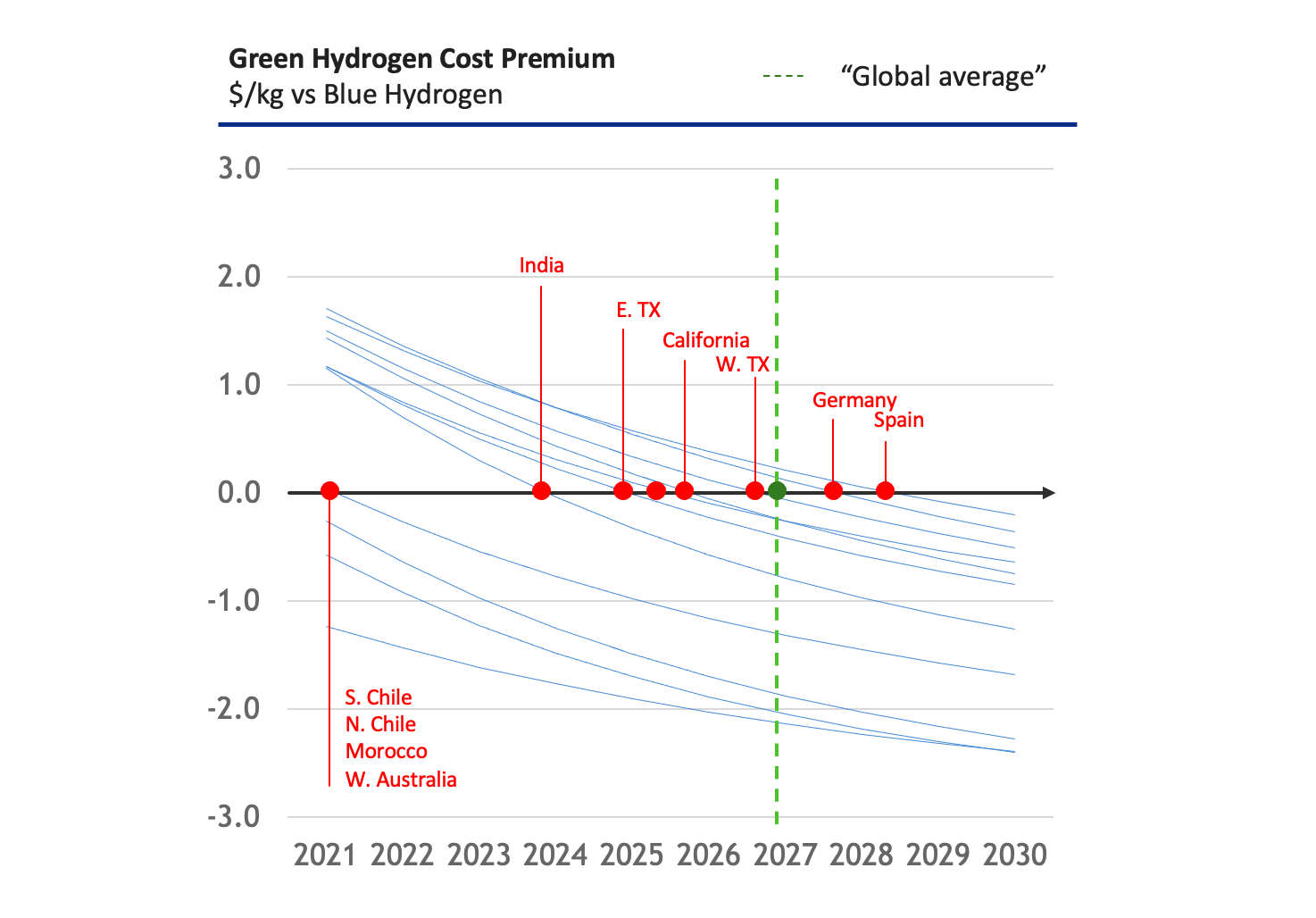

Comparing green and blue hydrogen using global average prices leads to the conclusion that they will meet at an inflection point in 2027, after which the electrolyzer route is expected to become the lowest-cost option for clean hydrogen. But incorporating the anticorrelation of real market price structures, it is evident that many markets have already crossed that inflection point (Exhibit 3), due to their access to very low renewable prices and exposure to expensive LNG for natural gas.

Taking the Thumb off the Scales

More informed strategies for assessing the cost of the energy transition will counter the historical bias to understate the value and impact in many markets of hydrogen made from renewable energy with electrolyzers. These strategies will need to examine regional market dynamics, rather than global averages, as well as considering how other, adjacent energy market trends could affect the price of fossil fuels. By moving away from flawed assumptions, we can accurately determine the most affordable and lowest-emitting way to power our economy going forward.

Related Insights

Harnessing Green Demand to Drive Sustainable Chemicals Production

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.