Learn how we are working to transform how we use and produce energy.

Georgia Power and the Golden Securitization Opportunity

One financial tool could save Georgia Power ratepayers over $1 billion while opening up new avenues for reinvestment in coal communities.

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Georgia Power has recorded a dramatic decline in coal usage. Whereas coal fueled over 60 percent of the utility’s power generation in 2010, it supplied just 15 percent of the utility’s electricity in 2020. Georgia Power is already preparing for the ultimate phaseout of coal, stating in its latest Integrated Resource Plan (IRP) that the utility plans to retire all its coal-fired power by 2035.

While Georgia Power’s transition away from coal is good news for the climate, it remains unclear how the associated retirement and transition costs will be financed by the utility and allocated to customers. Equitably sharing the investments in transition is the next big question for utilities, regulators, and customers.

Typically, for a coal plant that is shut down before it reaches its forecasted service lifetime, hundreds of millions of dollars of invested capital can remain unrecovered. Under the conventional utility business and financing model, there are few attractive ways to return this capital to the utility. And for utilities like Georgia Power that operate under the cost-of-service regulatory model, the obligation to pay off the unrecovered capital almost always falls to ratepayers. Continuing to pay off the remaining balance as a utility asset, as part of the rate base, means ratepayers go on paying the full approved rate of return — including utility profits — for what is now a “ghost” asset, sitting on the utility’s books with little to no associated risk. Keeping the asset on the utility’s balance sheet also means that new generations of utility customers will be paying for an investment from which they never received any tangible benefit. And while shortening the recovery period can mitigate intergenerational cost shifting, doing so will put upward pressure on near-term utility rates, which rise if more capital is returned to the company over a shorter period.

Similar problems arise with respect to coal ash ponds. These ponds, designed to hold toxic waste from coal power plants, have contaminated water supplies and pose a risk to nearby communities. Complete clean up of these toxic risks is both critically necessary and costly. Remediation of Georgia Power’s coal ash ponds is projected to cost over $9 billion through the 2080s, with well over half of those charges set to be incurred over the next decade and financed as utility assets. Allowing utilities to profit off the cleanup of environmental liabilities that could have been mitigated and/or avoided by prior risk management is arguably unfair — and incontrovertibly expensive. And even if some clean-up costs are shouldered by shareholders rather than ratepayers, the increased costs to investors may increase the utility cost of capital and thus still harm ratepayers.

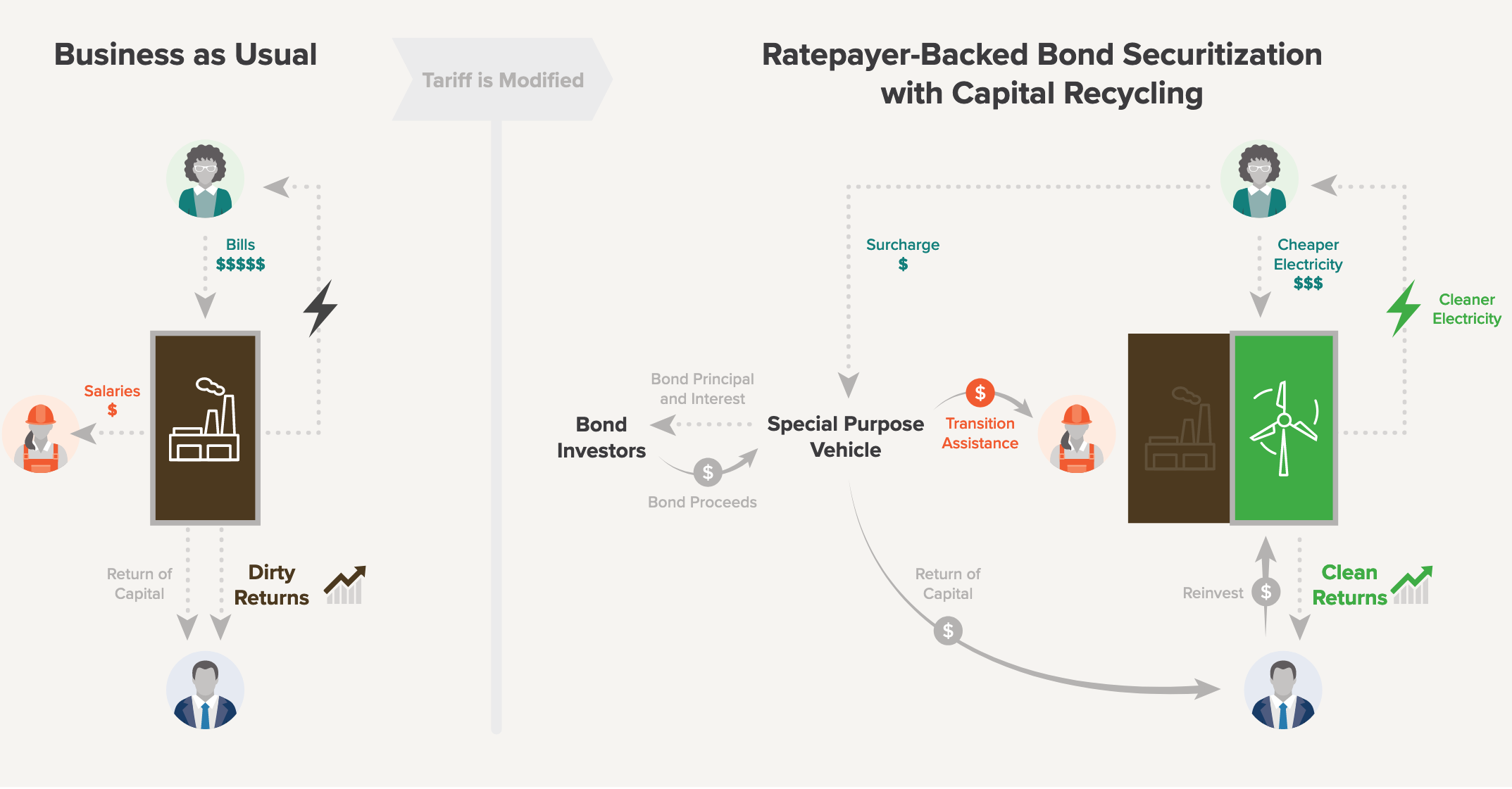

Luckily, there’s a proven solution: a financial mechanism called securitization. Securitization is a financing tool that creates the possibility for a win-win: when a coal plant retires, consumers pay lower electricity rates and utilities invest in and benefit from clean energy investment. As we have written before:

“Utilities have used securitization for decades to lower customer costs for unanticipated expenses, and recently the tool has been applied to support coal phaseout. In the context of coal retirement, securitization is akin to refinancing a mortgage. The rates paid by customers of investor-owned utilities in the United States include charges to allow utility investors the opportunity to earn a fair return (on an after-tax basis) on their invested capital. Since utility capital is usually an even mix of debt and equity, this translates into an effective “interest rate” (analogous to that of a mortgage) of 8–10 percent. Securitization replaces this rate of return with a low-interest-rate bond (of about 2–4 percent) that is paid back over a long period of time.

By refinancing the existing customer obligation to pay the utility’s return on equity and debt with just low-cost debt, securitization creates immediate and long-term savings for ratepayers… Utilities can reinvest their capital in needed transmission system upgrades and cheaper clean energy assets. Importantly, states must pass legislation to ensure that bonds receive a high rating, which maximizes savings for customers”

Eleven states already have some form of legislation authorizing securitization specifically for refinancing coal costs. Last year, a bill called the Georgia Utility Rate Reduction Act (GURRA) would have extended these benefits to Georgia Power’s ratepayers by authorizing securitization. With this financing tool, Georgia Power and the Georgia Public Service Commission would have the ability to reduce rates while allowing reinvestment in cheaper renewable energy. To better understand the scale of this opportunity, we calculated the potential ratepayer benefits from even a limited use of securitization.

Modeling Assumptions and Results

RMI looked at securitizing the unrecovered balance of Wansley Units 1 & 2, a coal plant retired in August 2022, as well as the expected cost of the coal ash remediation projected through 2031. We assumed an estimated remaining plant balance of $557.4 million for Wansley 1 & 2 at the close of 2022, whereas coal ash outlays, as indicated in company filings, were estimated at $4.50 billion from 2023–2031 inclusive of unrecovered capitalized costs from prior years. Additional cost ash remediation outlays from 2032 through 2083 are projected to reach $3.5 billion, but as granular data were not available and the implied yearly amounts relatively small, RMI assumed that these costs would be recovered from annual collections without the need for financing. RMI modeled recovery of the Wansley plant balance through amortization of a 10-year regulatory asset, rounding up slightly from the remaining depreciation schedule of 9.5 years as the model does not accommodate partial year inputs. For the coal ash remediation costs, a 3-year recovery period was assumed for outlays in any given year, in line with company filings.[1] Accumulated deferred income taxes (ADIT) were estimated for Wansley but not modeled for coal ash remediation. Using conventional utility finance, the net present value (NPV) of ratepayer costs (2022$) were calculated as $572.9 million for Wansley 1-2 and $3.67 billion for coal ash remediation outlays through 2031. [1] Per the information in APA-SPA-ADH-MBR-1, Sch 3, p7.

Securitization

Securitizing these costs could dramatically reduce the burden on ratepayers. RMI estimated forward-looking interest rates for AAA-rated securitization bonds using the September 8, 2022, US Treasury Yield Curve. The bonds for Wansley 1 & 2 were modeled as a 2023 issuance with a 10-year tenor, in keeping with the life of the regulatory asset and respecting the goal of limiting impacts on future cohorts of ratepayers who may never have received any benefit from these units. For coal ash remediation, however, RMI decided that a 25-year tenor was not only financially advantageous but also justified in terms of intergenerational equity, as all future customers will benefit from environmental enhancements. All bond issuances included initial fees of $3 million per transaction plus 0.7% of the initial capital raise before fees. Annual servicing fees were sized at $300,000 plus 0.05% of the initial capital raise before fees. This is in line with past securitization transactions. Including transaction fees, bond issuances associated with the coal ash remediation through 2031 totaled $4.55 billion, or approximately $50 million more than the outlays under the utility finance approach without transaction fees. Given the large size of the annual coal ash outlays from 2023-2031, RMI chose to model separate securitization transaction for each year, avoiding interest charges for pre-funding outlays in subsequent years in exchange for accepting additional fixed transaction and servicing fees. Deals could be structured differently, for instead with simultaneous issuance of multiple tranches of bonds with different tenors. If securitization transactions are approved, regulators should seek to maximize savings for consumers. Using the securitization approach as outlined, the net present value (NPV) of ratepayer costs (2022$) were calculated as $469.9 million for Wansley 1-2, a savings of $102.9 million versus utility finance, and $2.73 billion for coal ash remediation outlays through 2031, a savings of $942.6 million.

Securitizing both Wansley and coal ash costs would save ratepayers a total of $1.05 billion. This would have huge impacts for a state with the 7th-highest average monthly residential electricity bills, and especially important for low-income households experiencing severe energy burden.

Now, it is up to Georgia’s leaders to implement this solution.

- Securitization legislation, like GURRA, allows for the securitization of both unrecovered net plant balance of coal plants and coal ash remediation costs, while ensuring robust protections for ratepayers.

- If securitization is enabled in Georgia, Georgia Power would have a new pathway for recovering legacy investments that not only lower costs for ratepayers but could even open up new opportunities for profitable clean energy investments.

- As it considers the costs, opportunities and risks inherent to the energy transitions, the Georgia Public Service Commission, along with intervenors, should consider the full breadth of financing options to ensure ratepayers obtain the best possible deal, as well as how equitable solutions can lower rates while simultaneously supporting the transition to cleaner energy.

Georgia has an incredible opportunity to clean up the environment and save ratepayers money, all while ensuring the financial viability of Georgia Power and safeguarding future economic prosperity for fossil workers and communities. Transition financing solutions like securitization are proven and effective, and all stakeholders joining together can make an equitable and prosperous transition possible for all Georgians.

Authors

Christian Fong

Ben Serrurier

David Posner

Related Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.