Learn how we are working to transform how we use and produce energy.

Fannie Mae’s Financing for Solar: A Game Changer for the Solar Industry

Why we share this work for free

RMI is an independent nonprofit working to accelerate the clean energy transition. We publish research like this to inform decision-makers and drive real-world impact.

Our work is supported by philanthropy as well as partnerships, including fee-for-service engagements. This support makes it possible for us to share our independent insights for free.

If you find this work valuable, you can support it anytime.

Get more insights like this

Stay up to date with the latest research, analysis, and tools from RMI by opting in to receive occasional emails below. You’ll get new reports, event invitations, and practical insights to help us all accelerate the clean energy transition.

Loading form...

Your download should start automatically. If it doesn’t, click the download button below.

This work is made possible by philanthropy

RMI is a nonprofit supported by donors and partners. Philanthropy enables us to produce independent research and make resources like this freely available.

If you find this report valuable, please consider supporting our work. You can also explore how we partner with organizations to drive impact.

Jump to Section

Guest author Jamie Johnson is the founder and CEO of Energy Sense Finance.

Mortgage companies play an important role in making solar photovoltaics (PV) more affordable and accessible for homeowners, which is a key component to unlocking the economic opportunities of home energy upgrades. Learn more about how this complements RMI’s Residential Energy+ initiative, which is working with top industry representatives to make better energy performance more accessible, affordable, and desirable for U.S. homeowners.

Mortgage giant Fannie Mae just unlocked the lowest cost of capital for new solar installations to date. This follows the Department of Housing and Urban Development’s (HUD’s) recent decision to finance new solar installations within a first mortgage transaction, a potential game changer for the solar industry with the ability to bring about the next order of magnitude increase in solar installations.

Fannie Mae’s HomeStyle Energy Mortgage offers the lowest cost of capital for solar (currently a mid-three percent range fixed rate). To date, this market is the largest untapped source of low-cost capital that the solar industry can leverage for the benefit of homebuyers and mortgage refinancers. A new source of low-cost capital is increasingly important in order to accelerate solar industry growth, as some solar leasing companies have seen their own cost of capital rise in recent months or had access to capital shut off completely. This could be the game changer the solar industry has been looking for, with the capacity to change everything from the value proposition of solar ownership all the way to how solar is marketed and sold to current and future homeowners.

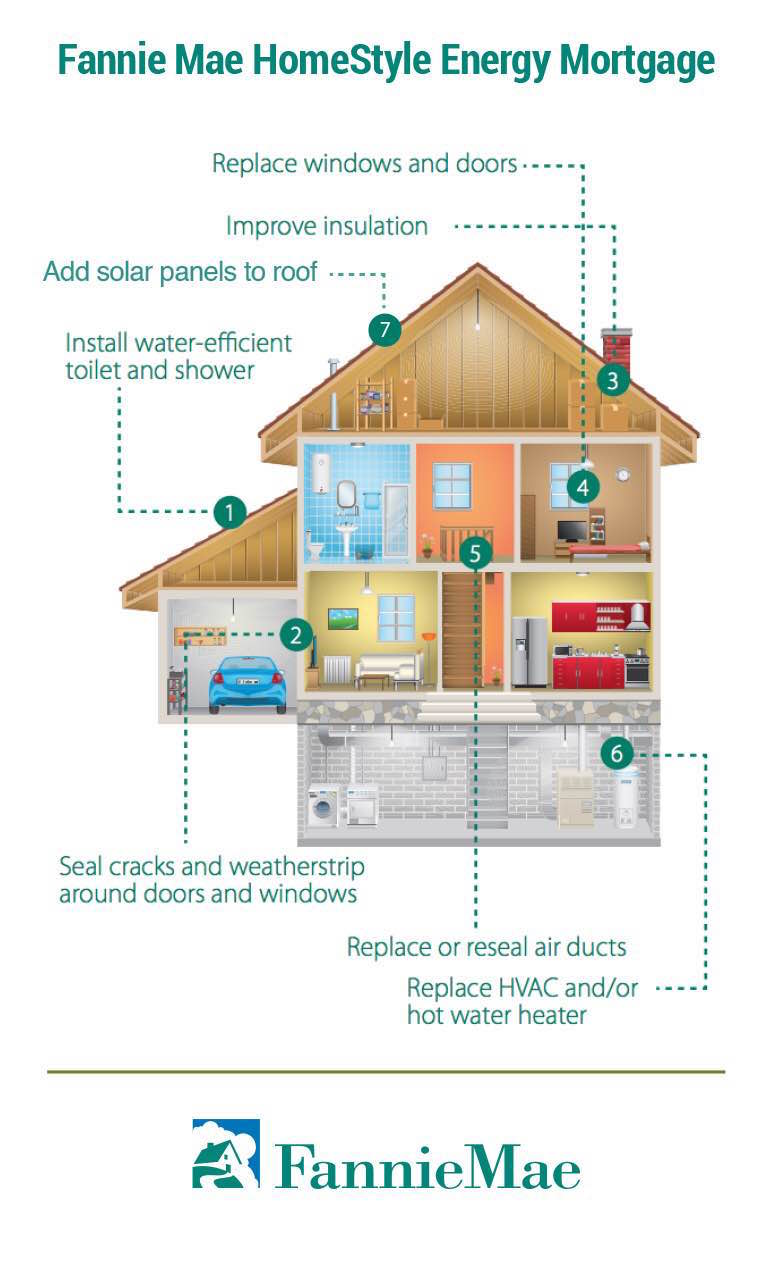

WHAT IS THE HOMESTYLE ENERGY MORTGAGE?

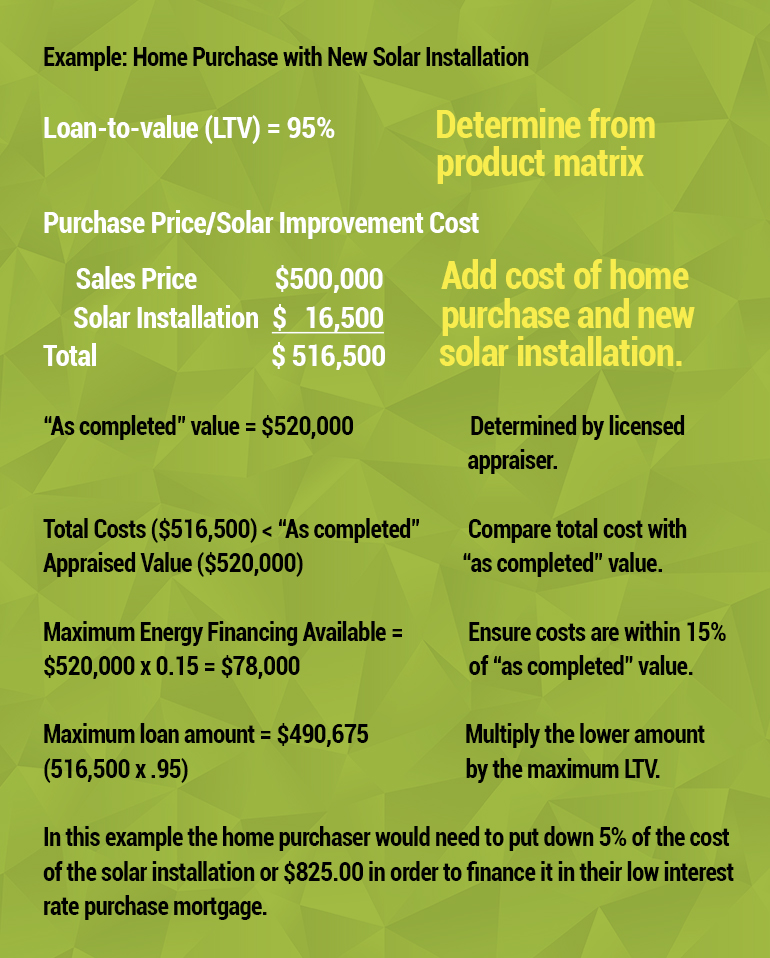

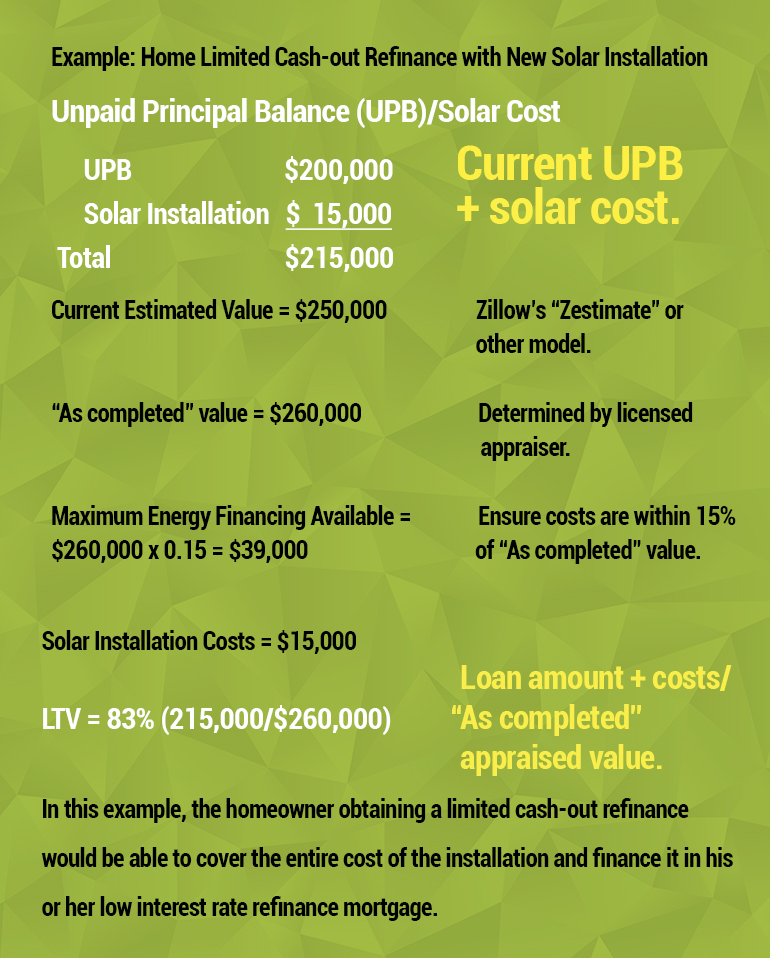

The HomeStyle Energy Mortgage from Fannie Mae enables a homebuyer or mortgage refinancer to add a solar system after the mortgage loan has closed. This is done by allowing up to 15 percent of the “as completed” home value to be used to pay for the cost of a solar system with funds escrowed by the lender, and gives the homeowner 180 days after the closing date to have the solar system installed. The new mortgage requires a home energy report to determine the cost-effectiveness of the solar improvement. The report must show that the present value of energy savings is greater than the cost to install. The homeowner must also have an as-completed appraisal, which includes value for the not-yet-completed solar system.

The initial concept, including the benefits of financing new solar installations within a purchase or refinance mortgage, was first proposed in 2012 to industry stakeholders, including Rocky Mountain Institute. It was then presented in 2013 at the Photovoltaic Specialists Conference.

Methods for developing a value for solar using the appraisal industry’s income and cost approaches were proposed in 2010, and later published in the fall 2013 edition of the Appraisal Journal (a publication of the Appraisal Institute), and have been allowed by both Fannie Mae and HUD since 2015. Appraisers, realtors, homeowners, and lenders can now estimate the market value of solar by using the free online PV Value® tool that was recently developed by Energy Sense Finance with funding from the Department of Energy’s (DOE’s) SunShot initiative.

WHY THIS IS A GAME CHANGER

Adding solar when purchasing a home or refinancing a mortgage has the potential to become the default choice, like repainting a room, doing new landscaping, or any other minor improvement a homeowner makes when completing a new real estate transaction. Fannie Mae’s financing for solar can result in:

- More captured value: As homeowners continue their shift away from leasing solar to owning solar, this new financing will allow homeowners to both capture more of the monthly savings (instead of paying it out to a third party), and capture the value of solar within their home’s appraised value.

- Lower installation costs: This new financing method for solar will help drive down installation costs by allowing homebuyers and homeowners to consider small, local solar installation companies for a quote. Many smaller solar installation companies are currently unable to offer competitive low interest-rate financing arrangements, yet are properly licensed, trained, and able to offer very competitive installation costs without financing.

- Solar as a commodity: Taking financing out of the equation will encourage healthy competition between installation companies and turn solar into a commodity, because homebuyers and mortgage refinancers can now have the cost of the solar installation included within their mortgage at their low, already agreed-upon interest rate. It’s like walking into a car dealership with a check in hand from the local credit union, knowing what the the value of the car is before purchasing, and eliminating the need for any dealer-provided financing.

- Increased viability: As installation costs align with local marketplaces, solar will become competitive with traditional energy sources in more states, including those with lower utility rates, increasing the solar adoption rate in the process.

THE TECHNICAL AND MARKET POTENTIAL

The conforming mortgage industry currently averages just over four million purchase and refinance transactions per year. Meanwhile, the National Renewable Energy Laboratory estimates that up to 89 percent of available small rooftops measuring less than 5,000 square feet are good candidates for solar and can support a minimum system size of 1.5 kW.

If Freddie Mac follows Fannie Mae and HUD with a similar offering of its own, it could open up financing for new solar installations within 3.5 million residential mortgage transactions per year, allowing for solar systems to be installed after mortgage transactions close.

While several factors will have an impact on the actual market potential—age of roof, local utility rates, net energy metering policy, installation costs, available solar resource, and others—as utility costs continue to increase and the cost to install solar continues to decrease in many states, we estimate between 1 and 1.75 million homeowners will take advantage of the ability to finance solar installations at the lowest interest rate available.

This new market potential comes as the solar industry recently celebrated its one millionth installation, a milestone that took nearly 40 years to achieve.

Just one million installations of homeowner-owned solar per year at a value of $10,000 per system has the potential to add $10 billion annually to residential property values nationwide.

WHAT ABOUT LOWER INCOME, LOW DOWN PAYMENT BORROWERS?

For those who can’t meet the typical Fannie Mae requirements for a higher down payment, income, or credit score, there is a similar product from HUD, referred to as the “solar and wind technology policy.”

It can be used with both purchase and refinance transactions, and allows for up to 20 percent of the “as-is” home value prior to the solar installation to be used to cover the cost of a solar installation. Additionally, it gives the borrower up to 120 days after the mortgage closing date to have the solar system installed.

WHAT ABOUT NEW HOME CONSTRUCTION WITH SOLAR?

For new home construction, the DOE’s SunShot initiative funded a working group, led by Sandia National Laboratories, that put together Solar Basics for Homebuilders, a guide that lays out the financing options available to both homebuilders and homebuyers who want to include a solar system with their new home.

Additionally, the Appraisal Institute, working in conjunction with the National Association of Homebuilders and the Building Codes Assistance Project, put together information for homebuilders to ensure that the new homebuyer receives an appraisal from a competent appraiser who has received specific training in valuing homes with solar.

There are now multiple sources of low-interest rate financing mechanisms in place for new solar installations that allow virtually all current or future homeowners to own their solar, maximize their monthly savings, and ensure the solar PV value is included in the appraised value of their homes.

WHERE DO WE GO FROM HERE?

Marketing to homeowners and homebuyers is the first step to ensuring they become aware of new low-interest rate financing options for solar. At the same time, appraisers need to be trained in how to properly develop value for solar systems before conducting an appraisal on a home with a solar PV system. Even further, underwriters need to be educated on allowable valuation methodologies. To assist with this effort, the Appraisal Institute offers a two-day course titled “Residential and Commercial Valuation of Solar,” developed with funding from the DOE’s SunShot initiative. There are additional educational efforts underway that will be announced later this year.

Solar installers may seek to work with real estate agents, home sellers, and homebuyers to educate them about these new financing options. They may also offer a solar installation quote with each new listing, along with an estimate of the value using the free PV Value® tool. Additionally, they may want to obtain a home energy rater designation and become a HERS or HES rater, if current guidelines remain in effect.

Energy Sense Finance plans on undertaking education efforts relating to valuation of solar with the free PV Value® tool, providing a national database of solar installations to appraisers, and addressing the valuation of energy storage with solar in the new Ei Value® platform that will be available later this year.

Providing a source of low-cost capital and enabling market value for solar were two missing pieces needed to enable a more rapid solar adoption rate and, now that those are coming into place, the solar industry can look forward to many sunny days ahead.

Stay tuned for our next blog in this series. We will explore a variety of financing products for home energy improvements, determining how they vary from both a consumer and a lender standpoint. While other products exist that allow homeowners to directly purchase home energy improvements, we would like to better explore why certain products are more conducive to rapid uptake of solar and energy efficiency than others

Image courtesy of iStock.

Infographics Source: Fannie Mae and Energy Sense Finance.

Authors

Laurie Stone

Managing EditorRelated Insights

Help build the clean energy future. Donate today.

Independent research. Real-world solutions. Supported by donors.

RMI can pursue the highest-impact climate and energy solutions because we’re supported by people who believe change is possible. Every gift helps advance the work needed to make clean energy the default choice worldwide.

For other ways to give to RMI, including checks or gifts of stock, please visit Other Ways to Give.